One reading in the crow’s nest bid back in three sleeps before the print. The others are still holding their tongues. Which of them is right?

⚓ Weathervane: The Fed has turned hawkish for the cycle. The committee’s own dots flipped from a cut to a hike under Warsh, and higher-for-longer is confirmed by the instrument. The unconfirmed second leg is risk appetite: equities are still trading as if the turn isn’t real. (Unchanged; today’s tape did not nudge it.)

Ahoy there, Trader! ⚓️

Ahoy there, Trader! ⚓️

It’s Phil…

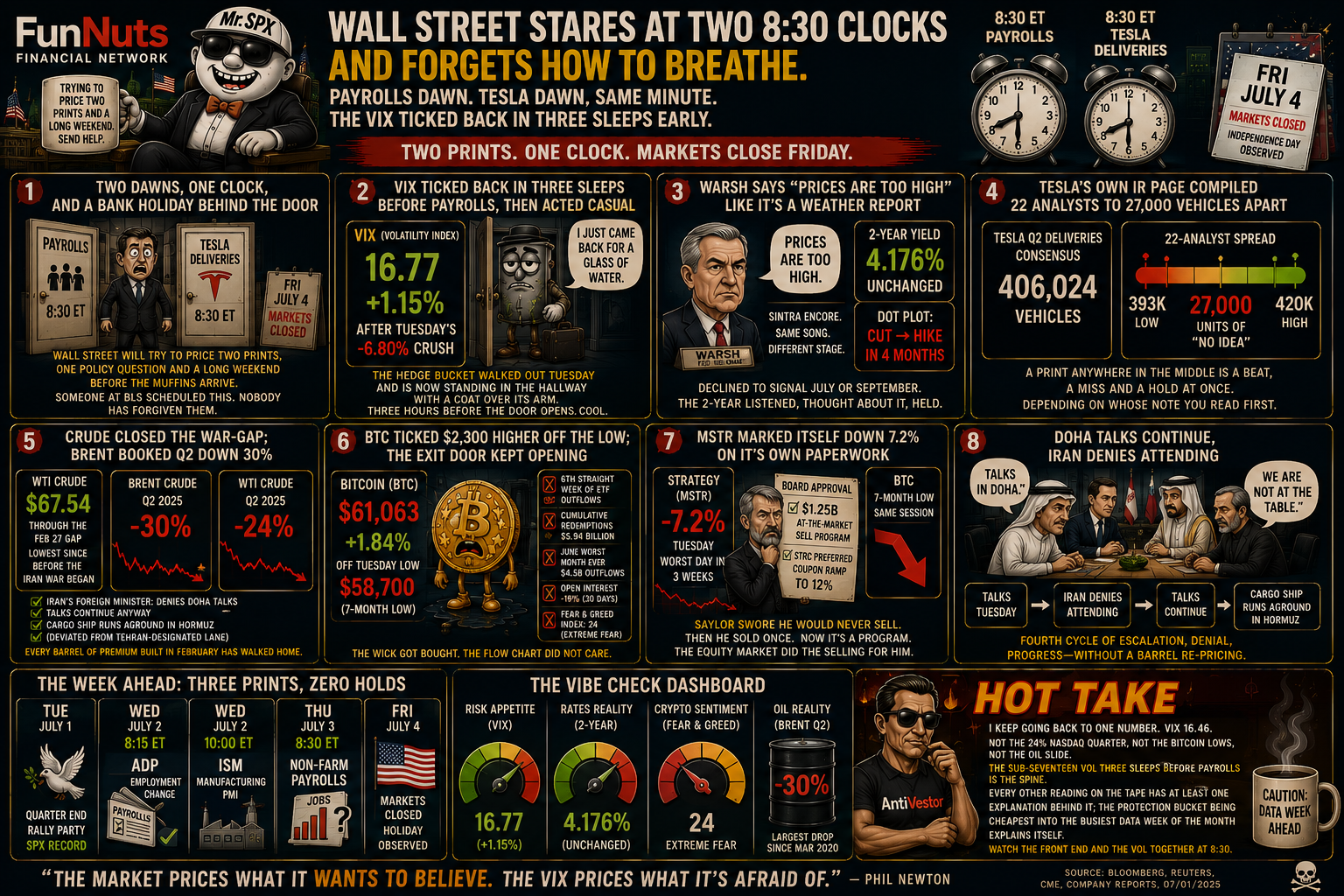

Two 8:30 ET prints share a clock this Thursday, then the market shuts on Friday for Independence Day observed. Payrolls consensus 100K to 115K jobs on 4.3%. Tesla’s Q2 delivery number lands in the same minute against an IR consensus of 406,024 vehicles. Futures at 05:52 ET had almost no view: ES +0.04%, NQ -0.37%. One instrument decided to say something anyway. VIX ticked 1.15% higher to 16.77 after Tuesday’s Q2-end crush of -6.80%, and the whole letter is about that one number.

