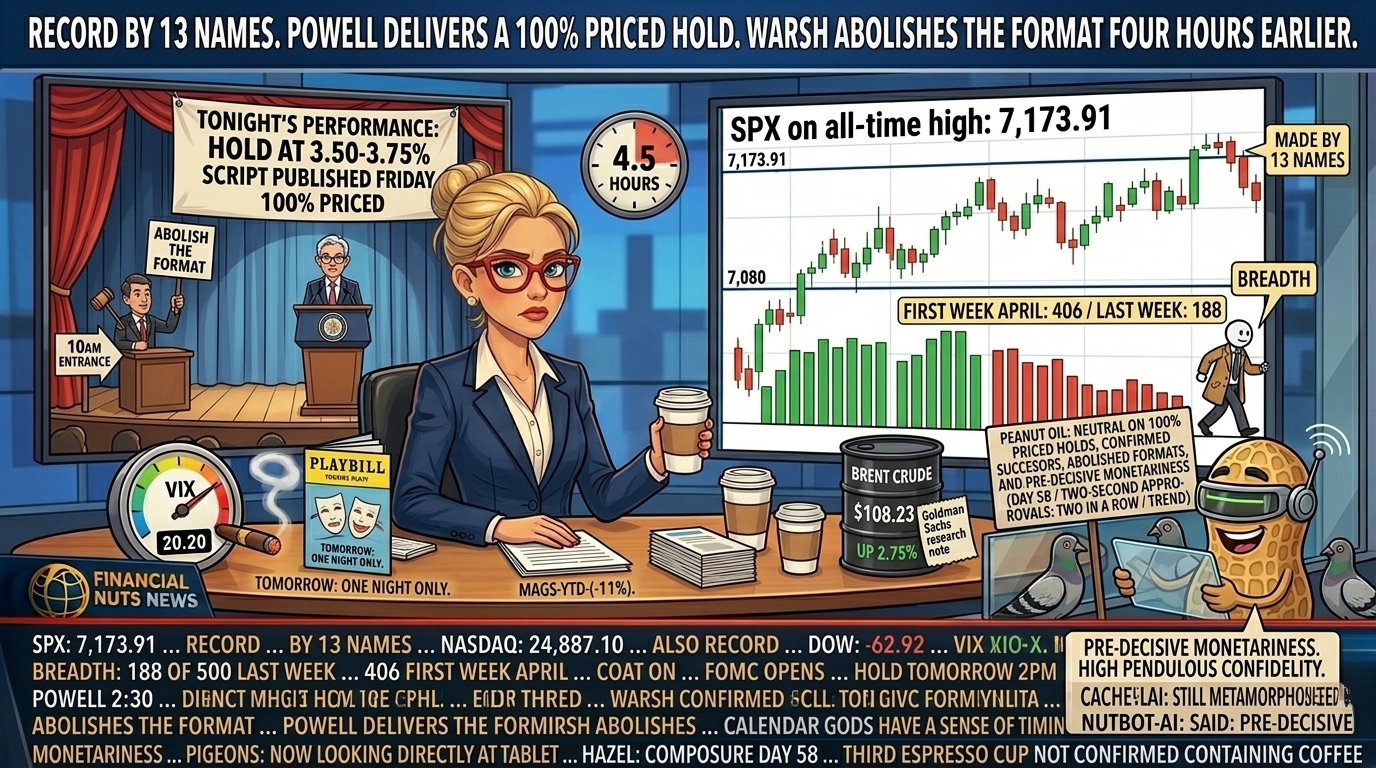

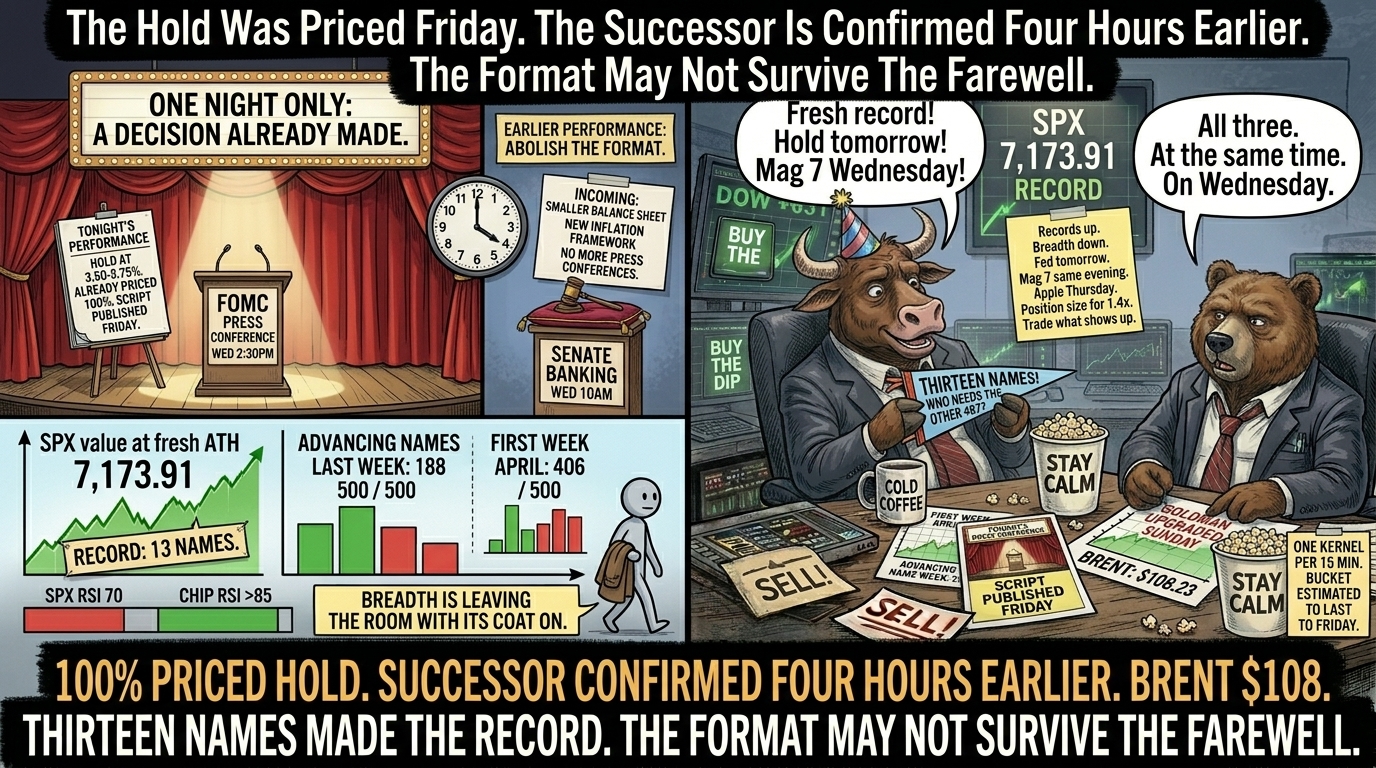

SPX 7,173.91 Monday Close. Fresh Record Made By Thirteen Names. Only 188 Of 500 Climbed Last Week Versus 406 First Week Of April.

The Breadth Is Leaving The Room With Its Coat On.

Ahoy there, Trader! ⚓️

Ahoy there, Trader! ⚓️

It’s Phil…

Tuesday morning. The SPX printed another record yesterday at 7,173.91, made by exactly thirteen names. Only 188 of the 500 climbed last week. The first week of April it was 406. The index is increasingly an S&P 13 with a 487-name supporting cast that has stopped supporting.

That is the cleanest divergence chart available between price and breadth, and it lands in the same week as the Fed, four of the Mag 7 reporting Wednesday after-close, and Apple plus PCE plus GDP plus ECB on Thursday.

Powell delivers a hold tomorrow. The futures curve already priced it at 100%. Wall Street has elevated central banking to theatre where the script publishes before opening night and the cast bows on cue. Four and a half hours before Powell reaches the lectern, the Senate Banking Committee will confirm Kevin Warsh as his successor. Warsh has spent his confirmation circuit telegraphing a smaller balance sheet, a different inflation framework, and the abolition of the regular post-meeting press conference. Including, presumably, the one Powell will be giving that afternoon. The format may not survive the farewell. The man may not survive his own format.

