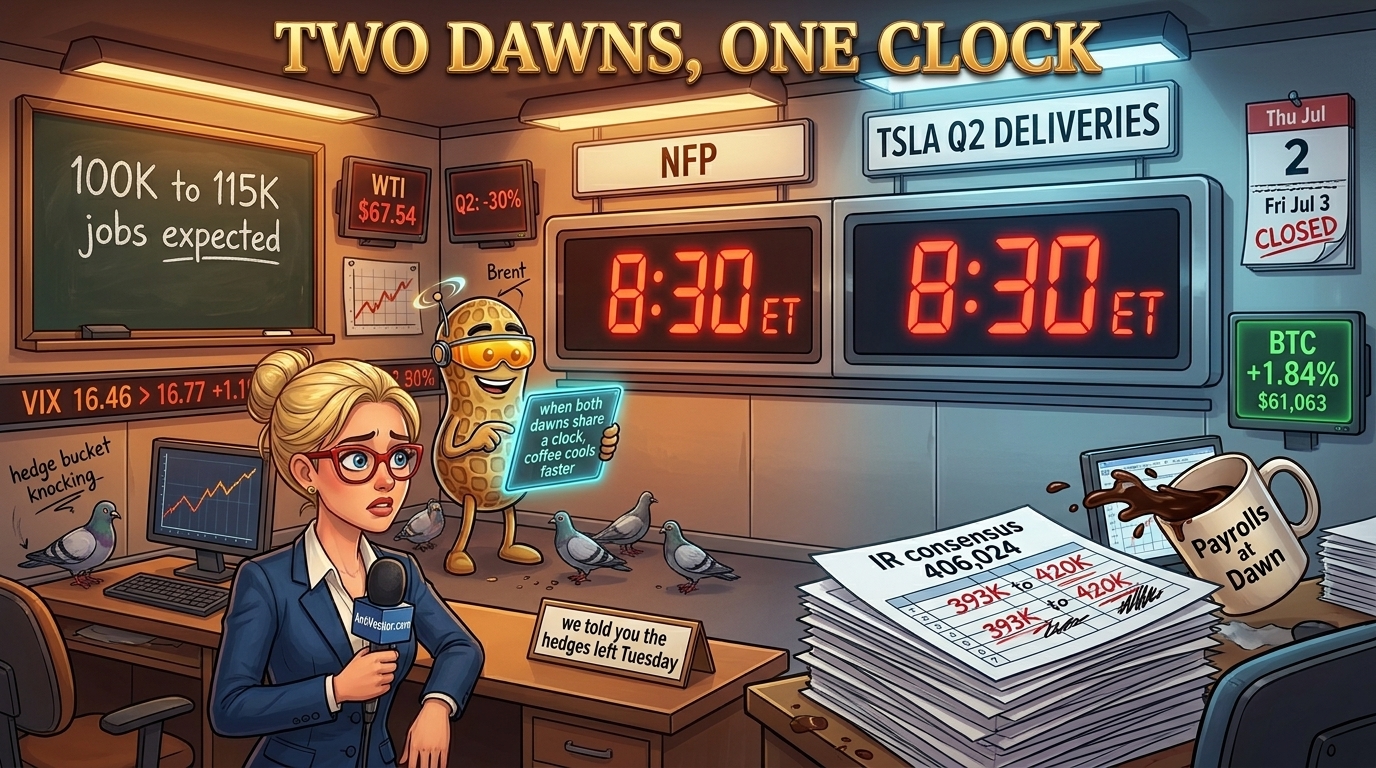

Two 8:30 prints share a clock, and only vol has the honesty to admit it.

Ahoy there, Trader! ⚓️

Ahoy there, Trader! ⚓️

It’s Phil…

Two Dawns, One Clock The hedge bucket walked out on Tuesday. This morning it started scratching to be let back in.

Wall Street rarely gets a calendar like this. Two of the year’s most-watched prints share an 8:30 ET clock this Thursday, and then markets shut on Friday for Independence Day observed. Payrolls first: consensus is 100K to 115K jobs on a 4.3% unemployment rate.

ADP came in soft at 98K on Wednesday, and the Fed chair told a room full of central bankers in Sintra that prices are too high, with the finality of a man announcing that water was wet. Tesla deliveries land in the same minute: the company’s own investor-relations page compiled 22 analysts to a consensus of 406,024 vehicles, and the sell-side happily sat 27,000 vehicles apart around that number, which is another way of saying that “beat” and “miss” are branding choices this morning depending on whose note the reader wrote down first.

Futures at 05:52 ET: ES +0.04%, NQ -0.37%, YM +0.17%, RTY +0.20%. Fine. Coiled, cordial, disinterested. The instrument that had an opinion overnight was VIX, up 1.15% to 16.77 after Tuesday’s 6.80% quarter-end crush and yesterday’s flat print. Small number. Correct direction. The hedge bucket is scratching at the door three sleeps early, and the door is not open yet.

The One That Mattered The room walked out of the protection trade on Tuesday. This morning it started asking for a coat back.

VIX 16.77 is not a number that dominates any newsroom banner this morning. It said something anyway. Tuesday’s 6.80% crush was the tape betting on a benign NFP three sleeps before it printed, and we planted a Part B flag against that call on the record.

This morning VIX ticked 1.15% higher on a fractionally red NQ and a fractionally green ES, three hours before the door opens. Neither index was leading; the hedge bucket walked in ahead of both. Which raises the question.

