A weekend of US-Iran combat, eighteen dollars off gold, and a textbook reaction that arrived inverted on every instrument.

⚓ Weathervane. The Fed has turned hawkish for the cycle. The committee’s own dots flipped from a cut to a hike under Warsh, and higher-for-longer is now confirmed by the instrument. The unconfirmed second leg is risk appetite: equities are still trading as if the turn isn’t real. Today’s tape nudges it in place rather than turning it; the second leg still reads as in-progress.

Ahoy there, Trader! ⚓️

Ahoy there, Trader! ⚓️

It’s Phil…

Here is the central question this letter wants to walk. Should the safety bid be selling off on a weekend of US strikes on Iran and Iranian strikes on US bases?

Walk the dots.

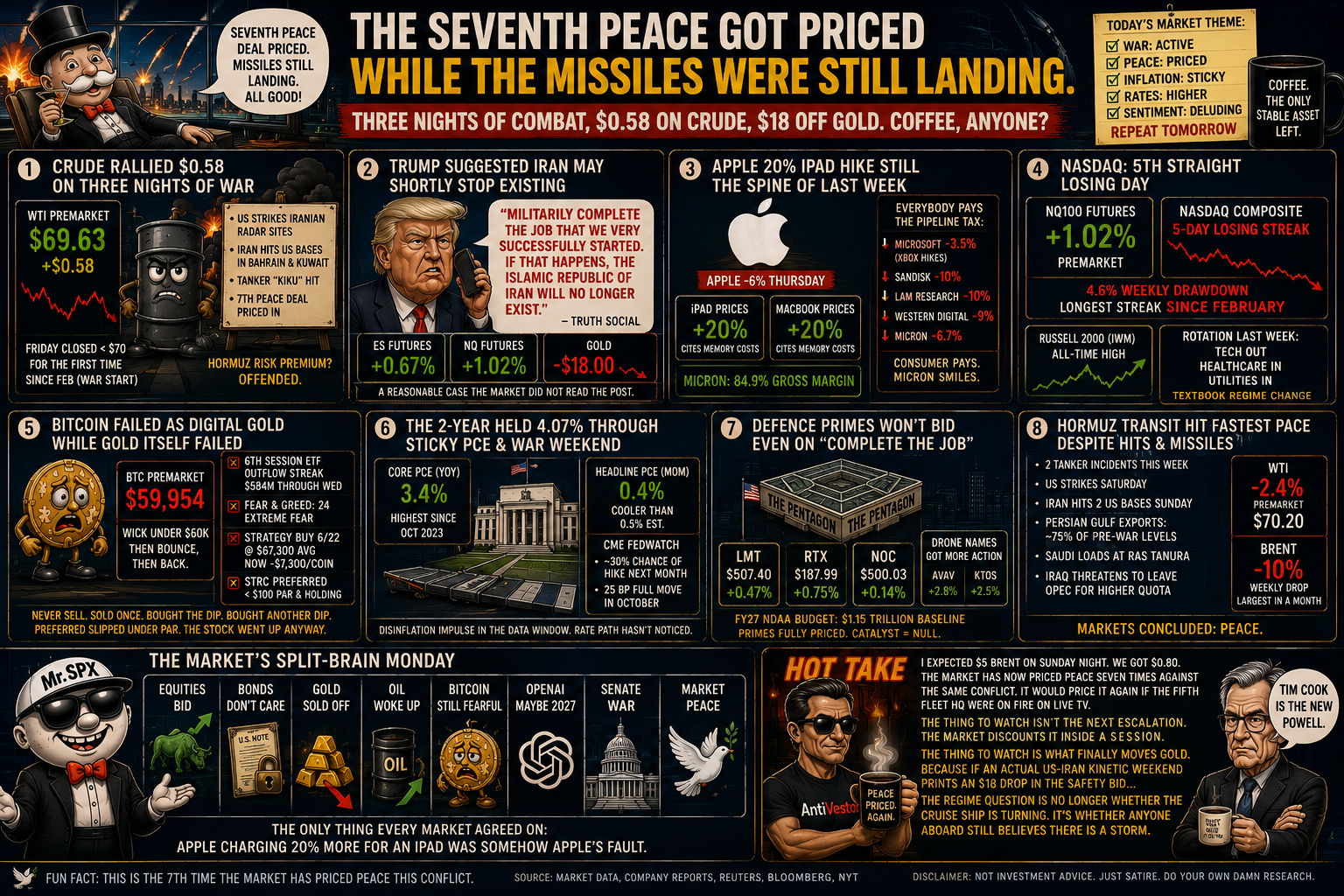

Saturday CENTCOM struck Iranian radar, comms, drone and minelayer sites after the KIKU tanker took a projectile. Sunday Iran fired ballistics at the US Fifth Fleet HQ in Bahrain and Ali Al Salem Air Base in Kuwait. Sunday night the President suggested on Truth Social that the Islamic Republic of Iran may shortly stop existing. The four instruments through it: two-year 4.07%, ten-year 4.38%, DXY 101.37, VIX 18.49. The fifth doing the real talking: gold $4,078, down eighteen dollars from Friday. WTI added fifty-eight cents. NQ gapped a percent. Vol shrugged.