Brent punched above $108 yesterday, up 2.75%. Iran offered Hormuz back with conditions attached. Trump told them to call. Goldman marked up oil forecasts Sunday morning. Investment banks now charging for the war they couldn’t price.

Operationally, the SPX broke its compression range Friday and the ES carried the breakout into NATHs Monday. The cash followed yesterday and printed a new high. The two patterns I flagged Friday have resolved in favour of pattern 1, the textbook breakout pullback continuation. The question now is whether the breakout has the breadth to carry it through Wednesday’s binary.

RUT remains in its range. Same trade as yesterday. Sell premium outside the box until something new happens.

Records Up. Breadth Down. Fed Tomorrow. Mag 7 After. Apple Thursday. Sleep Optional.

Get The Complete Premium Popper System – Automation Included

Your entry ticket to consistent SPX income. Inside: the exact setup, rules, and checklists I trade daily – for less than the cost of lunch. Easily actionable.

Get The Premium Popper System – Click Here

Tuesday 28 Apr.

- Monday close: SPX 7,173.91 fresh ATH / Nasdaq 24,887.10 fresh ATH / Dow -62.92 (lagging) / 13 names made the SPX record

- Breadth: 188 of 500 advancing last week vs 406 first week of April / SPX RSI near 70 / chip RSI past 85

- Tuesday pre-market: ES little changed / Dow futures +64 / 10 of Monday’s 13 record names hit ATH alongside the index

- FOMC: two-day meeting opens today / Wednesday 2pm statement / Powell 2:30pm / hold at 3.50-3.75% priced at 100% / Warsh Senate Banking Committee confirmation Wednesday 10am

- Earnings pre-open Tuesday: UPS, GM, Coca-Cola, Visa, Spotify, T-Mobile, Booking / after-close: Starbucks, Robinhood

- Wednesday after-close: MSFT, META, AMZN, GOOGL, QCOM (one third of the index by weight on stage in a single evening)

- Thursday: Apple, Q1 GDP advance, core PCE, ECB

- Brent: $108.23 (+2.75%) / WTI tracking higher on Iran-Hormuz framing / Goldman raised oil forecasts Sunday

- Iran offered Hormuz back with conditions / Trump told them to call / blockade still active

- Mag 7 (MAGS) -11% YTD while index prints records / S&P 493 carrying the rally / now arguably the S&P 487 carrying it

- 30-minute SPX: bullish BO + pulse bar at the smaller consolidation / back bullish on the swings via short DTE BWB / NATHs 7,178.74

- 30-minute RUT: bearish range reversal + pulse bar at the range highs / sell premium with a bearish bias / range still grinding

Market Snapshot

- ES: ~7,210 / pre-market little changed / NATHs intact from Monday

- YM: Dow futures +64 / playing catch-up

- NQ: NATHs / Semis still doing the heavy lifting

- RTY: RUT range intact / NATH 2,828.7 above

- GC: Gold steady / inflation hedge bid

- CL: WTI bid on Iran framing / Brent $108.23

- VIX: Sub-20 still / suppressed into binary catalysts

- BTC: Consolidating below 80K

Tag ‘n Turn

SPX: Bullish break of the smaller consolidation on a pulse bar, taken Monday. Back on the swings via a short DTE Broken Wing Butterfly.

RUT: Bear pulse bar at the range highs. Sell premium with a bearish bias.

The grind continues into Tuesday and the compressions on the indices keep coiling.

Monday’s plans, looked at as part of Monday’s insiders group call, used the bull and bear theses for big picture moves and what was needed to rejoin the swings.

SPX needed a bullish break of the new even smaller consolidation, ideally on a pulse bar. It happened. Back bullish on a short duration DTE Broken Wing Butterfly.

RUT continues to grind out the range and with a new bear pulse bar at the range highs, it is time to again sell some premium, this time with a bearish bias.

SPX Analysis

Bullish BO + Pulse Bar at the smaller consolidation. Back bullish on the swings via a short DTE Broken Wing Butterfly. NATHs at 7,178.74 above. Target 7,182.84.