So the question the tape has left open is this one. When the protection bid ticks back in before the print, is the hedge bucket admitting it walked out too early, or dealers just re-loading?

Textbook says vol behaves in a specific way into a scheduled, high-signal event. It should hold its range for a few sessions, then compress into the print itself as dealers finish positioning. What it should not do is walk out three sleeps in advance and start walking back in on the morning of. That is the shape of a positioning bucket that thought it knew, then thought again.

Walk the dots with me. Wednesday’s cash close had the long end lead: 30-year +7bp to 4.973%, 10-year +6bp to 4.481%, 2-year +4bp to 4.176%. That is a curve steepening on hawkish repricing, not on dovish expectations.

Warsh used his Sintra encore to reaffirm “prices are too high” while noting inflation expectations had eased. He declined to signal July or September. The 2-year listened and stayed above policy rate. WTI printed through the Feb 27 gap at $67.54, formally closing the trade opened on the day the Iran war began.

Gold gave back most of Q2’s give-up overnight, +0.82% to $4,077.90. And BTC bounced $2,300 off Tuesday’s seven-month low without a flow catalyst, on a day the ETF complex extended its outflow streak to six straight weeks.

What ties these threads is a single observation: yesterday’s tape did not corroborate Tuesday’s vol crush. The front end sat where it sat. The long end steepened hawkishly. Crude cracked further. If dealers really believed a benign NFP was three sleeps away, more instruments would have joined the vol crush. None did. Which brings us back to the door.

Phil’s Musing

The move that matters here is small in absolute terms and large in what it implies. VIX 16.77 sits inside the range the tape has held for two weeks; the fact that it ticked up rather than compressing further into the print is the first live test of the Part B call I planted on Tuesday. My working lean is that the vol crush was a positioning artefact of a quarter-end rebalance rather than a genuine view on payrolls. If that is right, the hedge bucket walking back in this morning is dealers admitting they were wrong to leave. The falsifier arrives at 8:30 ET. If the 2-year moves 5bp or more in either direction, the letter has to be rewritten.

If the vol bounce is confession, we should see the 2-year join in on the print. If it is dealers reloading, we should see vol fall again into 8:30. Watch the window between 05:52 and 08:29 ET.

Happy trading,

Phil

Less Brain, More Gain

…and may your trades be smoother than a cashmere codpiece

P.S. – Phils Footnote

I keep coming back to how quiet the room is. Two of the year’s biggest prints share a clock, and only one instrument decided to talk. When one instrument has the courage of its convictions and every other one is hedging, I want to listen to that one. On the record: I doubted the vol crush on Tuesday, and I am doubting the quiet on Thursday. If I am wrong on both, I would rather find out here than manage the position afterwards.

📓 Desk Notes – Part 160 | Thursday, July 2, 2026

Raw briefing for Analysis Edge. Observations not trades.

Live tape state (mechanical, §8.4)

SESSION BRIDGE: prior session (Wednesday July 1) full reaction ES -0.22% cash close, NQ -0.66%, 10-year +6bp to 4.481%, 2-year +4bp to 4.176%, WTI -1.3% to $68.58 fresh cycle low below the Feb 27 gap, VIX 16.63 flat after Tuesday’s 6.80% crush; live premarket 05:52 ET Thursday July 2 ES +0.04% / NQ -0.37% / VIX +1.15% to 16.77; threshold: SOFT. The prior session’s -0.22% cash close is comfortably sub-1% by itself, but the read is: (1) Tuesday’s Q2-end print left the protection bucket -6.80%, which is now testing live via a +1.15% premarket bid three sleeps before payrolls; (2) the twin 8:30 ET catalyst window (NFP + Tesla Q2 deliveries) is not priced overnight in either index; (3) crude at $67.54 has now printed through the Feb 27 gap left when the Iran war began. Read the premarket as a coiled reaction to Warsh’s Sintra hawkish encore plus the ADP miss, not a standalone view.

