The Fed turned a 2026 cut into a hike and knocked every asset down at once. This morning equities recovered and gold, oil and bitcoin did not. Which reaction is reading it right?

⚓ Weathervane: The turn is confirmed. The Fed has dropped its easing bias and the dots flipped a 2026 cut into a hike (3.4% to 3.8%) while the war premium drains out of oil. Higher-for-longer is the regime now, not the risk. The cruise ship has come about.

Ahoy there, Trader! ⚓️

Ahoy there, Trader! ⚓️

It’s Phil…

Here is the question I could not put down this week, and it is the same one I left open in today’s News Edge: is that trio still down because the higher-for-longer regime is squeezing every dollar-sensitive asset, or because each just has its own baggage?

Let me walk the dots, because Wednesday was clearer than this morning.

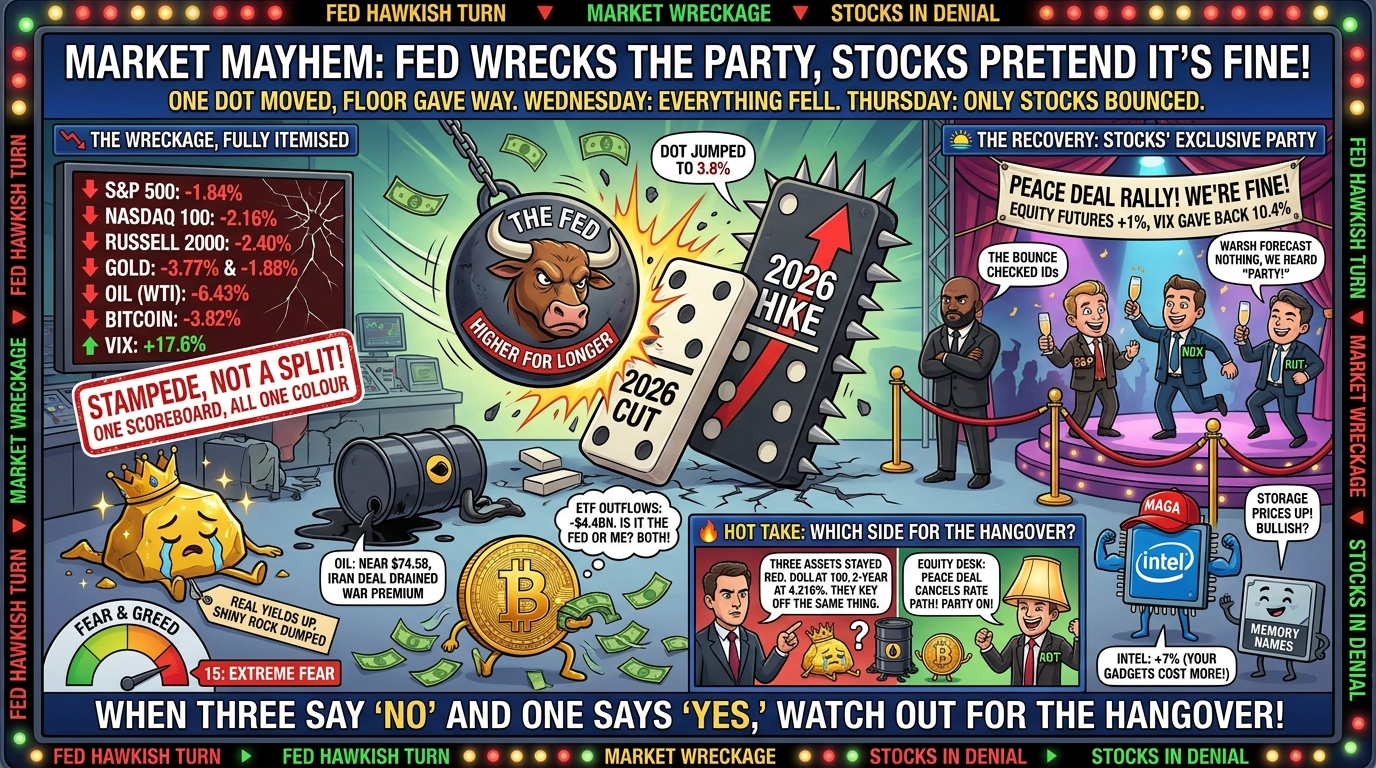

When the Fed turned hawkish at 2pm, it did not pick favourites. The median policymaker moved the end-2026 forecast to 3.8% from 3.4%, rewriting a planned cut as a hike. The 2-year Treasury yield, the bond market’s best guess at where policy goes next, jumped 16 basis points to 4.216%. The dollar climbed to 100 for the first time since March. And then everything fell together: the S&P future down 1.84%, gold down 3.77%, oil down 6.43%, bitcoin down 3.82%, with the volatility index up 17.6%. That is not a market having an argument. That is a market agreeing, all at once, that money just got more expensive for longer.