The smaller consolidation needed a bullish break, ideally on a pulse bar. The pulse bar arrived. The break confirmed. That is the trigger to rejoin the swings on a short DTE BWB.

The 30-minute compression keeps coiling tighter even as the daily NATHs print. Bull thesis remains outside the range. Bear thesis remains inside the range.

For premium poppers on the lower time frames, the same tiny range applies but on the 5-minute. The sensible read is to wait for the break out rather than take the usual opening range. That patience saved a lot of heartache yesterday as it did last week.

Current Status: Bullish Above 7,109.46 / PFZ Level 7,046.55 / Target 7,182.84 / NATHs 7,178.74

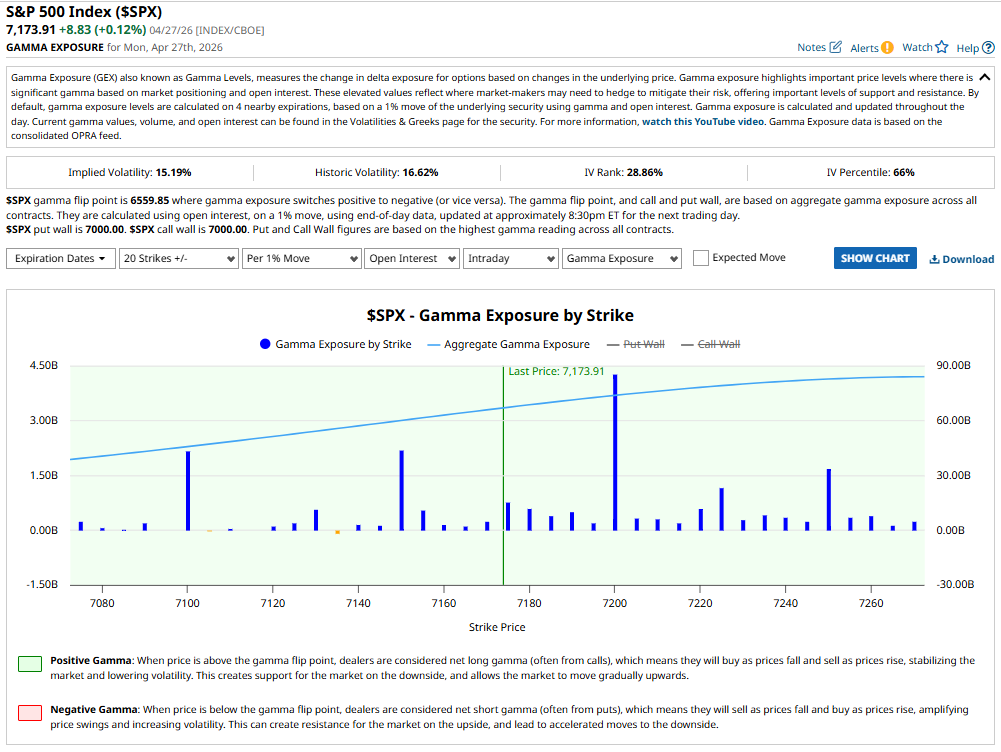

Gamma Exposure

GEX pin at 7,200. Put wall and call wall both 7,000. Gamma flip 6,559.85. IV 15.19% / IVP 66% / IV Rank 28.86%.

The GEX picture from Monday’s close shows 7,200 as the dominant call wall and the strike where the largest aggregate gamma exposure sits on the upside curve. 7,150 has a meaningful cluster acting as a secondary level. 7,250 sits above 7,200 with another sizeable spike.

