A 20 percent iPad price hike, a 6 percent Apple sell-off, an unchanged 2-year. One day, three readings, no agreement. Time to walk the chart.

⚓ Weathervane: The Fed has turned hawkish for the cycle. Higher-for-longer is confirmed by the instrument; the unconfirmed second leg is risk appetite. Today nudges the second leg through an unfamiliar channel: chipflation, not the rate path.

Ahoy there, Trader! ⚓️

Ahoy there, Trader! ⚓️

It’s Phil…

Let me try to think through this one out loud, because the tape on Thursday did something I have not seen before and I am genuinely trying to work out which mast to lash this to.

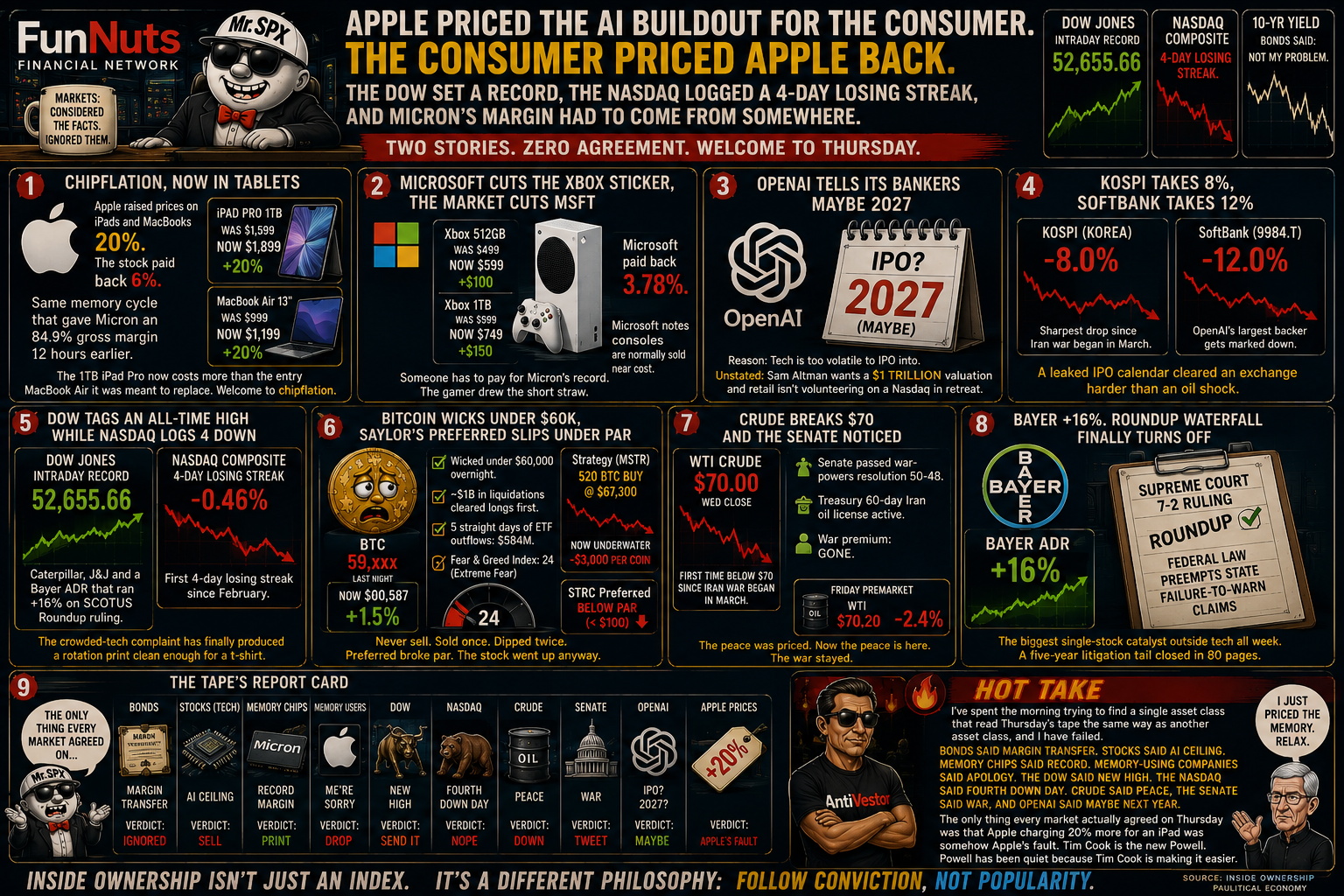

Here is the day, as plainly as I can put it. Wednesday after the close, Micron printed a record. Revenue $41.46B, gross margin 84.9 percent, $100B of contracted memory revenue across 16 customers. Twelve hours later, on Thursday morning, Apple raised iPad and MacBook prices 20 percent. The stock closed -6 percent. Microsoft did the Xbox version, +$100 on the 512GB / +$150 on the 1TB, and the stock closed -3.78 percent. Core PCE printed 3.4 percent year-on-year, the highest reading since October 2023. The Dow set an intraday all-time high at 52,655.66. The Nasdaq logged its first 4-day losing streak since February.

So, the question I want to ask out loud. Does chipflation reach the Fed?

Here is what I cannot work out. The cleanest single sentence the tape gave me Thursday was this: the memory cycle that put Micron at 84.9 percent gross margin is the same cycle that just forced Apple to lift consumer prices 20 percent. That is a complete transmission chain visible to a household: AI capex → memory scarcity → upstream margin → consumer sticker. And it is appearing precisely at a moment when the Fed has told us, plainly, that it will deliver price stability and that the next move is more likely to be a hike than a cut.

The textbook says: when a goods category passes a 20 percent input cost to the consumer in one move, the next CPI/PCE goods print catches some of it, and the front end of the curve repositions. The 2-year sits up. The dollar bids. The market starts pricing the hike with more conviction. That is the relationship. That is what the chart is supposed to do.

Here is what the chart actually did. The 2-year barely moved. The dollar barely moved. Equity leadership was the only instrument that re-rated. Apple -6. Microsoft -3.78. Nvidia and Amazon -2. The bond market, in other words, voted that this is a margin transfer up the chip stack, not new consumer inflation. The equity market voted that the AI trade has found its own ceiling because the customer cannot keep absorbing memory cost without it eating multiples.