Here the textbook actually behaved. A hawkish surprise lifts the dollar and real yields, and a higher discount rate marks down everything that pays you later, from equities to the rock that pays no interest at all. Gold falling while the dollar surges is about as clean as macro gets. For once, reality and the textbook shook hands.

The puzzle is this morning. A peace deal got signed with Iran overnight, and equities recovered more than a percent while the fear gauge gave back its spike. But gold slipped another 1.88%, oil sat near $74.58, and bitcoin barely moved off $64,127. The recovery let stocks back up and left three assets on the floor.

So should I read the trio’s silence as proof the regime is still biting? Partly, and only partly. Here is where I keep myself honest: each of those three has a private reason to stay down. Bitcoin is bleeding a record run of ETF outflows. Oil is losing a genuine war premium that the Iran deal drains no matter what the Fed does. Gold is unwinding a crowded trade. I cannot crown them oracles when each has its own mess. But notice the common thread: all three key off the dollar and real yields, the dollar is pinned at 100, and the front end has not backed down. When the assets that share one sensitivity all decline to celebrate, and only the equity desk insists the storm has passed, the burden of proof sits with the equity desk.

The real signal is the confirmed turn, not the daily bounce. My lean is that the equity relief is the leg carrying the risk into July, when the next CPI either ratifies the dots or breaks them, and the gold and bitcoin non-bounce is part regime, part flow.

Happy trading,

Phil

Less Brain, More Gain

…and may your trades be smoother than a cashmere codpiece

P.S. – Phil’s Footnote. What nags at me is the timing and the breadth. Wednesday was honest. One decision, every asset down, the dollar up, the textbook for once doing what it says on the tin. This morning is the part I distrust. Stocks are treating a peace deal that signs on a closed market as if it cancels the rate path, and the assets that fell hardest have not been invited back up. I will not pretend gold and bitcoin are pure truth-tellers, because each of them has its own baggage this week. But they all answer to the dollar, the dollar is at 100, and the 2-year has not blinked. So I am watching the front end, not the futures, to tell me which side got this wrong. I have been early before.*

Desk Notes

Thursday, June 18, 2026 | Internal briefing, off the Wed Jun 17 close and the Thu Jun 18 pre-open. Observations, not trades.

1. Mechanism read

The driver is the Fed, and on Wednesday it drove everything the same way: down. The SEP did the thing the front end had been pricing for two weeks. The dot-plot median for end-2026 moved to 3.8% from 3.4% in March, converting a projected cut into a projected hike, with nine of 18 officials pencilling one and the 2027 median up to 3.625%. The statement was gutted in the same direction: easing bias and forward guidance out, the standing “deliver price stability” closer dropped. The institution itself confirmed the hawkish turn.

What matters for the read is that the reaction was broad, not selective. Every major future fell: ES 1.84%, NQ 2.16%, RTY 2.40%, YM 1.70%. Gold fell 3.77%, crude 6.43%, bitcoin 3.82%. The VIX spiked 17.6% to 18.84. The 2yr ripped +16bp to 4.216% (above the policy band top), the 10yr added +7bp to 4.487% (bear-flattening, so policy-tighter not growth-hotter), and DXY pushed to ~100, first since March. A hawkish surprise that lifts the dollar and real yields marks down every asset that promises cash later, and that is exactly what printed. Note the cash S&P closed -1.21%, but the ES future bled to -1.84% through the presser and overnight, so the futures are the truer reaction; do not anchor on the cash close.

This morning the reaction is selective. Equity futures recovered (ES +0.85%, NQ +1.34%, YM +0.52%, RTY +1.18%) on the overnight Iran MOU plus dip-buying, and the VIX gave back 10.35% to ~16.89. But the dollar-sensitive trio did not join: gold -1.88% (~$4,268), crude -0.57% (~$74.58), bitcoin -0.49% (~$64,127). Driving vs following: Wednesday the Fed drove everything. Today equities follow the geopolitics and positioning; gold/oil/bitcoin still follow the regime (DXY 100, 2yr 4.216%) and, in part, their own flows (see §3).

VIX: captured this run. 18.84 at Wednesday’s spike (+17.6%), back to ~16.89 today (-10.35%). The earlier “not captured” flag is cleared.

2. Forward catalyst slate

- Today (Thu Jun 18): weekly jobless claims and the Philly Fed print. Accenture (ACN) and Kroger (KR) earnings – ACN for enterprise-spend tone, KR for the consumer.

- Friday (Jun 19): the formal US-Iran signing in Switzerland – but it lands on Juneteenth, US cash markets CLOSED. The single biggest scheduled de-risking event prints on a tape nobody can trade; reaction deferred to Monday.