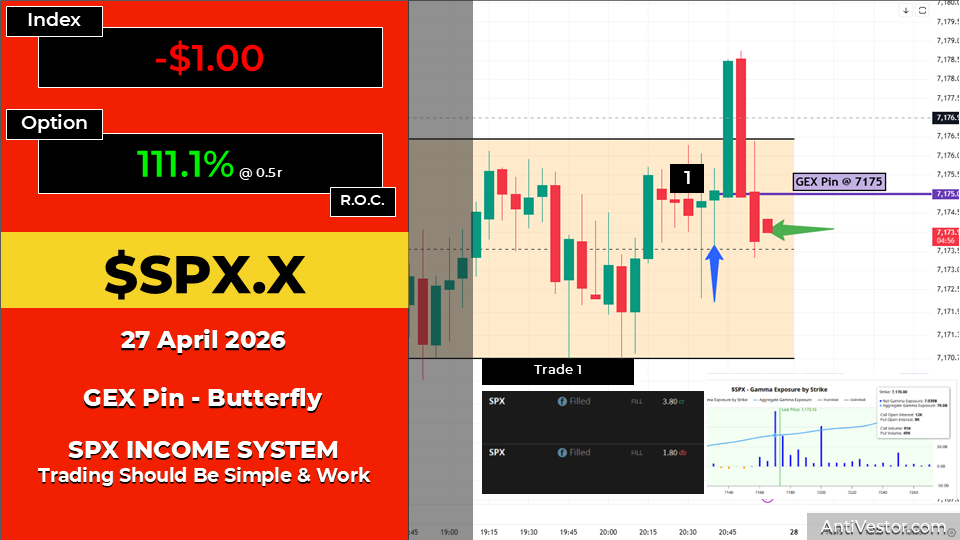

A late-day cheeky GEX-assisted trade on Monday: about 20 minutes before the closing bell, the 7,200 GEX pin combined with another intraday range suggested a close around that level. A Butterfly trade was used to zero in on the bullseye for 111.1% ROC. Quick punt, clean exit.

RUT Analysis

Bearish Range Reversal + Pulse Bar at the range highs. Sell premium with a bearish bias. Range still grinding.

RUT continues to grind out the range. A new bear pulse bar at the range highs is the trigger. Time to again sell some premium, this time with a bearish bias.

Bull thesis remains outside the range. Bear thesis remains inside the range. Until the range resolves, the bias is set by the most recent pulse bar at the boundary it tagged.

Current Status: Bearish Range Reversal + Pulse Bar at 2,800 / Target 2,765.66 / NATHs 2,817.95

Post Trade DeBriefing

Monday’s GEX-Assisted Butterfly: 111.1% ROC at 0.5r.

Cheeky little punt about 20 minutes before Monday’s closing bell. The 7,200 GEX pin combined with another intraday range was suggesting a close around that level. A Butterfly trade was used to zero in on a bullseye. Filled 3.80 cr / 1.80 db. 111.1% ROC at 0.5r. Quick clean exit.

Index P/L: -$1.00 (intentional small index figure on a precision strike).

Saved a lot of heartache yesterday by waiting for the break out on the lower time frames rather than taking the usual opening range. Same lesson as last week.

Rounding Off

The 13-name record. Yesterday’s SPX ATH was made by thirteen names. Only 188 of the 500 advanced last week against 406 the first week of April. The S&P 500 is, on a participation basis, increasingly an S&P 13. The Mag 7 sits -11% YTD while the index prints records. The 487 names not participating in this leg are the asymmetric risk into Wednesday: a Mag 7 print that hits could pull them back in, a Mag 7 print that misses leaves the index leaning on thirteen tickers and a Fed hold that’s already priced.

The Fed. Two-day FOMC opens today. Hold at 3.50-3.75% priced at 100%. Powell speaks at 2:30 Wednesday. Four and a half hours before Powell reaches the lectern, the Senate Banking Committee confirms Kevin Warsh as his successor at 10am. Warsh has telegraphed a smaller balance sheet, a different inflation framework, and the abolition of the regular post-meeting press conference. Powell will be giving the press conference Warsh wants to abolish, four and a half hours after Warsh is confirmed to abolish it. The format may not survive the farewell.

Hormuz. Iran offered the strait back with conditions. Trump told them to call. Goldman raised oil forecasts Sunday morning. Brent +2.75% to $108.23. Investment banks now charging for the war they couldn’t price seven weeks ago. The blockade still functionally active. The diplomacy still functionally absent.

The earnings block. Tuesday pre-open: UPS, GM, Coca-Cola, Visa, Spotify, T-Mobile, Booking. After-close Tuesday: Starbucks, Robinhood. Wednesday night: Microsoft, Meta, Amazon, Alphabet, Qualcomm. One-third of the index by weight reports in a single 36-hour window. Apple Thursday. PCE Thursday. GDP Thursday. ECB Thursday.

