Oil fell, stocks threw a party, and the one yield that sets the Fed’s path refused to relax. Walking the gap before Warsh speaks Wednesday.

⚓ Weathervane: From easing-bias to inflation-vigilance. The Fed’s compass has been swinging hawkish for weeks while the war premium drains out of oil. Cruise-ship heading, not yet a confirmed turn.

Ahoy there, Trader! ⚓️

Ahoy there, Trader! ⚓️

It’s Phil…

Let’s sit with something that doesn’t quite add up.

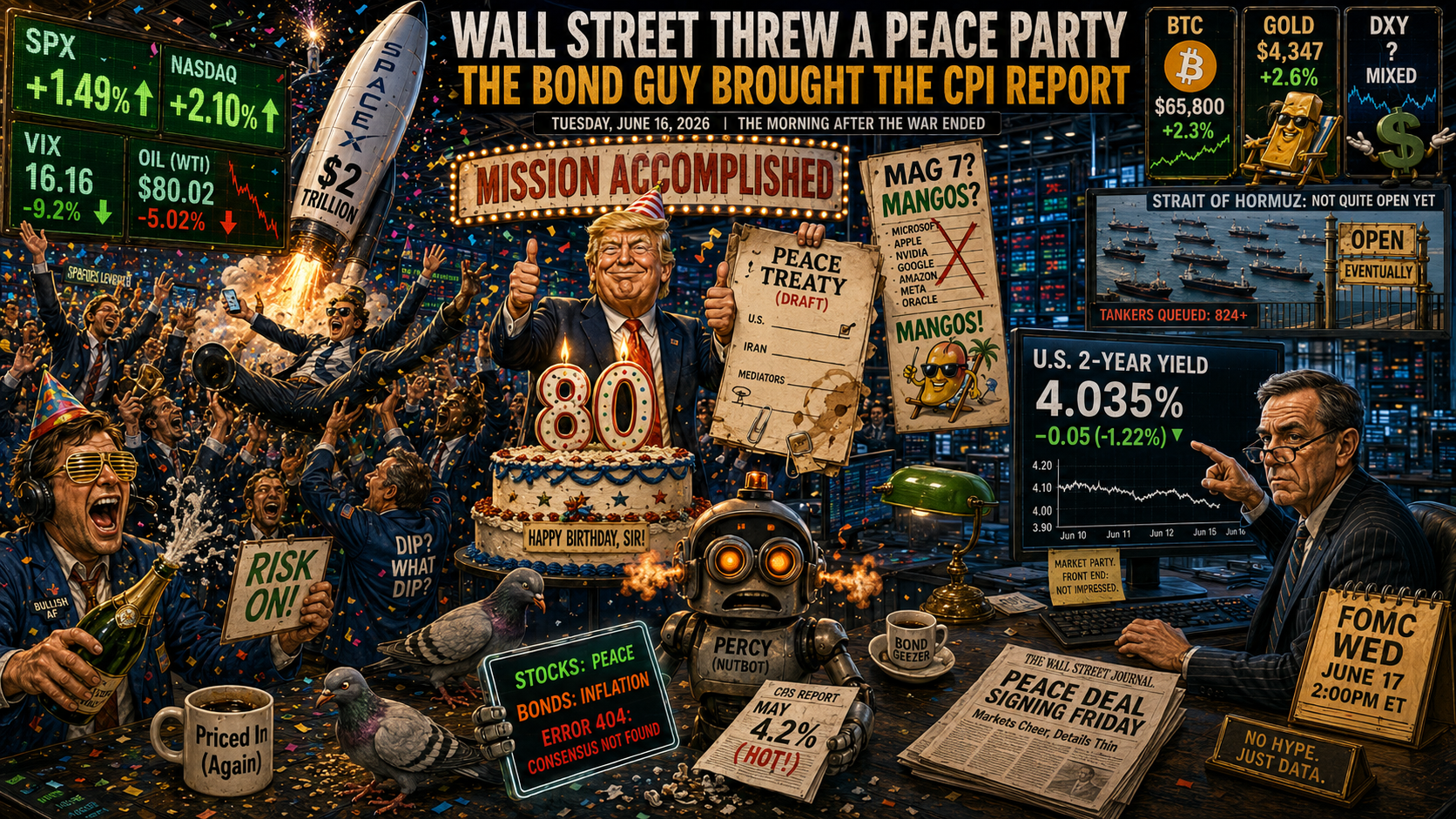

Monday handed us a clean, happy story. The US and Iran agreed to stop fighting and reopen the Strait of Hormuz, oil fell about 5% to near $80, the war premium that had haunted prices for more than 100 days started draining away, and stocks threw a party: the S&P up 1.49%, a record Dow, a newly public SpaceX worth more than $2 trillion. Volatility collapsed toward 16.

Textbook risk-on.

And yet…

The 2-year Treasury yield, which is really just the bond market’s bet on what the Fed does next, sat above 4%. That is above the Fed’s own policy rate of 3.50% to 3.75%. Markets are still pricing roughly an 80% chance of a rate hike before year-end. So here is the question I can’t shake: if peace just pulled the biggest inflationary scare of the year out of the oil price, why didn’t the front end relax with everyone else?

Here is what the textbook says should happen. A geopolitical shock spikes oil and is inflationary; remove the shock, oil falls, inflation expectations ease, and the pressure on the central bank to tighten comes off. Lower oil, lower yields, everyone exhales. That is the clean version, and it is the one the stock market clearly believes.

Now here is what the tape actually did. Oil fell, yes. But the 2-year barely flinched and the hike odds barely moved. Why? Because the inflation the Fed is actually losing sleep over in June 2026 may not be the oil at all. May’s CPI ran 4.2%, a three-year high, but strip out energy and the core monthly number was a tame 0.2%. The scary part was not petrol. It was jobs: 172,000 added in May against expectations near 80,000, a labour market hot enough that the front end thinks the next Fed move is up, not down. Peace cools the oil line. It does nothing for the jobs line. And the 2-year only cares about the second one.

