Dow at a high, chips at home, conviction missing.

Ahoy there, Trader! ⚓️

Ahoy there, Trader! ⚓️

It’s Phil…

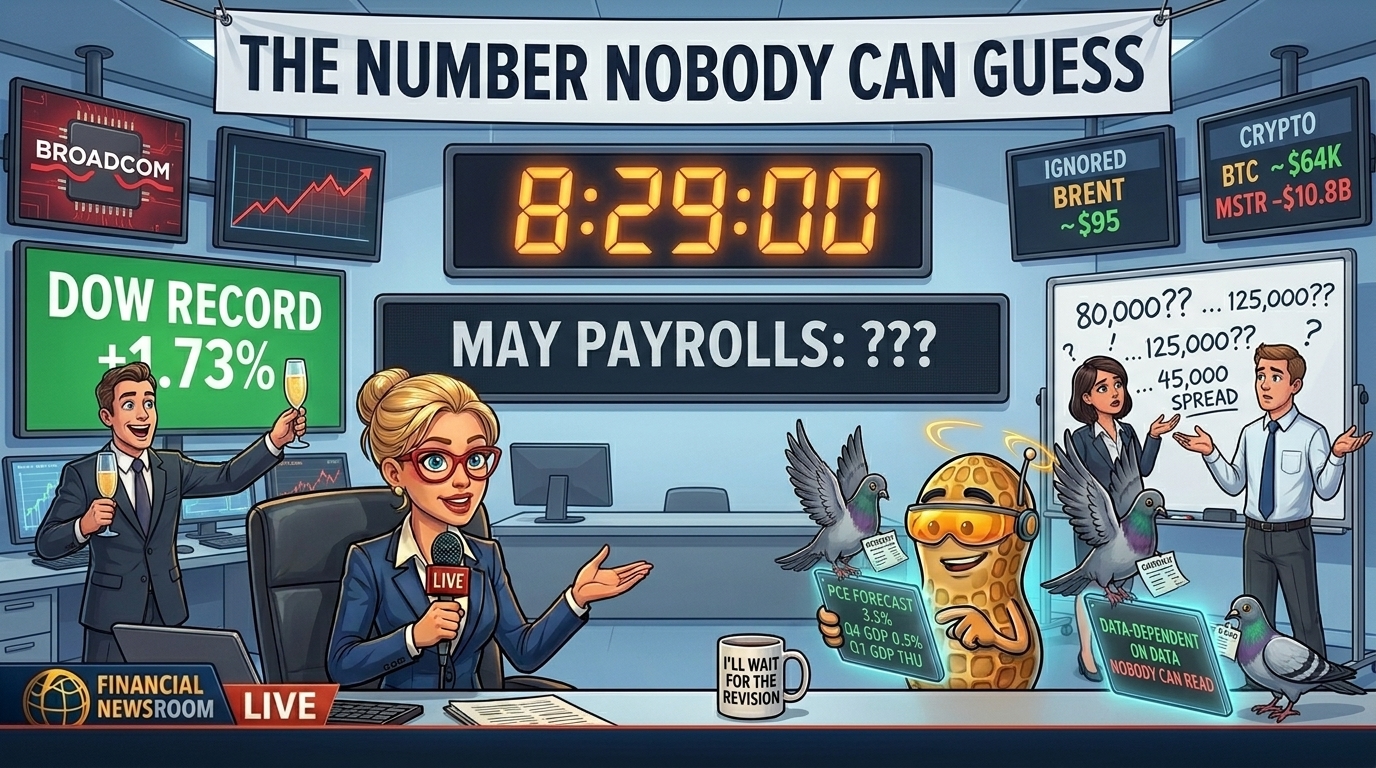

Wall Street Awaits a Number It Cannot Guess Forecasts span 80,000 to 125,000. The new Fed chair’s pitch is fewer answers.

Markets spent Thursday building a record and Friday morning bracing for a number nobody can name. The May payrolls print lands at 8:30 ET. Dow Jones economists guessed 80,000. FactSet guessed 125,000. The gap between them is 45,000 jobs, less a forecast than a shrug with a decimal point.

The supporting evidence arrived pre-confused. ADP counted 122,000 private jobs on Wednesday, a beat. Challenger counted 97,006 announced layoffs in May, the worst May since 2020, with AI blamed for the third month running. The labour market is hiring and firing at once, and Wall Street has decided both are bullish.

All of this feeds the last reading before Kevin Warsh chairs his first FOMC later this month. His stated philosophy is to communicate less. So the market is staking everything on a number it cannot predict, to anticipate a man who has promised to stop explaining himself.

Thursday’s record made it worse. The Dow rose 1.73% on healthcare and financials whilst the chips that built the year stayed home. A rally led by the stocks you buy when you are nervous. At 8:30 the guessing stops and the rationalising starts.