BTC. Below $80K. Consolidating. The break above $76K from earlier in April that triggered a reassessment has not produced a directional move. Range trade until something new develops.

Current Status: SPX records on 13 names / breadth deteriorating / FOMC tomorrow with successor confirmed first / Mag 7 same evening / Apple plus PCE Thursday / Brent $108 / oil bid on Hormuz / RUT still ranging

Expert Insights

“The market can stay irrational longer than you can stay solvent.”

— John Maynard Keynes (often paraphrased and possibly apocryphal in this exact form, traceable to Gary Shilling who attributed it to Keynes in 1986)

The SPX is at fresh ATH. The breadth is deteriorating. The Fed is delivering a hold the curve already priced. The successor abolishes the post-meeting format four and a half hours before the meeting concludes. Brent is at $108 on a deal that has not been signed.

Each of those facts on its own would be a tradeable observation. Together they describe a market that has decided several things are simultaneously true that historically have not been simultaneously true. That market may be right. That market may also be irrational for longer than is comfortable.

The job this week is not to bet on which of those facts gets resolved first. The job is to position size for a 1.4x volatility expansion across Wednesday and Thursday and let the chart confirm whichever fact resolves.

[Source: Gary Shilling, Forbes, 1986, public |

Federal Reserve FOMC schedule, public |

CBOE VIX historical volatility expansion data, public |

SpotGamma GEX data, 28 April 2026, spotgamma.com]

Percy and The NutBot Report

(Peanut-Powered Analysis)

(Peanut-Powered Analysis)

Percy has fed the FOMC eve setup, the breadth divergence, and the Warsh confirmation timeline into NutBot-AI. The tablet emitted a Beep-Beep. The three sourced points came back accurate. Percy has described the situation to the newsroom as “a pre-decisive monetariness with high pendulous confidelity,” which is not a phrase. Nobody has corrected him. NutBot-AI has no opinion. The press-pigeons have stopped looking at each other and have started looking at the tablet directly, possibly hoping it will help.

Beep-Beep. (repeated by Percy)

1 – The S&P 500 closing at a fresh all-time high of 7,173.91 on Monday with only 188 of the 500 components advancing last week (compared to 406 in the first week of April) and 13 names producing the headline record represents one of the narrowest breadth profiles to accompany an index ATH in the post-2020 cycle. [Source: S&P Dow Jones Indices breadth data, public | Bloomberg historical advance-decline data, public, 28 April 2026]. Historical precedent for indices printing records on sub-200 advancing components in a 500-name basket suggests these conditions resolve either with the laggards rotating in to broaden the rally or with the leadership rolling over to meet the laggards in retreat. The Wednesday/Thursday earnings block represents the closest available catalyst to force the question.

2 – The Senate Banking Committee scheduled to confirm Kevin Warsh as Federal Reserve Chair at 10am Wednesday, four and a half hours before Jerome Powell delivers the FOMC press conference at 2:30pm, places Powell in the institutional position of conducting a press conference his confirmed successor has publicly committed to abolishing. [Source: Senate Banking Committee schedule, public | Federal Reserve FOMC press conference schedule, public | Kevin Warsh public confirmation hearing testimony, public]. Warsh’s stated framework includes a smaller Fed balance sheet, a revised inflation targeting approach, and the elimination of regular post-meeting press conferences as a communication tool. The 100% priced hold for Wednesday’s decision reduces the rate-path component of the meeting to formality, leaving the press conference itself as the primary information event. This may be the last regularly scheduled FOMC press conference before format changes are implemented.

3 – Brent crude at $108.23, up 2.75% Monday on Iran’s conditional Hormuz reopening offer that Trump declined to engage with, combined with Goldman Sachs raising oil forecasts Sunday and SPX RSI near 70 / chip sector RSI past 85, places the breakout-record narrative against an inflation-impulse backdrop with technically extended momentum. [Source: ICE Brent crude futures, public | Goldman Sachs commodities research note, 27 April 2026, public | Standard RSI calculations on SPX and SOX indices, public]. The asymmetric risk is the simultaneous combination of a hawkish-leaning successor confirmation, a 100% priced hold that allows for surprise on the Powell statement language rather than the rate decision, four major tech earnings, and an oil price level last seen in early 2024. Any one of these could move the tape. The probability of all four moving together in a directionally-aligned way is materially higher than the probability of any one alone.