Both of these can be true at once, and that is where I get stuck. Margin transfers do not always print in headline inflation, because consumers can substitute, defer purchases, or trade down. The 20 percent Apple sticker may be more elastic than it looks. But the precedent for memory cycles is not friendly: the last full DRAM/NAND scarcity cycle of comparable shape, 2017-2018, did show up in CPI goods at the margin. It was muted because the Fed at the time was already tightening. The Fed at the moment is tightening too.

So my honest read is that the bond market is right for now and wrong eventually. Right for now because one Apple price hike is not a trend, and the goods component of PCE has been the disinflationary leg of the cycle. Wrong eventually because if Q3 brings similar guides from the other Mag7 hardware names, and core goods PCE prints with a chipflation contribution into autumn, the front end has to engage. Whether “engage” means a third hike priced or a fourth is the regime question; that the question gets asked at all is the chipflation thesis crossing the threshold.

Phil’s Musing

My lean is that the bond market is reading this right for the next month or two. Chipflation is a margin story first, a CPI story second, and the consumer absorbs a sticker hike before the print catches it. The trade I am watching is not what the 2-year does on the next PCE; it is what the goods-services spread does over the next two prints. If the spread narrows, chipflation is a multiple story and Macro Edge says so. If the spread widens, we have a problem the Fed has not engaged with yet, and the cruise ship turns.

Happy trading,

Phil

Less Brain, More Gain

…and may your trades be smoother than a cashmere codpiece

P.S. – Phils Footnote I find this one harder than usual to write a verdict on. The Fed under Warsh told us last week it would deliver price stability; Apple told us on Thursday what that might actually cost in iPad units. The bond market shrugged, equity leadership did not, and I have spent the morning trying to work out which side is going to look right in six weeks. I lean to the bond market for now and the equity tape for the cycle, and I will mark this honestly either way. Ahoy.

🛠 Desk Notes | Friday, June 26, 2026

Raw morning briefing. Observations, not trades.