Get The Complete Premium Popper System – Automation Included

Your entry ticket to consistent SPX income. Inside: the exact setup, rules, and checklists I trade daily – for less than the cost of lunch. Easily actionable.

Get The Premium Popper System – Click Here

Stock Market Edge

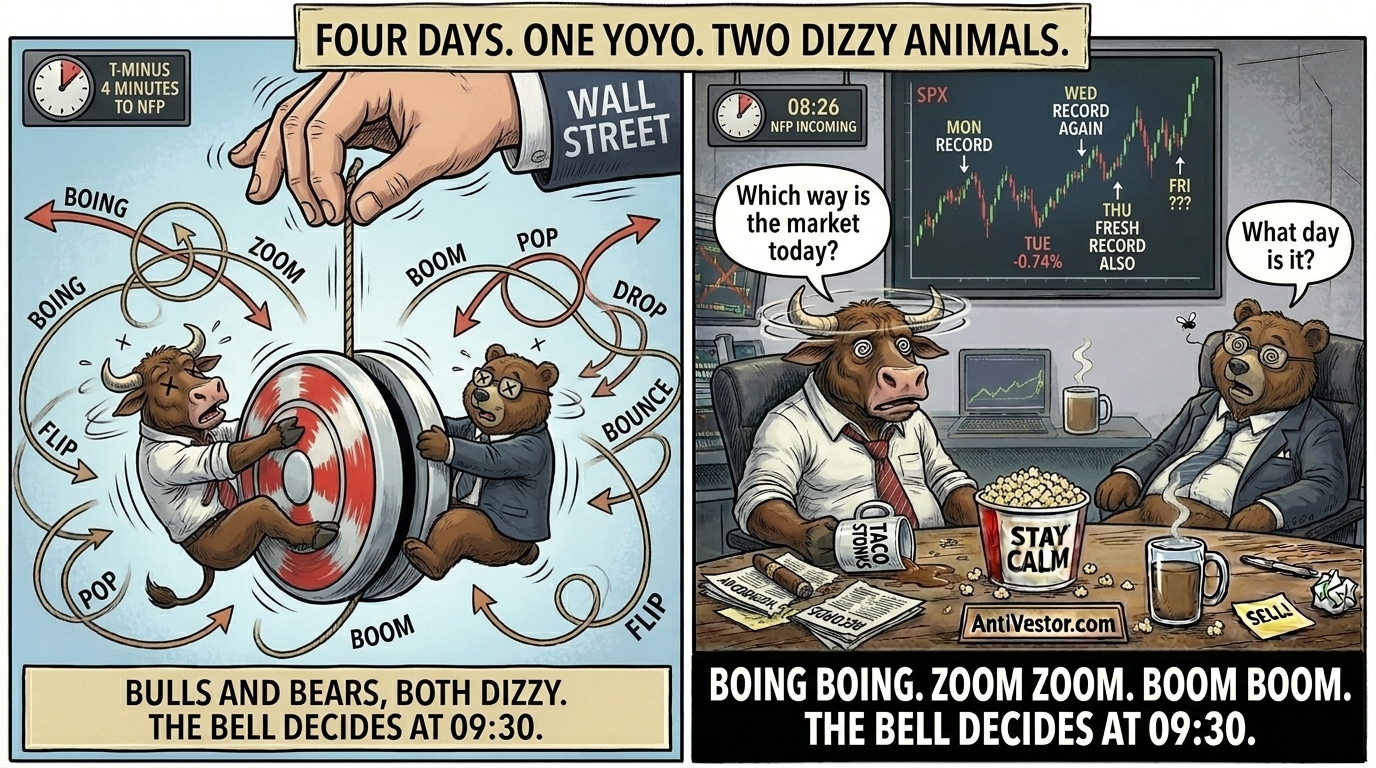

A Record Nobody Quite Believes The Dow hit a high, the engine stalled, and everyone clapped anyway.

- Premarket snapshot: Index futures eased into the 8:30 ET payrolls print, the S&P clinging above 7,600 after Thursday’s close. The Dow finished at a fresh record, up 1.73%. The Nasdaq slipped 0.09%, attending its own party reluctantly after a soft Broadcom note.

- Sector rotation: Healthcare and financials did the heavy lifting whilst technology took the day off. The megacap chips that wrote the 2026 story were absent for the record. Marvell was the exception, soaring after Nvidia’s chief executive anointed it the next trillion-dollar company. Everyone else bought defensives and called it strength, with Dell firming on a fresh Bernstein target lift.

- Earnings or guidance: Broadcom’s soft outlook dragged the chip complex again, the newest AI name to report perfectly well and get sold anyway. Washington chose the same morning to demand export licenses for Nvidia and AMD chips headed to Chinese subsidiaries. Lululemon went further, down more than 11% after trimming its full-year forecasts. Apparently the stretchy trousers stretched the guidance too.

