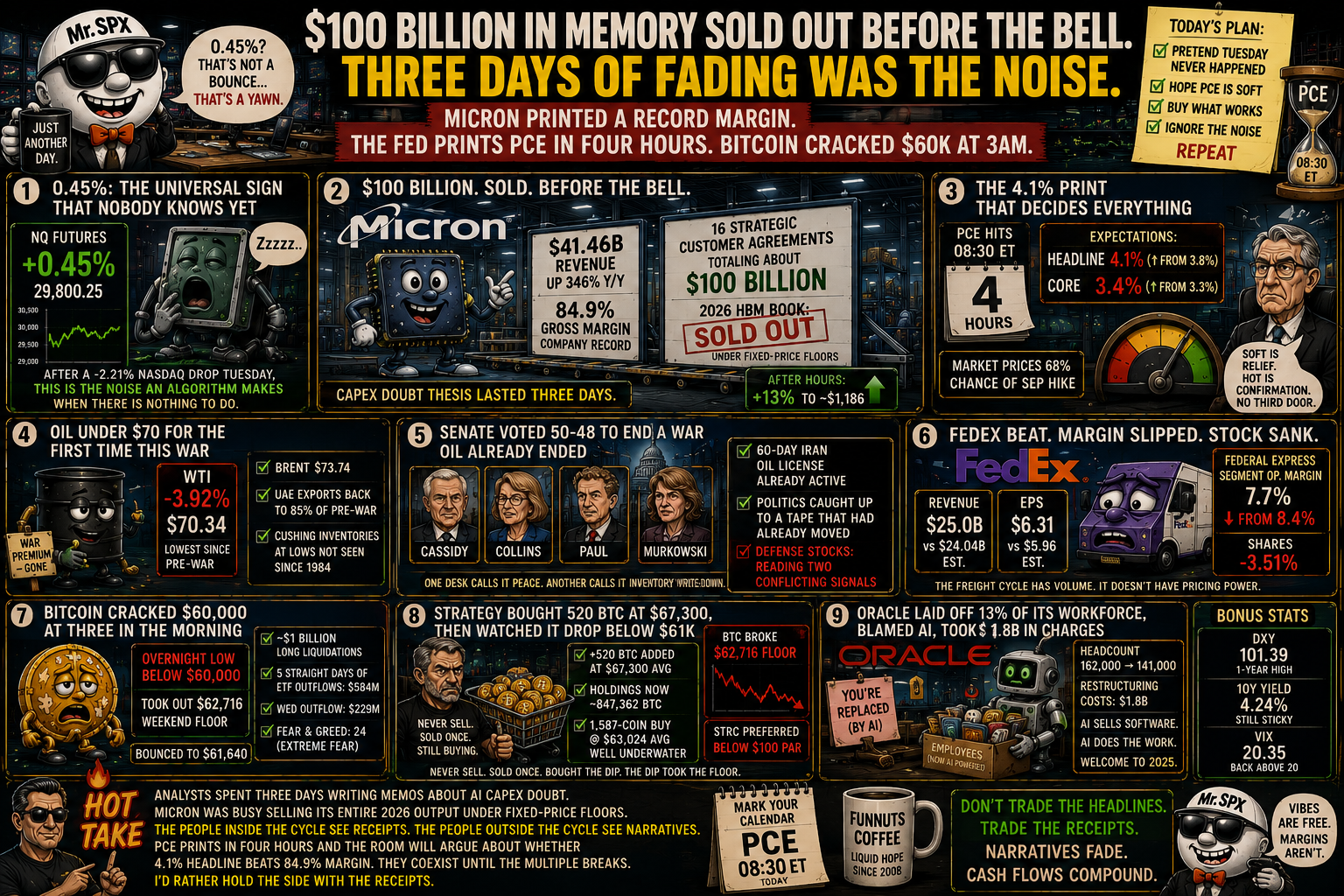

Wednesday night sold the entire 2026 AI memory book at floor prices. Thursday morning the Fed’s preferred gauge prints into a tape that already half-prices a hike. Which signal wins, and which textbook is right?

