A monster TSMC print, a Netflix guide-down, a VIX finally noticing. The front end saw this two days ago.

⚓ Weathervane: The Fed has turned hawkish for the cycle. The committee’s own dots flipped from a cut to a hike under Warsh, and higher-for-longer is now confirmed by the instrument. The unconfirmed second leg is risk appetite: equities are still trading as if the turn isn’t real.

Ahoy there, Trader! ⚓️

Ahoy there, Trader! ⚓️

It’s Phil…

A curious one to sit with this morning.

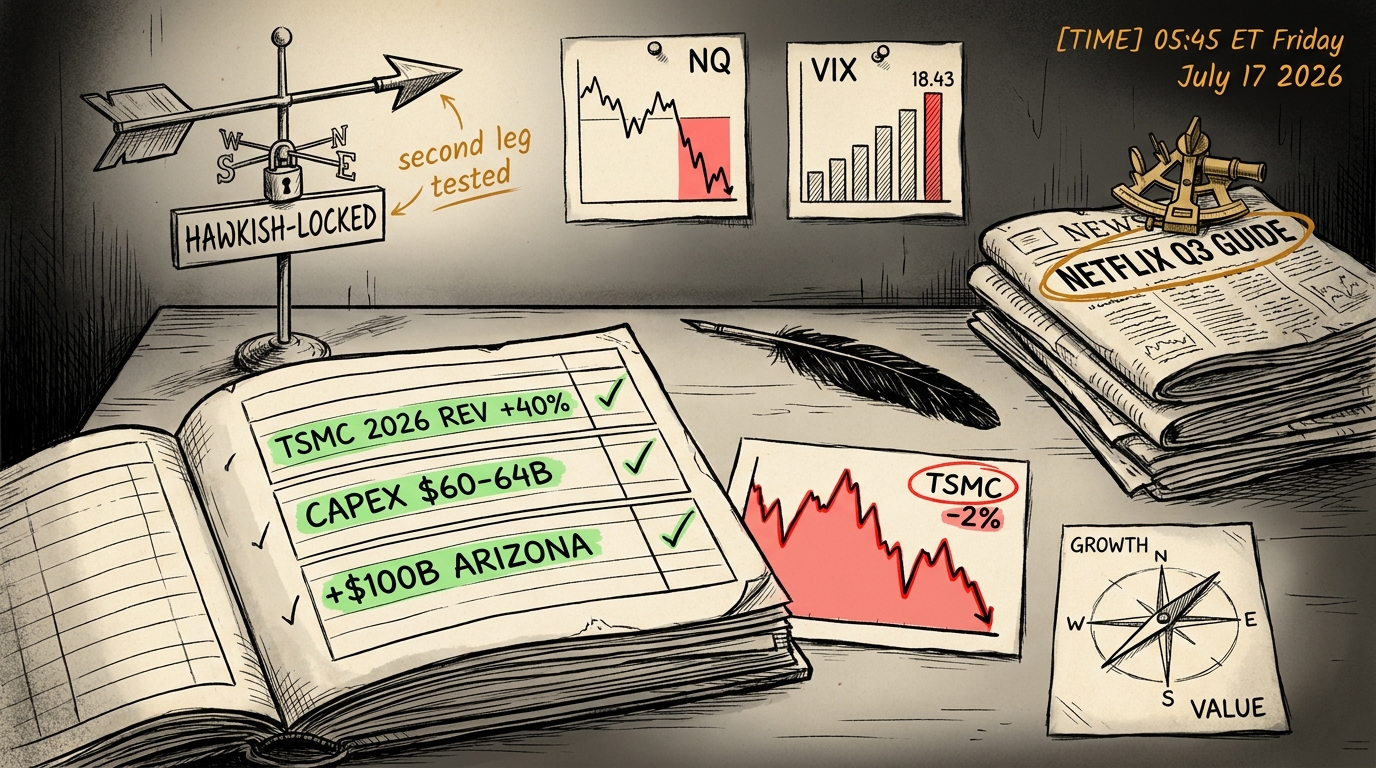

Yesterday the AI trade got exactly what bulls had been asking for. Taiwan Semiconductor, the tollbooth on the AI highway, beat the quarter, lifted 2026 revenue growth to slightly above forty percent from a prior “above thirty,” raised capex to sixty to sixty-four billion from fifty-two to fifty-six, and added another hundred billion in Arizona. The chairman told the call his AI conviction “remains very high.” The stock fell two percent.