So the gap between the stock party and the bond market’s stony face is not really a contradiction. It is a disagreement about which problem matters. Equities priced the problem that got solved. The 2-year priced the one that didn’t.

The slow read is that the regime has been quietly shifting from “cuts are coming” to “higher for longer, maybe higher full stop” for several weeks, and the 2-year crossing above the policy rate is the clearest tell yet. I would want Warsh’s dot plot on Wednesday before calling the cruise ship turned, but the heading looks hawkish. Not hoisting the mainsail yet.

Which is why Wednesday is the whole game. Warsh chairs his first meeting; almost nobody expects a rate change, but the dot plot and his debut tone will tell us whether the committee sides with the 2-year or with the stock market. One of them is about to look early.

Happy trading,

Phil

Less Brain, More Gain

…and may your trades be smoother than a cashmere codpiece

P.S. – Phil’s Footnote

Learning in public: I find this one genuinely clarifying, because it is a reminder that “the market” is never a single opinion. The bond market and the stock market looked at the exact same Monday and reached opposite conclusions, and only one of them gets to be right by Thursday. I will be watching the front end more closely than the headline. Tell me what I am missing.

🗒️ Desk Notes | Tuesday, June 16, 2026

Raw briefing.

1. Mechanism read (full)

- 2yr (front end): above 4.00%, sitting ABOVE the Fed funds range (3.50% to 3.75%). Driven there by May payrolls (172,000 vs ~80,000 expected) and CPI 4.2% y/y (three-year high). Options price ~80% odds of a hike by year-end even after the ceasefire eased it. This is the artery.

- 10yr (long end): ~4.4% area (last firm reference 4.41% in early May; 30yr near 2007 highs). 2s10s still positive, front end catching up. LIVE VARIABLE: a confirmed Mon Jun 15 10yr close was not isolated in the search pass, framed qualitatively.