⚓ Weathervane (unchanged). The Fed has turned hawkish for the cycle. The committee’s own dots flipped from a cut to a hike under Warsh, and higher-for-longer is now confirmed by the instrument, not just the front end. The unconfirmed second leg is risk appetite: equities are still trading as if the turn isn’t real. Today’s note: Tue–Wed’s broad de-risk had begun the equity-side confirmation; one Micron print pulled NQ back up violently, but ES +0.75% and RTY +0.24% mean the repricing is only partially unwound. The banner does not rewrite, the read is one PCE print away from doing so either way.

Ahoy there, Trader! ⚓️

Ahoy there, Trader! ⚓️

It’s Phil…

The wind shifted twice in fourteen hours yesterday, and we want to read the gust patterns honestly before answering anything.

The central question stands ahead of 8:30. Which adjudicates first, the $100 billion book or the 8:30 PCE print?

Walk the dots before guessing.

Wednesday’s cash session was a quiet disinflation-impulse day. Oil cracked $70 for the first time since the Iran war began, the 10-year fell ten basis points, and equities went home essentially flat. That move had a name attached to it: Hormuz traffic and the 60-day Iran oil licence feeding through, very slowly. The 2-year, however, refused to budge. The front end is not interpreting this energy story as a path-change for the Fed. It is reading it as a one-off price level. That distinction matters more this morning than it usually would.

Then Wednesday night Micron printed numbers that look like a different industry. Revenue $41.46 billion versus $35.84B estimated. A record 84.9% gross margin against a 74.9% prior quarter. Sixteen strategic customer agreements totalling about $100 billion in contracted revenue, with deposits, take-or-pay clauses, and floor prices. The 2026 HBM book was sold out before the call started. That last detail is the one the textbook will struggle with this morning.

What the textbook says should happen. A disinflation impulse (oil down, 10-year down) plus an idiosyncratic positive earnings catalyst in the highest-multiple part of the equity market should produce a clean risk-on: index futures higher, breadth wide, dollar softer, volatility lower, gold flat. The textbook expects PCE-day caution to be modest because the disinflation impulse is already in place.

What the tape actually did. NQ +2.21%, ES +0.75%, RTY +0.24%. The breadth refused to show up. The dollar is firm at 101.58. Gold is flat at $4,015. VIX is off but still 18. That is not a risk-on tape. That is a single-stock catalyst with read-across to its sector and nothing more, with the rest of the room arms-crossed waiting for a 4.1% headline inflation print.

Sit with the gap. The room can hold a $100 billion sold-out book and a 4.1% headline inflation print simultaneously without contradicting itself, because they live in different parts of the equation. One is a numerator story (memory’s earnings power compounding faster than anyone modelled). The other is a denominator story (the discount rate that turns those earnings into a multiple). The textbook only breaks if both move at once. Usually only one moves a session.

What I cannot decide yet is which the 8:30 print activates. A soft core PCE softens the 2-year, broadens the rally into the breadth that the morning is missing, and the contract terms earn their multiple back. A hot core PCE leaves the rally narrow, the AI complex priced at a discount to its own backlog, and the second-leg equity repricing we have been tracking gets back on track.

Phil’s Musing

The piece of this I cannot stop turning over is the customer-contract terms. Floor prices and take-or-pay on a hundred billion of memory is not the language of a peak. That is the language of a supplier who knows its buyers cannot find the goods elsewhere this cycle. If the read is correct, the multiple compression we got the last three days was a discount-rate trade dressed as a fundamentals trade, and a soft enough PCE today unwinds it quickly. If the read is wrong and PCE prints hot, the AI book trades cheaper than its own forward earnings for a while, which historically has not been a place that pays the bear. I lean cautiously toward the receipts, and let the print mark me to market by tonight.

The follow-through to watch is breadth. If the Russell closes positive on a soft PCE, the second-leg confirmation we have been tracking goes back to a coin toss. If RTY closes negative on a hot print while NQ holds, the de-risk story is fully alive again and the receipts argument runs into a discount-rate wall. Either way we will know more by tonight than we did this morning.