Overnight, the chip complex extended the bleed into a second day. Netflix guided a hundred-forty-million-dollar Q3 shortfall against consensus and fell eight percent after hours to a fresh fifty-two-week low. S&P futures gave back over one percent, Nasdaq futures over two, and the VIX bid to eighteen for the first time in six weeks. The two-year held at four-sixteen, essentially unchanged from Wednesday. The front end did not move.

So here is the day’s honest question.

If TSMC’s forty percent guide and record capex could not lift the chip complex, what was the tape actually selling?

Let’s walk the dots. TSMC is a vendor. It sells wafers to Nvidia, Apple, and Qualcomm. Its guide up historically reads as “vendor sees demand,” and its capex up as “vendor commits to more supply.” Textbook: raised vendor guide plus vendor investment plus softer front end equals higher tape.

The tape read differently. Raised guide from a vendor is a signal about total capex the sector must earn back through end-customer revenue growth, and the tape is no longer confident that revenue growth is turning up. Netflix compounded it, a large-cap growth story delivering a second decelerating guide inside two quarters. Two very different growth companies telling the same growth-multiple story. The pattern the tape has priced: the AI capex bill goes up, the customer revenue goes sideways.

Here is where the front end enters. Wednesday’s soft PPI and Warsh’s Senate register took September hike odds off twenty-two points in seven sessions; the two-year fell to four-twelve intraday. Wednesday’s equities read that as tech’s rally to enjoy. Overnight is the tape re-reading it as tech’s revaluation. A slower Fed with a slower customer means the AI capex has to earn its way through something other than easy money and hyper-growth. That is a different question than “when does Warsh hike,” and it does not close by the front end alone.

Textbook says higher. Reality: tape lower, VIX bid, chip complex bleeding through a beat-and-raise, growth-multiple stocks bearing the widest damage. The tape has decided that the confirming signal is a top signal.

Phil’s Musing

The one that keeps me honest here is the timing. The front end priced this two days before the tape did. If I were only reading the equity moves, I would say something snapped overnight and Netflix was the shove. But the two-year was already there on Wednesday, and the equity move is the follow-through. My lean is that this is not a spike; it is a re-rating that started earlier, quietly, and only became visible when a beat-and-raise from the strongest AI vendor got sold. Alphabet on the twenty-fourth is the print that tells us whether the customers agree.

Happy trading,

Phil

Less Brain, More Gain

…and may your trades be smoother than a cashmere codpiece

P.S. – Phils Footnote I do not know when this ends. What I know is that “growth is now an accusation” is a proper regime signal when a forty percent guide and a hundred-billion-dollar Arizona commitment cannot lift the vendor that just delivered them. Six sessions ago, the front end told us. Two days ago, Wednesday’s equity celebrated. Overnight, Thursday’s equity revised. That is a market working through information at three different speeds, and it is honestly interesting to watch in real time. If Alphabet or Tesla or Meta names AI capex as a margin item in the next three weeks, I will be back here with a rewrite of the Weathervane. If they do not, this might just be an August of Wall Street quietly deciding what it thinks a growth multiple is worth. Either way, I am reading the two-year more than the S&P for a while yet.

📓 Desk Notes | Friday, July 17, 2026

Observations, not trades.

SESSION BRIDGE: prior session (Thu Jul 16) full reaction cash SPX -0.51% to 7,533.77 with Nasdaq -1.6% on the chip rout while TSMC’s Q2 beat and raise (2026 growth to slightly above 40%, capex $60-64B from $52-56B, +$100B Arizona) failed to lift the complex, 2yr held 4.16% (essentially unchanged from Wed’s 4.17%), 10yr 4.57%, VIX crept toward 17 through the cash session, then Netflix -8% after hours on a Q3 guide of $12.86B vs Street’s $13B and a tightened full-year range to $51.0-51.4B; live premarket ES -1.02% at 7,500.50, NQ -2.12% at 28,607.50, VIX +10.23% to 18.43 (first close above 18 since mid-June), BTC -1.63% to $62,732.50 tracking the equity risk-off, oil flat at $79.06, gold flat at $3,995.8, DXY +0.21% to 100.708; threshold: SOFT trigger (Nasdaq -1.6% Thursday, premarket ES -1.02% at the 1% investigate line, VIX +10.23% amplifying, NQ -2.12% amplifying further; carry-over fires).

1. The mechanism read (full)

What moved – the four instruments plus the tape.

- 2-year Treasury yield: 4.16% Thursday close (Wed close 4.17%, intraday low Wed 4.12%). The front end held its Wednesday reprice through Thursday’s soft data blackout and the TSMC print. September hike odds held near 48%. Real yields softer alongside nominal.