- The coiled one: physical Hormuz reopening is a Mon Jun 22+ event at the earliest, probably weeks of normalisation – Kpler has ~500 vessels still parked, 2 to 3 months cited to clear. The announcement is priced; not one extra barrel has physically moved. That gap is the watch.

- The claim about to be tested: July FOMC. Prediction markets have flipped to lean hike over cut for July. If the next CPI confirms the May 4.2% trajectory, the dots stop being a forecast and start being a schedule.

- Oil supply overhang: IEA flags a structural glut (+8m bpd supply by 2027 vs +2m demand). Even a fully reopened strait drips into a soft market, capping any war-premium snap-back – relevant to whether crude’s non-bounce is regime or just supply.

3. Divergence flags

- Wednesday broad vs Thursday selective (the headline flag). Wednesday was a stampede – every asset down on one decision. This morning only equities and vol-compression recovered; gold, oil and bitcoin stayed red. The tell is not that things fell (broad hawkish risk-off is textbook), it is that the recovery picked only equities. When the dollar-sensitive complex refuses to rebound while the dollar holds 100, the equity bounce reads as relief/positioning, not a genuine fade of the rate path.

- MIXED attribution – do not over-read the non-bounce as pure regime confirmation. Each of the three has its own reason to stay down: bitcoin is bleeding a record ~$4.4bn of ETF outflows (idiosyncratic), crude is losing a genuine war premium to the Iran deal (idiosyncratic, and the IEA glut caps it), gold is unwinding a crowded trade. BUT all three are also dollar/real-yield sensitive, and that common factor is the regime. Read: part regime, part baggage. The honest framing is that the equity bounce is the suspicious leg, not that gold/bitcoin are infallible oracles.

- Equities vs the bond market. Stock futures +0.85% to +1.34% while the 2yr sits at 4.216% and DXY at 100. Rates price tighter-for-longer; equities price relief. Late-cycle disagreement; the bond market is usually the one to believe.

- ETF outflows vs corporate accumulation. Spot-BTC-ETF net flows flipped negative for 2026 on a record ~$4.4bn streak, while Strategy keeps adding (846,842 BTC). One corporate buyer absorbing allocator selling – watch whether that holds.

- Chip cost-push read as bullish. Intel +7% (Apple onshoring) and memory +4-6% on a warning that hardware gets more expensive. A cost-push story trading as a growth story. Flag for whether it survives the peace-deal euphoria fade.

4. Regime status and sensitivity read

Weathervane: REWRITTEN this edition (first rewrite). The slow cruise ship came about. The Fed dropped its easing bias and the dots flipped a 2026 cut into a hike (3.4% to 3.8%) while the war premium drains out of oil. Higher-for-longer is now the stated regime, not the risk scenario. Note: Wednesday’s broad, all-asset selloff is a stronger confirmation of the turn than a stocks-only move would have been – the whole market repriced the same direction off one decision.

Regime Flag: TRIPPED. The soft flag raised Part 149 and sustained through 150 was waiting on the confirming instrument to print. Wednesday it printed, from the institution’s own hand, and the breadth of the reaction (equities, rates, dollar, gold, oil, crypto all in line) is the cleanest possible confirmation. Multi-week easing-bias pattern formally broken. Candidate for a higher-for-longer special report under Warsh.

Tight-or-loose read: the tripwire had been running slightly tight/hot by design (curious-newbie over-caution). On this event it is NOT premature – the dot plot plus an all-asset repricing is exactly the hard confirmation the soft flag was waiting for. A looser wire would have tripped here too. Treat the early-sensitivity caveat as resolved for this thread. Hand to the tiller for the special-report call. Public tell (“hoist the mainsail, the macro winds have changed”) stays HOLSTERED pending Phil’s greenlight.

5. Open data variables

- Pre-open levels keyed to the ~09:56 ET charts: BTC ~$64,127, gold ~$4,268, WTI ~$74.58, ES +0.85% / NQ +1.34% / YM +0.52% / RTY +1.18%, VIX ~16.89. Refresh at ~09:25 ET tomorrow’s-equivalent before any publish that slips.

- VIX now captured (18.84 Wed spike, 16.89 today). Prior “not captured” flag cleared.

- SEP core-PCE projection still conflicted across sources (3.3% vs 3.6%) – kept qualitative everywhere; settle the exact figure before it goes in any public number.

- Saylor/Strategy lifetime sale count still drifts (one source: second-ever / first since 2022); callbacks kept to the undisputed “swore never, then sold.” Verify vs the 8-Ks.

- Correction logged this edition: the first pass framed Wednesday as a stocks-vs-bitcoin split and omitted gold. The tape was a broad all-asset selloff; gold -3.77% was the cleanest dollar tell. Spine rebuilt around breadth-then-selective-bounce.