Beep. (Percy nods as though he follows.)

This Bot potentially hallucinates. Maybe. OK, Probably! The FOMC Eve and Warsh Confirmation Risk Assessment is 22 pages. Percy has added Appendix E, which is a list of words Percy believes describe the simultaneous-binary-events condition, including “convergencitude” and “multiplicitivity.” Neither is a word. Peer review submitted to NutBot-AI by Percy. Approved in two seconds. The two-second record from yesterday has been re-equalled. Percy is pleased. Percy has noted that two consecutive two-second approvals constitute a trend.

In Other News…

The S&P 500 made a record yesterday on thirteen names. The other 487 are doing something else. Last week 188 of the 500 advanced. The first week of April it was 406. The breadth is leaving the room with its coat on while the index waves from the stage.

Today the FOMC opens. Tomorrow at 10am the Senate Banking Committee confirms the man who wants to abolish the press conference Powell will deliver four and a half hours later. The cast bows. The script publishes. The format may not survive the farewell. The man may not survive his own format.

Powell is delivering a decision the futures curve already made. 100% priced. Zero suspense. Wall Street has elevated central banking to theatre.

Iran offered the strait back with conditions yesterday. Trump told them to call. Goldman raised oil forecasts Sunday morning. Brent up 2.75% to $108.23. Investment banks now charging for the war they couldn’t price.

Tuesday pre-open: UPS, GM, Coca-Cola, Visa, Spotify, T-Mobile, Booking. Wednesday night: Microsoft, Meta, Amazon, Alphabet, Qualcomm. The seven Mag names that dragged MAGS down 11% year-to-date are about to tell the rest of the year what AI capex actually buys, presumably in the same tone.

Apple Thursday. PCE Thursday. GDP Thursday. ECB Thursday.

The market is sub-20 VIX into all of this. SPX RSI near 70. Chip RSI past 85. The breadth has left, the breadth has its coat on, the breadth is asking the doorman where the cars are parked. The index is on stage taking its bow.

Hazel’s Take:

Tuesday 28 Apr. SPX 7,173.91 Monday close at fresh ATH made by 13 names / Nasdaq 24,887.10 also record / breadth: 188 of 500 advancing last week vs 406 first week April / SPX RSI 70 / chip RSI 85 / SPX bullish BO + pulse bar at the smaller consolidation / back on the swings via short DTE BWB / RUT bearish range reversal + pulse bar at range highs / sell premium with bearish bias / FOMC opens today / Wednesday 2pm hold 100% priced / Powell 2:30 / Warsh confirmation 10am same day / format may not survive the farewell / MSFT META AMZN GOOGL QCOM Wednesday after-close / Apple plus PCE plus GDP plus ECB Thursday / Brent $108.23 +2.75% / Iran offered Hormuz back, conditions attached, Trump told them to call / Goldman raised oil forecasts Sunday / VIX sub-20 / BTC below 80K / Phil’s GEX butterfly 111.1% ROC into Monday’s close / composure day 58. The second smaller espresso has acquired a third companion.

Rumour Has It…

Hazel has updated the calendar. FOMC start today in red. Wednesday 10am Warsh in red beside Wednesday 2pm Powell in red. Thursday is now four shades of red in a single column for Apple, GDP, PCE and ECB. The calendar has run out of red and Hazel has switched to a deeper red borrowed from a different pen set. Day 58. The double espresso has now been joined by a second smaller cup and a third even smaller cup arranged in descending order. She has not commented on the third cup. The third cup has not been confirmed as containing coffee.

Wallie at the chalkboard. Today’s entries: “SPX RECORD: 13 NAMES” (one underline, considered, applied with reservation). “BREADTH: 188 OF 500 LAST WEEK / 406 FIRST WEEK APRIL” (two underlines, applied to the second number rather than the first). “POWELL: TOMORROW 2:30. HOLD 100% PRICED.” (no underlines, the chalk hovered and moved on). “WARSH: TOMORROW 10AM. ABOLISHES THE FORMAT.” (three underlines, instant). Below the list: “PHIL’S FOREHEAD: HEALING.” Two underlines.