Happy trading,

Phil

Less Brain, More Gain

…and may your trades be smoother than a cashmere codpiece

P.S. – Phils Footnote

This is the kind of morning where the textbook is more honest than the analysts. I have spent the week listening to capex-doubt arguments that sounded sophisticated until the company that sells the actual capex disclosed it had already sold the year under fixed-price floors. I am not certain about PCE. I am more certain about the receipts.

🗒️ Desk Notes | Thursday, June 25, 2026

Observations not trades.

1. Mechanism Read

SESSION BRIDGE: prior session (Wed Jun 24) full reaction SPX -0.10% to 7,358.22 / Nasdaq Comp -0.43% / Dow +0.35% / WTI -3.92% to $70.34 (first sub-$70 of the cycle) / 10Y -10bp to ~4.40% on the oil-led disinflation impulse; AFTER-HOURS catalyst Micron +13% on $41.46B revenue, record 84.9% gross margin, sixteen strategic customer agreements totalling ~$100B contracted; live premarket (04:30 ET Thu Jun 25) ES +0.75% / NQ +2.21% / RTY +0.24% / VIX -3.33% to 18.00 / CL -1.36% / GC +0.16% / DXY +0.19% / BTC +1.08% (recovered from sub-$60k overnight low); threshold: HARD (NQ premarket +2.21% well outside the ~0.6% abnormal band; concentrated AI-memory catalyst, not breadth; the editorial carry-over fires).

What moved (four instruments).

- 2-year UST: ~4.18% area (live source variable; June 22 hit 4.232%, the highest since Feb 2025; Jun 18 cited 4.179%). Did NOT soften ahead of the PCE print. The front end is anchored to the hawkish path.

- 10-year UST: ~4.40%, down ~10bp Wednesday on the oil crash. The long end took the disinflation impulse. The 2s10s gap held wider than recent average; curve still arguing about which end is right.

- DXY: 101.58, +0.19%. Firm, near 2026 high. Risk-off cushion intact even on an AI rip.

- VIX: 18.00, -3.33%. Hedge supply came off as the AI bid returned. Off Monday’s 20+ spike, but well above the May floor.

What it implies (causal read).

- The Wed cash session was a quiet disinflation-impulse day driven by oil. The Wed AH session was an idiosyncratic AI catalyst (Micron). The Thu premarket is the sum: AI lifts NQ +2.21%, but RTY only +0.24% and YM only +0.10% mean the bid is NOT being interpreted as a broader risk-on. It is a single-stock catalyst with wide read-across to AI peers, nothing more so far.

- 10Y dropping 10bp WHILE NQ rips +2.21% is a textbook AI-disinflation bull mix on paper, but the 2yr did not co-operate (held high). That is the signature of a market that wants to believe the rates path softens but the front end will not let it.

- Bitcoin trading as high-beta risk overnight (cracked $60k with stocks, recovered with NQ) rather than as an inflation hedge confirms: this is a rates story doing the work under the surface, not a risk-appetite reset.

The one artery driving the tape today: Micron’s $100 billion contracted backlog and record 84.9% margin. The spine for the AVE/Macro edition. The mechanism is binding multi-year demand at fixed-price floors removing capex doubt as the active driver. PCE at 8:30 ET is the adjudicator that decides whether the multiple holds the new floor.

2. Forward Catalyst Slate

| When | Catalyst | Why it matters |

|---|---|---|

| Thu Jun 25 08:30 ET | Core PCE (May) | Headline expected 4.1% YoY (from 3.8%), core 3.4% (from 3.3%). The print that decides September hike pricing. Soft = relief; hot = front-end vindicated. |

| Thu Jun 25 08:30 ET | Initial Jobless Claims (w/e Jun 20) | Secondary read; only matters if it diverges sharply from trend. |

| Thu Jun 25 08:30 ET | Final Q1 GDP, Durable Goods (prelim May), Personal Income | Bundle prints; durable goods has the cyclical tell embedded; GDP is mostly noise this far in. |

| Fri Jun 26 | UMich consumer sentiment final + inflation expectations | Inflation expectations are the second-tier follow-through to PCE; Warsh framed price stability twelve times on Jun 17. |

| Next week | September FOMC pricing path | Currently ~68% hike odds on CME FedWatch; PCE today + jobs next week + August CPI are the gating prints. |

| Carrying | Saylor / Strategy 8-K monitor | Cash position $1.4B; STRC preferred below par. Watch for either a second sale OR a new aggressive buy. Sale count holds at one. |

3. Divergence Flags

- NQ +2.21% vs RTY +0.24%: the breadth gap is the loudest tell. A real risk-on prints with small-caps participating. This is concentrated AI, not regime change. If the gap closes on a soft PCE, the rally broadens; if PCE prints hot and NQ holds while RTY fades, today’s bid is an air pocket.