MECHANISM READ (full, §8)

What moved (Wednesday cash close)

- 2-year: 4.176%, +4bp on session. Still parked above policy rate. Two days from NFP.

- 10-year: 4.481%, +6bp. Rebounded from Monday’s 4.36% seven-week low.

- 30-year: 4.973%, +7bp. Long end led the steepening.

- DXY: advanced against major currencies Wed on Warsh’s “prices are too high” line; yen at 40-year low.

- VIX: 16.63 close Wed after Tuesday’s -6.80% crush to 16.45; VIX9D 13.73 (Tue close), VIX3M near 19.00 (contango pricing medium-term uncertainty ahead of Thu NFP).

- Equities Wed cash: SPX -0.22% at 7,482, Dow -0.03% at 52,305, NQ -0.66%, RTY -0.39% at 3,012.59.

- Crude Wed cash: WTI $68.58 (-1.3%), Brent $71.57 (-1.9%). Fresh cycle low; below Feb 27 gap.

- Gold Wed cash: $4,003.6 (-0.88%). Q2 wrap: gold -14%, worst quarterly performance since 2013.

- BTC Wed cash: ~$59,200, recovering from Tue $58,700 seven-month low.

- Premarket Thu 05:52 ET: ES +0.04%, NQ -0.37%, YM +0.17%, RTY +0.20%, VIX +1.15% to 16.77, gold +0.82% to $4,077.90, WTI -0.81% to $67.54, BTC +1.84% to $61,063.

What it implies

- Front end is not confirming the vol crush. VIX -6.80% Tue on a session when the 2-year still parked at 4.10% was the tape betting on a benign NFP with only one instrument saying so. The 2-year did not corroborate that view. Today’s premarket vol bounce (+1.15%) is the hedge bucket reintroducing itself before the door opens. Direction matters more than the level here.

- Long-end steepening (+7bp on 30-year vs +4bp on 2-year Wed) is consistent with a market unwinding the “peace priced” narrative that dominated the Q2-end rally, not with the front end capitulating to easing. That is a hawkish steepening, not a dovish one.

- WTI through the Feb 27 gap is not a fresh geopolitical event; it is the market formally closing the trade opened on the day of the war’s start. Every barrel of geopolitical premium built since Feb 28 has now walked out.

- BTC bounce off the Tue low is a wick-buying rebound, not a flow-reversal. ETF outflows are still running (six straight weeks). MSTR marked itself down -7.2% on its own sell authorisation Tuesday. Two failure modes converging on one filing schedule.

The one artery

VIX 16.77 +1.15% into the 8:30 ET twin catalyst window. The instrument that had a view overnight was the protection bucket, ticking back in three sleeps before payrolls. Small number, load-bearing direction against Tuesday’s -6.80% crush. Feeds the AVE cold-open, the one-number spine (§4.9), and today’s Macro Edge central question.

CARRY-OVER (§10.6, editorial)

Fires SOFT. The Tuesday Q2-end print left the tape with the biggest single vol move of the week going the wrong way relative to the calendar. Wednesday’s tape confirmed the ambiguity (VIX flat at 16.63 while long-end yields rose). This morning’s +1.15% VIX bid is the live test of the Part B call planted Tuesday (see ledger: “The protection bid walks out three sleeps before NFP”).

Ladder:

- AVE (dial 8+): the deflating nod in the cold-open. “The hedge bucket walked out on Tuesday. This morning it started scratching to be let back in.” The teaser beat sits with the central question.

- Snippet: the one-liner in the 📉 VIX section (“hedge bucket walked out the door on Tuesday and is now standing in the hallway with a coat over its arm”).

- Macro Edge: the full dissection. Textbook expectation is that vol holds its range into a known data window; a 6.80% crush on Tuesday against that expectation, plus a small bid today, is the tell that dealers positioned for a benign print without the front end agreeing. That is the “they thought X but it was really Y, because…” beat.

FORWARD CATALYST SLATE

- Thu Jul 2, 08:30 ET: June NFP. Consensus 100K to 115K jobs, 4.3% unemployment, AHE +0.3% MoM. ADP +98K Wed came in soft. September hike odds live.