1. Live tape state

SESSION BRIDGE: prior session (Thu Jun 25) full reaction Dow +0.14% to ATH 52,655.66 intraday / 51,920.62 close, S&P -0.01% to 7,357.49, Nasdaq -0.46% to 25,358.60 logging first 4-day losing streak since February, Apple -6% on a 20% iPad/MacBook price hike, Microsoft -3.78% on Xbox $100/$150 hikes, Micron +15% on its earnings, Bayer ADR +16% on SCOTUS Roundup ruling; core PCE 3.4% YoY (in line, highest since Oct 2023), monthly headline 0.4% (cooler than 0.5% consensus), Q1 GDP final 2.1% (revised up from 1.6%), personal income +0.7%, personal spending +0.7%; after-hours NYT report OpenAI is leaning to a 2027 IPO drove KOSPI -8% / SoftBank -12% in Asia Friday; live premarket Fri Jun 26 03:30 ET / 08:30 UK ES -0.14% / NQ -0.56% / RTY +0.16% / YM +0.19%, VIX +3.44% to 19.53, CL -2.39% to 70.20, BTC +1.48% to 60,587 (off a Thursday close near 59,700 after a sub-60k overnight wick), DXY -0.14% to 101.44, gold +0.14% to 4,053.3; threshold: SOFT (index futures silent under 1%, but Thursday’s intra-cash rotation, Dow ATH vs Nasdaq 4-day losing streak first since February, and the OpenAI 2027 IPO tail are the noteworthy catalyst that fires the carry-over; the OpenAI delay is the late catalyst the bridge weights past the cash close).

Live variables for Phil to verify before publish:

- 2-year yield exact level (last cited ~4.18% area in ledger; the post-PCE settle is the variable).

- BTC retest level into the US open (currently 60,587, ranged between 59,700 close and the wick).

- Hormuz: a fresh cargo-vessel incident was reported Thursday; verify whether the tape is still treating it as priced.

2. The mechanism read

What moved:

- Front end (2yr): essentially flat through PCE; the bond market did not engage on a sticky core or on the Apple/MSFT price-hike news. The September hike odds firmed slightly on CME FedWatch but the rate path is not in motion today.

- Long end (10yr): ~4.40% area after the ~10 bp Wednesday fall, stayed there Thursday. Curve sits in its post-FOMC flat regime; no fresh signal.

- Dollar (DXY): 101.44, -0.14% premarket Friday. Despite a sticky PCE and a stronger Q1 GDP revision, the dollar did not bid. That’s the cleanest read that the bond market is treating Thursday’s news as a margin transfer story, not a new-inflation story.

- Vol (VIX): 19.53, +3.44% premarket. Small absolute move but the premarket bid confirms the tape is in a rotation, not a panic. No one is buying tails on this; they are selling AI leadership and buying everything else.

What it implies (causal read): The chipflation transmission is now a one-step pipeline visible to a retail consumer: Micron’s record 84.9% gross margin Wednesday after the close → Apple raises iPad/MacBook prices 20% Thursday → Apple -6% → Microsoft does the Xbox version → MSFT -3.78%. The leadership de-rate that began Tuesday is now mechanically explained, not just a “froth” narrative. Crucially, the rates side did not confirm it as new inflation; the equity side did confirm it as a ceiling on the AI leadership multiple.

The OpenAI delay tail is the same story told upstream. If the most-anticipated IPO of the cycle is being delayed because the market is too volatile to receive a $1T price tag, then the AI capex story has lost its public-market validation. SoftBank -12% is the cleanest read of what that means for OpenAI’s largest backer.

The one artery driving the tape: Apple’s 20% price hike, because it is the consumer-facing receipt of the entire AI capex cycle and the first one the bond market did not engage with. The Dow at ATH on Caterpillar and Bayer is the funding flow, not the cause.

3. Forward catalyst slate

Today (Fri Jun 26):

- 10:00 ET: University of Michigan final June consumer sentiment. The only US data print. Watch the 1yr inflation expectation, if it ticks up alongside Thursday’s PCE, that’s the first soft signal that chipflation is leaking into household perception.

- BTC ETF flow data for Thu Jun 25 lands later; the fifth-straight outflow run becomes a sixth or breaks.

Weekend / early next week:

- Strategy 8-K window stays live. Sub-par STRC into Monday is the funding-strain signal; another buy disclosure with the position underwater is the next test of the never-sell line.

- BTC weekly close into Sun: 60k area is the cycle floor question.

Next week (data slate):

- Mon Jun 29: no major data or earnings.

- Tue Jun 30: June consumer confidence, Nike (NKE) and Constellation Brands (STZ) earnings.

- Wed Jul 1: ADP June employment, June construction spending, June ISM Manufacturing PMI, General Mills (GIS) earnings.

- Thu Jul 2 (early close ahead of Jul 4 holiday): jobless claims; possible market closure portions.

- Fri Jul 3: market closed for Independence Day.