- 10Y -10bp Wednesday vs 2Y holding ~4.18%: the front end refused to follow the long end down on oil. That divergence says the rates market is reading the move as a one-off energy disinflation, not a path change. The PCE print is the test of whether the front softens at all.

- Stocks ripping AH on Micron vs Bitcoin cracking $60k overnight: BTC behaved as risk, not as macro hedge, while equities took an idiosyncratic catalyst. The two assets do not share a risk premium today. ETF flows say so explicitly: $584M out over five sessions.

- WTI -3.92% Wednesday vs the Senate war powers 50-48 vote: the political ceiling on more action arrived AFTER oil had already priced peace. Defence stocks have to read both. Watch the relative trade defence-vs-energy this week; a coil there could be the actionable setup.

- MSTR ticked up Wednesday while BTC broke down: the proxy-premium pattern intact through this week; closer to the limit if STRC preferred slips further below par.

- Goldman’s $400 Micron PT and “margins are a peak” falsified inside one print (margins added ten points to a record 84.9%). Note for callbacks: when a sell-side house anchors a thesis on margin compression in a sold-out cycle, the take usually does not survive contact with the customer contract terms.

4. Carry-Over Note

Threshold HARD this edition: the prior session full reaction’s after-hours leg (Micron +13% AH; NQ +2.21% premarket) is well outside the abnormal band, and the catalyst is named and certain. The carry-over rides the tiers as follows:

- AVE: the deflating verdict on three days of fading chips (“Margins that were supposed to be a peak rose ten points”). Once, in the cold-open.

- Snippet: the one-liner on the analyst memo timeline (the capex doubt thesis lasted three days). Once, in the HotTake.

- Macro Edge: the full “they thought X but it was really Y because” dissection: capex doubt was the narrative, the receipts were locked-in floor prices and a sold-out year, and that is what the multiple should have been pricing all along.

5. Part C – Regime Tracking

⚓ Weathervane (the persistent banner). UNCHANGED. Current read: “The Fed has turned hawkish for the cycle. The committee’s own dots flipped from a cut to a hike under Warsh, and higher-for-longer is now confirmed by the instrument, not just the front end. The unconfirmed second leg is risk appetite: equities are still trading as if the turn isn’t real.”

- Today’s note: the second leg’s confirmation got knocked off course in one earnings print. Tue-Wed’s broad de-risk had begun the equity repricing; the Micron blow-out pulled NQ back up violently, but ES +0.75% / RTY +0.24% mean the repricing is only partially unwound. The Weathervane second-leg confirmation is now a coin toss into PCE rather than a leading thesis. The banner does not rewrite, but the read is weaker than 24 hours ago.

- Rewrite rule: not satisfied. We need a confirmed PCE print plus a session that does not round-trip the de-risk before any update. Today is a marker, not a turn.

⚓ REGIME FLAG (internal tripwire). CONFIRMED, holding. Hawkish-for-the-cycle remains the multi-week pattern break. Still a candidate for a longer-horizon special report. Sensitivity read (§17.3), CALIBRATION UNCHANGED, slightly hot as designed. Last week’s restraint on weekend oil re-flare proved correct (reversed in three days). Today’s read: holding fast-tape AI catalyst below flag threshold (a single earnings print is not a pattern break) is the tripwire working as designed. No change requested; Phil agrees or instructs tighten/loosen.

Public tell status: NOT triggered. “Hoist the mainsail, the macro winds have changed” stays holstered. If post-PCE equities round-trip the de-risk fully and breadth returns (RTY catches up), the second leg’s confirmation is back on the table; that is the kind of follow-through that would put the public tell genuinely into play, Phil’s call.