- Thu Jul 2, 08:30 ET: Tesla Q2 deliveries. IR consensus 406,024, spread 393K-420K across the street.

- Thu Jul 2, 10:00 ET: June factory orders.

- Fri Jul 3: US markets closed for Independence Day observed.

- Mon Jul 6: ISM June Services PMI.

- Tue Jul 7: SpaceX joins Nasdaq-100 before open.

- Wed Jul 8: FOMC minutes; Levi Strauss earnings.

- Tue Jul 15: STRC preferred first semi-monthly payment (Strategy).

- Tue Jul 22: Tesla full Q2 earnings (post-close).

- Tue Jul 28-29: FOMC decision. Markets pricing 73% hold Jul, 65%+ for at least one hike by September.

- ~Aug 1 window: July Mag7 guides (META, GOOG, MSFT, AMZN) – the chipflation transmission live test.

DIVERGENCE FLAGS

- Vol vs front end. VIX -6.80% Tuesday with 2-year at 4.10% is the loudest current divergence. Dealers priced a benign print; the instrument that would agree did not move. Today’s +1.15% pre-NFP bounce starts to close the gap without resolving it.

- BTC price vs BTC flows. Bitcoin bounced 1.84% off Tue’s low; spot ETF outflows extended to six straight weeks and $5.94B cumulative in the same session. Price and flow are not the same trade this week.

- MSTR equity vs MSTR paperwork. Strategy filed a $1.25B sell program and the equity marked itself down 7.2% on the announcement, before a sale hit. The price is doing the selling that the program did not yet need to.

- Crude vs Doha talks. Iran’s foreign minister denied being at the Doha talks Tuesday; the talks continued anyway; crude added no premium and closed below the Feb 27 gap. Fourth cycle of “escalation-and-denial-and-progress” without a re-price.

- NQ vs the rest. Premarket NQ -0.37% while ES, YM, RTY are all slightly green. Tech-led leadership from Tuesday walked back out on Wednesday (-0.66%) and is not stepping back in this morning. Watch the semi complex reaction to today’s twin print.

Part C: Regime tracking & the ⚓ Weathervane (MIP 10.6 §17)

⚓ Weathervane (persistent banner)

UNCHANGED. “The Fed has turned hawkish for the cycle. The committee’s own dots flipped from a cut to a hike under Warsh, and higher-for-longer is now confirmed by the instrument. The unconfirmed second leg is risk appetite: equities are still trading as if the turn isn’t real.”

Today’s note: The equity disagreement leg gets a live test today at 8:30 ET. The vol crush on Tuesday and the small bid this morning frame the specific mechanism: dealers positioned for a benign NFP, and are now trying to re-hedge before it prints. The cruise ship has not turned; the speedboat is trying to price two prints and a long weekend at once.

Rewrite rule: not satisfied. The 2-year has not moved. The vol bounce is small in absolute terms.

⚓ REGIME FLAG (internal tripwire)

No new flag fired today. Warsh thread remains the CONFIRMED multi-week pattern break. Candidate threads status:

- Chipflation as regime story: below threshold. July Mag7 guides (starting ~Aug 1) remain the trigger.

- Hormuz complacency as regime story: below threshold but candidate strengthening. Iran FM’s public denial of the Doha format Tue plus crude closing below the Feb 27 gap Wed is the fifth cycle. One more clean cycle and this upgrades.

- Corporate BTC treasury capitulation: below threshold but candidate strengthening. MSTR -7.2% on its own paperwork plus BTC seven-month low in the same session adds price confirmation. Still need a second corporate filing.

- Vol regime compression at quarter-end: below threshold. Tuesday’s -6.80% was one session; today’s +1.15% bounce three sleeps before NFP is the first live test of whether the compression was structural or tape. Trigger: vol holds sub-17 THROUGH NFP AND through the FOMC Jul 28-29 without re-bid.

Sensitivity read (§17.3)

UNCHANGED, holding loose-leaning. Four candidate threads tracked as Part B shots rather than fired regime flags. Tripwire working as designed – Phil to agree or instruct tighten/loosen.

Public tell status

NOT triggered. “Hoist the mainsail, the macro winds have changed” stays holstered. The candidate for the next two weeks: NFP prints today that fails to ease September hike odds AND vol re-bids 20%+ on the day = the structural read upgrades and the public tell gets re-evaluated.