- Cross-asset nuance: Brent held near $95, up over 4% on the week, as a fragile ceasefire did its fragile thing. Iran reported no progress. Trump promised a deal this weekend. Treasury yields stayed above 4.0%, quietly reminding everyone the cuts are still imaginary.

📊 There’s a level on SPX I’m watching closely this morning. My full analysis briefing has it – plus what happens if we hold it, and what happens if we don’t. [Read it here →]

Crypto Market Edge

The Man Who Said Never Just Did Strategy sold, ETFs bled, and the rotation got a rebrand.

- Price snapshot: Bitcoin traded near $64,000, having dipped to $65,710 on June 3, its first look below $67,000 since April. It is down about 13% on the week and roughly 49% from its October high. Ether sat near $2,000, saying nothing, itself halved from its autumn peak.

- Flows & positioning: Spot Bitcoin ETFs shed around $3.4 billion across eleven straight sessions, the worst run of 2026. Citi reckons ETF flows now explain about 45% of weekly moves, a polite way of saying the building has one exit. June 3 added $1.8 billion in liquidations, mostly longs, who had assumed the only direction was up. Europe joined the exit, shedding about $1.67 billion in crypto products the prior week.

- Leadership & rotation: Strategy is now about $10.8 billion underwater on 843,706 coins. The stock hovers near $136, a short walk from its 52-week floor near $104 and down roughly 15% from Friday’s close. Saylor explained the slide as capital rotating into AI, which is one word for it.

- Catalysts & roadmap: Strategy sold 32 Bitcoin at $77,135 to cover preferred dividends, its first sale since 2022. Citi called it a planned tax move, and Tom Lee called it bottom behaviour. The never-sell doctrine, it turns out, had an asterisk all along.

TL;DR – The Bottom Line

- The Dow set a record on healthcare and financials whilst the chips that built 2026 stayed home. A rally led by the stocks you hide in is still a tell.

- S&P futures slipped above 7,600 into the payrolls print. One number nobody could forecast now decides whether Thursday’s record was earned or merely rented.

- Bitcoin fell near $64,000 as ETFs lost $3.4 billion over eleven sessions and Strategy sold coins for the first time since 2022. Never-sell, briefly.

- Economists pinned May jobs anywhere from 80,000 to 125,000, unemployment near 4.3%. A 45,000 spread is not a forecast, it is a group shrug with footnotes.

- The print lands at 8:30, the last labour read before Warsh’s first FOMC this month. A Fed promising to say less greets a market desperate for more.

📌 Fun Fact

The Non-Farm Payrolls report – published by the US Bureau of Labor Statistics on the first Friday of each month at 08:30 ET – is one of the most market-moving economic data releases in the world. Its underlying survey, the Current Employment Statistics (CES) programme, was established in 1915 as a small employer-payroll collection. The current NFP report in roughly its modern form dates to 1939.

NFP measures the net change in non-farm employment across all major sectors, drawn from a sample of approximately 120,000 businesses and government agencies. The print is paired with the household-survey-based unemployment rate that releases at the same minute, and with the average hourly earnings figure that releases alongside.

The forecaster-versus-print dynamic is itself a market discipline: the market reaction is graded against the consensus, not the absolute number, which is why today’s forty-five thousand-job spread between Dow Jones economists (80,000) and FactSet (125,000) is unusual. A 45,000-job gap means that even if NFP prints “in line” with one estimate, it will simultaneously be a beat or miss against the other – a quirk that turns interpretation into a coin flip before the data crosses the wire.

The 08:30 ET first-Friday release window corresponds to the standard BLS economic data release schedule, which is tied to the prior month’s data collection cycle completing in the third week. The data is embargoed until release, with strict media handling protocols dating to the 1980s.

[Sources: US Bureau of Labor Statistics historical archives;

CES programme methodology documentation;

BLS Handbook of Methods (chapter on Employment); public]

Meme of the Day:

Happy trading,

Phil

Less Brain, More Gain

…and may your trades be smoother than a cashmere codpiece

p.s. There are 3 ways I can help you…

- Option 1: The SPX Income System Book (Just $12)

A complete guide to the system.

Written to be clear, concise, and immediately actionable.

>> Get the Book Here

- Option 2: Full Course + Software Access – 50% off for Regular Readers – Save $998.50

Includes the video walkthroughs, tools for TradeStation & TradingView, and everything I use daily. Plus 7 additional strategies

>> Get DIY Training & Software

- Option 3: Join the Fast Forward Mentorship – 50% off for Regular Readers – Save $3,000

>> Join the Fast Forward Mentorship – trade live, twice a week, with me and the crew. PLUS Monthly on-demand 1-2-1’s

No fluff. Just profits, pulse bars, and patterns that actually work.