- DXY (transmission): no fresh print confirmed this pass. Peace plus lower oil plus risk-on is a mixed dollar signal. LIVE VARIABLE.

- VIX (confirmation): crushed toward 16 (premarket -14.6% to ~16.6) on the deal. A rally with vol crushed is a clean relief rally, not a nervous one.

- What it implies: the equity move is a geopolitical-premium unwind (oil down, VIX crushed, risk back on), NOT a Fed pivot. The 2yr is saying the Fed’s actual problem (hot jobs, sticky core) is untouched by peace. Oil down helps headline CPI optics (energy was ~60% of the 4.2% reading; core monthly only 0.2%) but does nothing for the labour-market heat. Stocks priced the problem that got solved; the 2yr priced the one that didn’t.

- One artery: the 2yr above 4%, pricing a hike into Warsh’s first meeting while equities took a peace victory lap.

2. Forward catalyst slate

- Tue Jun 16: FOMC Day 1 begins, Warsh’s first as chair. Decision-eve coiling.

- Wed Jun 17: FOMC decision 2:00pm ET + Summary of Economic Projections + new dot plot + Warsh debut press conference 2:30pm ET. THE event. Rate hold ~97% priced (CME FedWatch 97.4%); the signal is in the projections, the tone, and the dissents (April’s meeting was the most divided in decades).

- Thu Jun 18: post-Fed digestion; deal-signing run-up.

- Fri Jun 19: Juneteenth, US market closed. US-Iran deal scheduled to sign. Note the oddity: the week’s most market-moving signature lands on a no-trade day.

- Watch: dot-plot shift from easing bias to neutral / hike-tail; Warsh’s leaner-Fed, says-less communication style on debut; Trump-Warsh tension (Trump publicly wants cuts, the data says otherwise).

3. Divergence flags

- Breadth vs index: S&P +1.49% but only ~50.7% of the tape advanced vs 46.7% declining. The index move was tech-led, not broad. The rally is narrower than the headline.

- Price vs flows (crypto): BTC two-week high above $65,500 against an 11-day ~$3.4bn spot-ETF outflow streak. Price leading, money leaving.

- Peace rally vs front-end hike pricing: the headline divergence. Equities and the 2yr read the same Monday and disagreed.

- Defence names: rode the war’s structural arms-race bid for weeks (LMT +3.4% Jun 11 on ~$10bn awards, NATO production push). A peace deal directly tests that premium. No confirmed Mon Jun 15 defence move isolated this pass, watch the reaction into the signing.

- Oil down on eased geopolitics, deal unsigned: the deal signs Friday and a reopening may be only partial given infrastructure damage. The peace-priced-early pattern fired again, just with an actual deal attached this time.

4. Regime tracking

- ⚓ Weathervane (banner): “From easing-bias to inflation-vigilance: the Fed’s compass has swung hawkish over recent weeks while the war premium drains out of oil. Cruise-ship heading, not yet a confirmed turn.” Rides into Wednesday unchanged.

- ⚓ REGIME FLAG (soft): the Fed-path easing thesis has broken its multi-week pattern. Rate-expectations have moved from “cuts coming in 2026” at the start of the year to “no cuts, ~80% hike odds, cuts pushed to 2027,” and the 2yr now sits ABOVE the policy rate. That is a genuine multi-week pattern break, not a single odd day. Candidate for a longer-horizon special report on the higher-for-longer turn under Warsh, pending Wednesday’s dot-plot confirmation.

- Sensitivity read (tight-or-loose): running slightly TIGHT / hot, by design (the curious-newbie over-caution we set on purpose). The easing-thesis break is real, but hoisting anything before the SEP prints would be jumping the gun. I would hold this flag soft and let Wednesday confirm or deny. Phil’s call on whether to tighten the trigger.

Observations only. No named trades.