- 10-year Treasury yield: 4.57%, unchanged Thursday. The long end has ignored the front-end move for a second session. 10Y-2Y spread at +41bp, steepening bias intact.

- DXY: 100.708 (+0.21%) overnight, a mild bid consistent with positioning unwind and haven demand into the equity sell rather than a policy shift. Not a dollar-strength story; a de-risk story.

- VIX: 18.43 (+10.23%) overnight. First close above 18 since mid-June. This is the compression thread’s first genuine bid after riding through cycle 11 of the Hormuz book, the CPI/PPI double-print, the Warsh double-testimony, and the fourth night of Iranian strikes.

- Tape: SPX -0.51% Thursday, NDX -1.6%. Overnight ES -1.02%, NQ -2.12%. Chip complex extending Wednesday’s bleed. Netflix -8% AH. Gold flat, oil flat, BTC tracking tech beta.

What it implies – the causal read.

The story is not the front end (which held); it is the equity catching up to the front end. Wednesday’s move on soft PPI and Warsh’s Senate register took September hike odds off 22 points in seven sessions. Wednesday’s equity response was Apple-hits-ATH and Nasdaq +0.62%: the tape reading the dovish signal as tech’s rally. Thursday and overnight are the tape re-reading the same signal as tech’s revaluation. The trigger for the revision was TSMC’s beat and raise, read as “vendor commits to more supply into a demand story the market no longer believes at these multiples.” Netflix compounded the sell by giving the tape a second decelerating growth guide inside two quarters, at a lower multiple, from a different sector. Two “growth companies” delivering not-good-enough was enough to bid the VIX 10%. AI valuation is now the tape’s question, not AI demand.

The one artery. The tape decided that a monster beat-and-raise from the AI supply chain’s toll operator was a supply-side confirmation of the “customer capex is being redirected” thesis (the chipflation ledger’s live case), not a demand-side dismissal of it. Same data, opposite reading to the one bulls priced entering the print. TSMC’s $8B capex raise and $100B Arizona is what has to be earned back by hyperscaler revenue growth. The tape’s overnight message is that it is not confident that revenue growth is turning up.

2. Forward catalyst slate

Today, Friday Jul 17:

- Housing starts and building permits (June) at 08:30 ET.

- Import-export price index at 08:30 ET.

- Univ Michigan sentiment preliminary (July) at 10:00 ET.

- Fed’s Waller speaks 08:30 ET; Bostic 12:30 ET.

- Earnings before open: American Express, Truist Financial, Schlumberger, State Street, Regions, Fifth Third.

- The market wants to hear Waller and Bostic on where they land after Warsh’s Senate register.

Next week (the Mag7 guide window opens):

- Mon Jul 20: NAHB housing market index; Fed’s Williams speaks; Cleveland Fed CPI nowcast update.

- Tue Jul 22: Tesla Q2 after close (first Mag7 print in the adjudication window). Consumer confidence (July).

- Wed Jul 23: Existing home sales; Alphabet Q2 preview building.

- Thu Jul 24: Alphabet Q2 after close. PMI flash prelims (S&P Global). New home sales.

- Fri Jul 25: Durable goods orders.

Week after (peak):

- Mon Jul 27: Dallas Fed manufacturing.

- Tue Jul 28: FOMC day 1; consumer confidence.

- Wed Jul 29: FOMC decision, Warsh presser at 14:00 ET; ADP; Q2 advance GDP.

- Thu Jul 30: Meta Q2 after close, Apple Q2 after close; PCE prelim; jobless claims.

- Fri Jul 31: Amazon Q2 after close; ECI (Q2); Chicago PMI.

3. Divergence flags

Gold flat into a softer dollar and a fear-side VIX bid. Textbook: dollar down + risk off + rates flat = gold bid. Actual: gold +0.09%. Something is absorbing the safe-haven demand. Candidate absorbers: BTC (also selling), Treasuries (flat), USD reserve rotation quietly bidding the dollar despite the risk-off headline. This is the second consecutive session gold has failed to catch the bid the textbook prescribes.

BTC as tech beta, not haven. BTC -1.63% overnight tracks NQ -2.12% far more closely than DXY +0.21% or gold flat. Wednesday’s dovish front-end reprice did not lift BTC over $64K, and Friday’s risk-off did not break the range on the downside; BTC is trading with the growth complex, not the currency complex.

The AI trade’s supply chain divergence. TSMC (vendor, up 40% guide) is being sold on capex raise while hyperscaler customers (Apple, Alphabet, Meta, Amazon, Microsoft) still trade at growth multiples. The market is asking “who pays for the $8B capex raise?” and pricing an answer none of the vendors want to hear.