Textbook vs reality.

The textbook reaction to a US-Iran kinetic weekend is the classic risk-off composite: oil rip, gold bid, equity sell-off, vol spike. The tape printed the inverse on every instrument. Crude lifted only fifty-eight cents and is still sub-$70. Gold actively fell. Equities bid up. Vol unchanged.

That is the textbook arriving wearing the wrong outfit. The question is whether the inversion is a stable property or a one-weekend anomaly. The cleanest read is that the Hormuz risk channel has been progressively de-priced across each escalation cycle this spring, and the market is now testing whether kinetic exchange itself is structurally de-priced too. Transit volumes recovered to about 75% of pre-war levels last week even with two tanker incidents. The supply story has stopped scaring anyone.

The bond and vol tells.

The two-year did not move through last Thursday’s 3.4% core PCE and did not move through the weekend strikes. FedWatch reads roughly 30% odds of a July hike and a full 25 bp move in October. Vol unchanged at 18.49 against an actual US-Iran kinetic weekend is the strongest evidence yet that the curve has fully digested the conflict.

Phil’s Musing

The market has gone past pricing peace and started pricing fatigue. The first six peace agreements were the optimism trade. This seventh one looks like the indifference trade. That is a different regime. If indifference holds through one more escalation cycle this week, the Hormuz complacency thesis upgrades from a candidate to a tracked thread, and the chart we should be looking at is gold against Brent rather than gold against the index. Watch what finally moves gold; if eighteen dollars off the safety bid is what an actual war weekend buys, the next mover may have to come from inside the rate channel.

Happy trading,

Phil

Less Brain, More Gain

…and may your trades be smoother than a cashmere codpiece

P.S. – Phils Footnote I genuinely expected $5 Brent on Sunday night, after the second night of strikes and Iran hitting US bases. We got eighty cents. I am still trying to talk myself out of the read above, because pricing-fatigue-as-regime is a strong claim and one weekend is one weekend. But the instruments line up too cleanly to ignore. If the cruise ship has not turned, the speedboat is doing a very convincing impression.

🗒️ Desk Notes | Monday, June 29, 2026

Raw briefing export. Observations not trades.

Live tape state

SESSION BRIDGE: prior session (Friday Jun 26) full reaction was a thin negative cash close inside a 2% weekly drawdown on SPX and 4.6% on Nasdaq Composite, with the Nasdaq logging a fifth straight down session; weekend tail dominated everything else as the US struck Iranian radar, communications and minelayer sites Saturday after the KIKU tanker hit, Iran fired ballistics and drones at the US Fifth Fleet HQ in Bahrain and Ali Al Salem Air Base in Kuwait on Sunday, and President Trump’s “complete the job” Truth Social post raised the escalation ceiling; live premarket ES +0.67% / NQ +1.02%, VIX +0.49% at 18.49, gold -0.44% to $4,078, WTI +0.58% at $69.63; threshold: SOFT (NQ in the 1.0% to 2.0% band, plus a manual catalyst flag fires on the weekend US-Iran strikes regardless of the index print).

1. Mechanism read

The four instruments. Two-year 4.07% Friday close, ten-year 4.38%, 10-2 spread holding near 31 bp. DXY 101.37 essentially flat at 101.366 premarket. VIX 18.41 Friday close to 18.49 premarket, effectively unchanged. Gold $4,096 close to $4,078 premarket, down 0.44%.

What moved. The premarket equity bid is the surface story. Underneath: the safety bid actively sold off through actual US-Iran kinetic exchange. The 2-year did not flinch through last Thursday’s sticky core PCE (3.4% YoY, monthly 0.4% cooler than the 0.5% consensus) and did not flinch through the weekend strikes. CME FedWatch is pricing roughly 30% odds of a Fed hike in July and a full 25 bp move in October; September hike odds firmed slightly on the PCE print without backing off.

What it implies. The mechanism is the same one the ledger has been tracking: hawkish-for-the-cycle Fed pricing held by a 2-year above policy rate, paired with equity leadership re-rating through chipflation (Apple -6% Thursday on a 20% iPad sticker, Microsoft -3.5% on Xbox hikes, Sandisk/Lam/Western Digital down 10% Friday). The weekend war did not move the rate channel, did not move the dollar, did not move vol. It moved gold downward, which is the cleanest no-flight-to-safety tell the cycle has produced.

The one artery. Gold -$18 to $4,078 on a weekend the US bombed Iran twice and Iran hit two US bases. This is the spine number. Equities up, oil up 58 cents, VIX flat, gold down: a single coherent read that the market has fully de-risked the Hormuz channel and is now testing whether kinetic exchange itself can be de-risked too.

2. Forward catalyst slate

Holiday-shortened week, payrolls moved to Thursday.

- Mon Jun 29 – No major economic data; calendar empty. Watch first cash session reaction to the war weekend.