Kash at the streaming desk, standing. Six timers now active: FOMC start (today), Warsh confirmation (tomorrow 10am), FOMC announcement (tomorrow 2pm), Powell press conference (tomorrow 2:30pm), Mag 7 block (tomorrow after-close), Apple plus PCE plus GDP plus ECB (Thursday). The ceasefire-indefinite timer has been retired for the week on grounds that six active timers is enough and the ceasefire timer would just be confusing. Stream title: “FOMC EVE / WARSH AT 10AM / POWELL AT 2:30 / SAME DAY / SLEEP IS BACK ON THE TABLE FOR FRIDAY.”

Mac on location. Flak jacket on. The St Petersburg notebook page now has a sub-page titled “GOLDMAN COMMODITIES NOTE / SUNDAY UPGRADE.” Mac has noted that the same investment banks that did not price the war are now pricing the consequences. He considers this professionally interesting. Local breakfast adequate. Return flight destination still unconfirmed. He has been asked twice. He has not answered either time.

Percy in the centre of the room. NutBot mode. Amber visor on. Antenna spinning. Holographic tablet displaying the 22-page FOMC Eve and Warsh Confirmation Risk Assessment with Appendix E (the list of words Percy thinks describe simultaneous-binary-events conditions, none of which are words) visible. Three press-pigeons have stopped looking at each other and are now looking directly at the tablet, possibly hoping it will help. Percy is describing the setup as “a pre-decisive monetariness with high pendulous confidelity.” Two-second peer review re-equalled. Percy has declared two consecutive two-second approvals a trend.

Phil at the back of the newsroom. Sunglasses still on indoors. The forehead has progressed from third-degree to second-degree, which Phil has counted as a win. The legs remain milk-white. He has explained that the burns are healing on a fixed timeline and the legs are healing on no timeline at all because they were never burnt to begin with. Nobody has questioned this.

The empty Cachè-AI terminal is still in the corner. The “PROMOTED” sign is still there. The terminal has been off for four days now. Nobody has commented.

This is entirely made-up satire. Probably!

Breaking scoops courtesy of the Financial Nuts Newswire-because who needs sanity?

Fun Fact:

The S&P 500’s closing record on 27 April 2026 of 7,173.91 was produced by only thirteen of the 500 component stocks advancing on the day, and from a weekly breadth perspective only 188 of 500 components closed positive last week against 406 in the first week of April 2026.

Historical FactSet and S&P Dow Jones Indices data show that all-time-high closes accompanied by sub-40% weekly advancing-component breadth occur in fewer than 5% of ATH sessions over the past three decades and statistically resolve within 30 trading days either through a meaningful broadening of participation as the laggards rotate in, or through a leadership reversal as the index rolls back toward the laggards.

[Source: S&P Dow Jones Indices, public |

FactSet historical breadth data, public |

Bloomberg index advance-decline historical data, public]

The cleanest forward catalyst available to force the question is the Wednesday/Thursday Mag 7 plus Apple earnings block. The 487 names that have not been participating either get a reason to or do not.

Meme of the Day:

Happy trading,

Phil

Less Brain, More Gain

…and may your trades be smoother than a cashmere codpiece

p.s. There are 3 ways I can help you…

- Option 1: The SPX Income System Book (Just $12)

A complete guide to the system.

Written to be clear, concise, and immediately actionable.

>> Get the Book Here

- Option 2: Full Course + Software Access – 50% off for Regular Readers – Save $998.50

Includes the video walkthroughs, tools for TradeStation & TradingView, and everything I use daily. Plus 7 additional strategies

>> Get DIY Training & Software

- Option 3: Join the Fast Forward Mentorship – 50% off for Regular Readers – Save $3,000

>> Join the Fast Forward Mentorship – trade live, twice a week, with me and the crew. PLUS Monthly on-demand 1-2-1’s

No fluff. Just profits, pulse bars, and patterns that actually work.