Netflix as growth-multiple canary. Decelerating guide + narrowed full-year + fresh 52-week low reads as a growth-multiple compression signal for the whole complex. Netflix and Big Tech share very little; growth-multiple stocks share almost everything with each other when the tape starts questioning valuation.

UnitedHealth as counter-signal. Boring healthcare beat and raise is catching a bid while the “growth” names sell. This is what rotation looks like in the first 24-48 hours, before it either accelerates or fades.

Part C: Regime tracking and the weathervane (MIP 10.6 §17)

⚓ Weathervane (persistent banner)

- UNCHANGED from Part 168; the first CHALLENGE mark on the Fed leg from Wednesday now paired with a NEW soft challenge on the AI-trade leg. Current read: “The Fed has turned hawkish for the cycle. The committee’s own dots flipped from a cut to a hike under Warsh, and higher-for-longer is now confirmed by the instrument. The unconfirmed second leg is risk appetite: equities are still trading as if the turn isn’t real.”

- Today’s note: The unconfirmed second leg took a live challenge this session. TSMC delivered exactly the print bulls needed to keep pricing the turn as unreal, and the tape sold it. Netflix compounded the message across sectors. VIX +10.23% is the fear-side finally noticing what the front end priced Wednesday. This is not the cruise ship turning; it is the second leg of the Weathervane finally being tested by the tape. Cruise ship still on heading.

- Rewrite rule: not satisfied. If TSMC’s follow-through is a Big Tech guide (Alphabet Jul 24) that names AI capex as a margin item, or a Fed speaker actively conceding a slower path before FOMC Jul 28-29, we start drafting. Sensitivity on both legs remains TIGHTER.

⚓ REGIME FLAG (internal tripwire)

- CONFIRMED on Warsh thread; chipflation thread ADVANCED via TSMC beat-and-raise being sold; vol regime compression BROKEN this session (VIX 18.43 exits the sub-18 compression band held since early June).

- Candidate threads worth watching:

- Chipflation as a regime story: CROSS-COMPLEX CONFIRMED. IBM Tuesday letter + Wednesday cross-section split + Thursday’s failed-vendor-rescue-by-TSMC = customer-side transmission is now the whole complex’s story, not one name’s story. Trigger for formal flag remains: two or more Mag7 July guides (Tesla Jul 22, Alphabet Jul 24, Meta Jul 30, Apple Jul 30, Amazon Jul 31, Microsoft, Nvidia) explicitly cite AI capex or memory cost as a margin item. TSMC’s message strengthens the case; the confirmation is with the customers.

- Vol regime compression: BROKEN. VIX 18.43 exits the sub-18 band held from early June through Wed Jul 15. Compression thread was TRIPLE-PRINT-TESTED to Wed; the breaking print is a Big Tech guide (Netflix) plus a chip sell despite a monster beat (TSMC). If VIX closes above 18 today, the thread converts from “compression regime” to “compression regime broken cycle 12”; if it fades below 17 today into the weekend, the break is a spike, not a shift. Watch the close.

- Fed hawkish-locked thesis: first CHALLENGE mark from Wed holds. No fresh Fed-side data today; Waller and Bostic speak. Trigger for formal flag remains: durable 2yr break below 4.10% or a Fed speaker actively conceding a slower path. Not met yet.

- Corporate Bitcoin treasury capitulation: unchanged. Strategy funded July’s coupon via MSTR dilution; sale count HOLDS at TWO for 2026. Saylor’s BIP-110 tweet fight continues in the background but is not moving the tape.

- Trump Accounts / OBBBA policy tell: still below threshold. No fresh evidence Thursday or overnight.

- Sensitivity read (§17.3): TIGHTEN to HIGH on the AI-trade / chipflation leg through Fri Jul 31 (Mag7 guide window peak). VIX compression sensitivity moves to HIGH (was tracked structural candidate; today may be the day the candidacy died). Fed-leg sensitivity holds HIGH through Alphabet Jul 24 and FOMC Jul 28-29. Recommendation to Phil: hold Weathervane through today; consider a rewrite of the “unconfirmed second leg” language if Tesla Jul 22 or Alphabet Jul 24 confirms AI capex as a Big Tech margin item.

- Public tell status: NOT triggered. “Hoist the mainsail, the macro winds have changed” remains holstered. Two live candidate triggers now with a third live: Tesla Jul 22 (chipflation), Alphabet Jul 24 (Big Tech capex confession), any Fed speaker confirming Warsh’s softer register before FOMC (Fed leg).