- Tue Jun 30 – FHFA HPI (April), Chicago PMI (June), Consumer Confidence (June), JOLTS (May). Earnings: Nike, Constellation Brands.

- Wed Jul 1 – ADP Employment (June), S&P Global PMI Manufacturing final, Construction Spending, ISM Manufacturing (June). Earnings: General Mills.

- Thu Jul 2 – June nonfarm payrolls, unemployment rate, hourly earnings, average workweek, manufacturing payrolls, initial claims, durable orders final, factory orders. Moved up one day.

- Fri Jul 3 – US markets closed for Independence Day (250th anniversary).

Coiled threads:

- The Fed/2-year reaction function: if Thursday’s NFP prints hot (above ~175k consensus), September hike odds firm further; if soft, the disinflation-impulse-without-cut frame gets its first real test.

- The chipflation pipeline: next core PCE prints in late July and the July Mag7 guides (META, GOOG, MSFT, AMZN) are the adjudication window for Part B’s chipflation thesis.

- Hormuz risk channel: if the cease-fire framework fully reconstitutes this week, the WTI sub-$70 print holds; if Iran retaliates again against US assets, the test is whether the current complacency holds at $80 Brent.

- Strategy 8-K window: the next disclosure is the cleanest read on whether Saylor adds more contraries below his $67,300 average or holds.

3. Divergence flags

- Equities up, gold down, oil up 58 cents, VIX flat – on three nights of US-Iran kinetic exchange. The textbook reaction is the opposite move on every instrument. Single-edition divergence and the cleanest tell of the cycle.

- BTC failed as digital gold on the weekend gold itself failed. Both correlate to the downside only when both are selling; the “uncorrelated” thesis dies a little further.

- Defence primes did not bid into “complete the job” rhetoric. LMT/RTX/NOC barely moved Friday into the strikes; the NDAA $1.15T FY27 baseline is fully priced and active war is no longer a fresh catalyst for the primes.

- Last week’s rotation outran the index. Russell 2000 closed Friday at an all-time high on IWM while NQ100 lost 4.6% on the week. The breadth read and the leadership read are no longer telling the same story.

- Lilly +7.13% Friday on EU leukaemia therapy backing sat next to MU -6.7%. Healthcare took the leadership baton intra-day.

4. The carry-over note

Fires this run, both reasons: NQ +1.02% trips the SOFT threshold band, and a manual catalyst flag is justified by three nights of US-Iran exchanges and Iranian strikes on US Fifth Fleet HQ and Ali Al Salem Air Base.

The noteworthy thing. Markets had been set up to break risk-off on actual US-Iran kinetic exchange and shrugged. Gold falling eighteen dollars on the same weekend the US struck Iranian military infrastructure and Iran fired ballistics at the Fifth Fleet HQ is the precise inversion of the expected reaction. The expected-reaction-that-didn’t-show is the full safety bid.

How it rides the ladder this edition:

- AVE – snarky deflating nod in the cold-open (“considered the facts, delivered the opposite move on every single instrument”) and the teaser beat verdict.

- Snippet – HotTake one-liner about the Fifth Fleet HQ being on fire on live television and the market still pricing peace.

- Macro Edge – the full curious-Socratic dissection: textbook reaction is oil rip + gold bid + equity sell + vol spike, reality delivered the opposite on every instrument, walk why.

Part C – Regime tracking & the Weathervane

⚓ Weathervane status: UNCHANGED, second leg still in progress. Current read: “The Fed has turned hawkish for the cycle. The committee’s own dots flipped from a cut to a hike under Warsh, and higher-for-longer is now confirmed by the instrument. The unconfirmed second leg is risk appetite: equities are still trading as if the turn isn’t real.”

Today’s note for the Weathervane. Today’s premarket bid is precisely the “equities still trading as if the turn isn’t real” tell. The chipflation transmission story confirmed last Thursday is intact and last week’s de-risk rotation (tech out, healthcare and utilities in) is the regime question made visible. Today’s snap-back is the falsifier test: if it sustains and cap-weight S&P puts back through prior highs ahead of breadth this week, Part B’s “broad de-risk is repricing not position clearing” call gets marked-MISS. If breadth keeps leading and the snap-back fails inside two sessions, it confirms.

⚓ Regime Flag status: CONFIRMED on Warsh thread; no new flag. Chipflation candidate thread still held below the multi-week trigger; one Apple sticker is not yet a pattern. The new candidate worth watching this run: the Hormuz channel has now survived US-Iran kinetic exchange without re-pricing. If a second escalation cycle this week also fails to break $80 Brent, the “Hormuz is structurally de-risked” thesis fires as a new tracked thread.

Sensitivity read (§17.3): UNCHANGED, holding loose-leaning. Keeping the Hormuz complacency thesis as a Part B candidate rather than a fired regime flag is the tripwire working as designed. One weekend of failed risk pricing is suggestive, not a pattern. Phil to agree or instruct tighten/loosen.

Public tell status: NOT triggered. “Hoist the mainsail, the macro winds have changed” stays holstered.