When the protection bid ticks back in before the print, is the hedge bucket admitting it walked out too early, or dealers just re-loading? We went down the rabbit hole in today’s Macro Edge. [link]

Collect Morning Income

– Learn More

Stock Market Edge

Two 8:30 prints, one coiled tape, and the calendar shuts the door on Friday. NFP consensus 100K to 115K; Tesla IR bar 406,024 vehicles; and VIX quietly nudging back.

Premarket snapshot:

ES +0.04% at 7,536, NQ -0.37% at 29,954, YM +0.17%, RTY +0.20% at 05:52 ET; VIX +1.15% to 16.77, holding just above Tuesday’s 16.46 crush low into the payrolls window. Wednesday’s cash close was SPX -0.22% at 7,482, Dow flat, NQ -0.66% as Tuesday’s chip leadership walked out.

Sector rotation:

Wednesday reversed the semi leadership without asking; SNDK -4%, MU -3%, MRVL -2%. Meta jumped 8.1% into the Warsh remarks, alongside GIS +8.8% and APP +7.6%. Data-centre losers were louder: NBIS -13.4%, CRWV -11.1%, GLW -10.4%. The Russell finished Wed at 3,012.59.

Earnings and guidance:

Tesla’s Q2 delivery number lands premarket with the IR consensus at 406,024 and the analyst range from 393K to 420K, so a headline in the middle is beat, miss and hold at once depending on which note the reader wrote down first.

Cross-asset nuance:

10-year finished Wed at 4.481%, up six bp; 2-year at 4.176%, up four; 30-year at 4.973%, up seven. Long end steepened, front end held. Gold +0.82% overnight at $4,077.90. WTI $67.54 through the Feb 27 gap; the war premium has gone home.

📊 There’s a level on SPX I’m watching closely this morning. My full analysis briefing has it – plus what happens if we hold it, and what happens if we don’t. [Read it here →]

Crypto Market Edge

Bitcoin bounces off Tuesday’s low; the institutional exit door kept opening in the same session. BTC +1.84% to $61,063; ETF outflows now six straight weeks; MSTR sell budget live.

Price snapshot:

BTC at $61,063 at 05:52 ET Thu Jul 2, up 1.84% in 24 hours; the Tue Jun 30 close was $58,700, the lowest print since early December. ETH held $1,595. SOL +2.7% Wednesday. Coinbase (COIN) finished Wed at $146.19, -3.6% on session.

Flows and positioning:

Spot Bitcoin ETFs posted a sixth straight week of net outflows, cumulative $5.94 billion drained. June alone was $4.5 billion, the worst month on record for the complex. Open interest is -18.72% over 30 days to $45.62 billion. Fear & Greed at 24, extreme fear.

Leadership and rotation:

Strategy MSTR closed Tue down 7.2% on the board’s own $1.25 billion at-the-market sell authorisation, its worst session in three weeks; the STRC 12% coupon record date opened Wed. BTC printed a seven-month low into the same session Strategy marked itself down on its own paperwork.

Catalysts and roadmap:

MiCA licensing came into force across the EU Tue, restricting unlicensed exchange access to member-state customers. FOMC meets Jul 28-29 next, markets pricing 60%-plus for a hike by September. NFP this morning is the front-loaded test of the September odds and the front-end trajectory in one print.

Collect Weekly Income

Learn More

TL;DR – The Bottom Line

- Two of the year’s biggest prints share the 8:30 ET clock this Thursday; the tape did not guess overnight, and VIX 16.77 was the only instrument with a view.

- Payrolls consensus 100K to 115K on 4.3%; ADP came in soft at 98K on Wednesday; Warsh’s Sintra encore said “prices are too high” and offered no path.

- Tesla IR consensus is 406,024 vehicles; the sell-side sits 27,000 vehicles apart around it, so a print in the middle is beat and miss at once.

- Crude closed the war-gap at $67.54, the lowest since the day before the war began; Brent booked Q2 down 30%, the largest quarterly fall since 2020.

- Bitcoin ticked $2,300 higher off Tuesday’s seven-month low, but six weeks of ETF outflows totalling $5.94 billion have not flipped positive, and MSTR marked itself down 7.2% on its own paperwork.

📌 Fun Fact

The World Cup arithmetic that made May’s payrolls print land 172,000 above forecast.

The BLS reported May 2026 nonfarm payrolls at +172,000 jobs, well above the +85,000 consensus. Leisure and hospitality contributed +70,000 of the beat, driven largely by food services and drinking places (+48,000). The World Cup group stages ran May 15 to June 3 across US host cities, and the resulting temporary hiring surge is now the working reference case for anyone modelling June today. If June comes in soft, the tournament will have paid for itself twice.

Meme of the Day:

Happy trading,

Phil

Less Brain, More Gain

…and may your trades be smoother than a cashmere codpiece

p.s. There are 3 ways I can help you…

- Option 1: Collect Morning Income (Just $12)

A complete guide to the Premium Popper system.

Written to be clear, concise, and immediately actionable.

>> Learn More Here

- Option 2: Collect Weekly Income (Just $12) –

A complete guide to the Tag ‘n Turn system.

>> Learn More Here

- Option 3: Join the Fast Forward Mentorship

>> Join the Fast Forward Mentorship – trade live, twice a week, with me and the crew.

PLUS Monthly on-demand 1-2-1’s

No fluff. Just profits, Tag ‘n Turn Pulse bars, Poppers, and Patterns that actually work.