The ADP/ISM combo Wednesday is the first hard print of next week. If ISM softens and ADP holds, that’s the dovish set-up the disinflation-pivot needs; if ISM bounces, the higher-for-longer thesis gets a third leg of confirmation.

4. Divergence flags

- Dow ATH vs Nasdaq 4-day losing streak. The cleanest rotation print of the cycle. Mag7 funded defensives/industrials; equal-weight held while cap-weight wobbled. The breadth read against tech crowdedness has actually arrived as numbers. Watch whether the rotation broadens to the Russell into next week or stalls on the first ISM print.

- 2-year unchanged through a sticky core PCE AND a 20% Apple price hike. That is two disinflationary tells the bond market did not buy. Either the bond market is right that this is margin transfer (in which case the equity de-rate finds a floor once positioning clears), or the bond market is wrong and Q3 PCE prints with a chipflation contribution the Fed will have to engage. Phil’s “cheaper oil will not move Warsh’s Fed” Part B shot leans into the first reading.

- Crude down 2.4% in premarket while a fresh Hormuz incident is in the tape. The premium is fully gone and the political/operational risk no longer prices into oil. Either Iran becomes a non-event for the cycle, or there is a sleeper repricing coming if a new vessel incident scales.

- BTC bounced 1.5% off a sub-60k wick without ETF inflow confirmation. Spot reclaimed; flows did not. The cleanest read of the “trapdoor opened, longs flushed” story; the floor test is whether next week’s flows turn.

- STRC below par with Strategy’s latest buy underwater. The first quantifiable funding strain in MSTR’s capital stack. The 8-K window into next week is the live falsifier on both Saylor’s never-sell and on MSTR’s accumulation capacity.

5. Carry-over note

Fires today: SOFT. The index thresholds did not trip on numbers alone (premarket silent under 1%), but the Thursday intra-cash rotation (Dow ATH vs Nasdaq 4-day losing streak first since February) plus the OpenAI 2027 IPO after-hours tail are the noteworthy catalyst pair worth carrying.

The noteworthy thing: The market that has been waiting for inflation from Powell got it from Tim Cook instead, and the bond market did not engage. The leadership was repriced inside one Thursday on a transmission mechanism (Micron margin → Apple sticker → MSFT Xbox sticker) clean enough that no one on the desk could pretend it was a vibe call.

How it rides the tiers (today):

- AVE: built around the spine. “Tim Cook just did Powell’s job for him” runs the teaser logic.

- Snippet: the 🏭 / 📺 / 🤖 sequence carries the chipflation pipeline as three sequential gags.

- Macro Edge: the actual dissection, what chipflation is, what it isn’t, why the bond market voted “not yet”, and what would force a vote the other way.

6. Part C, Regime block

⚓ Weathervane (the persistent banner)

UNCHANGED but visibly tested. The current read: “The Fed has turned hawkish for the cycle. The committee’s own dots flipped from a cut to a hike under Warsh, and higher-for-longer is now confirmed by the instrument. The unconfirmed second leg is risk appetite: equities are still trading as if the turn isn’t real.”

Today’s note: Thursday delivered the cleanest second-leg confirmation yet, but on an unfamiliar mechanism. The leadership was not re-rated on the rate path; it was re-rated on margin transfer. The end result for the Weathervane is the same, leadership de-rated, breadth held, but the route is new. The Weathervane therefore holds, second-leg confirmation now reads as in-progress through a chipflation channel rather than a rate channel.

Rewrite rule: not satisfied. The cruise ship has not turned; the speedboat is making a slightly different wake.

⚓ REGIME FLAG (the internal tripwire)

- CONFIRMED, candidate special report still live. The hawkish-for-the-cycle turn remains the confirmed multi-week pattern break. Today’s chipflation read is a refinement of the transmission mechanism, not a new flag.

- Second candidate thread (chipflation as a regime story, not just a fast-tape one): held below threshold. One Apple print does not break a pattern. If the July guides from MSFT, GOOG, META show similar memory pass-through and core PCE prints with a goods-services spread that widens further on chipflation, the candidate fires.

- Sensitivity read (§17.3): unchanged, holding loose-leaning. Holding the chipflation thesis as a Macro Edge central question rather than a fired regime flag is the tripwire working as designed. One earnings cycle is not yet a regime change. Phil to agree or instruct tighten/loosen.

- Public tell status: NOT triggered. “Hoist the mainsail” stays holstered.