A curious-newbie walk around Hormuz cycle seven, from Brent $76 after hours back to $72 by London open.

(…and that’s even changed since I wrote this)

⚓ Weathervane. The Fed has turned hawkish for the cycle. The committee’s own dots flipped from a cut to a hike under chair Warsh, and higher-for-longer is now confirmed by the instrument. The unconfirmed second leg is risk appetite. Equities are still trading as if the turn is not real.

Ahoy there, Trader! ⚓️

Ahoy there, Trader! ⚓️

It’s Phil…

Let me try to think about last night with a clear head.

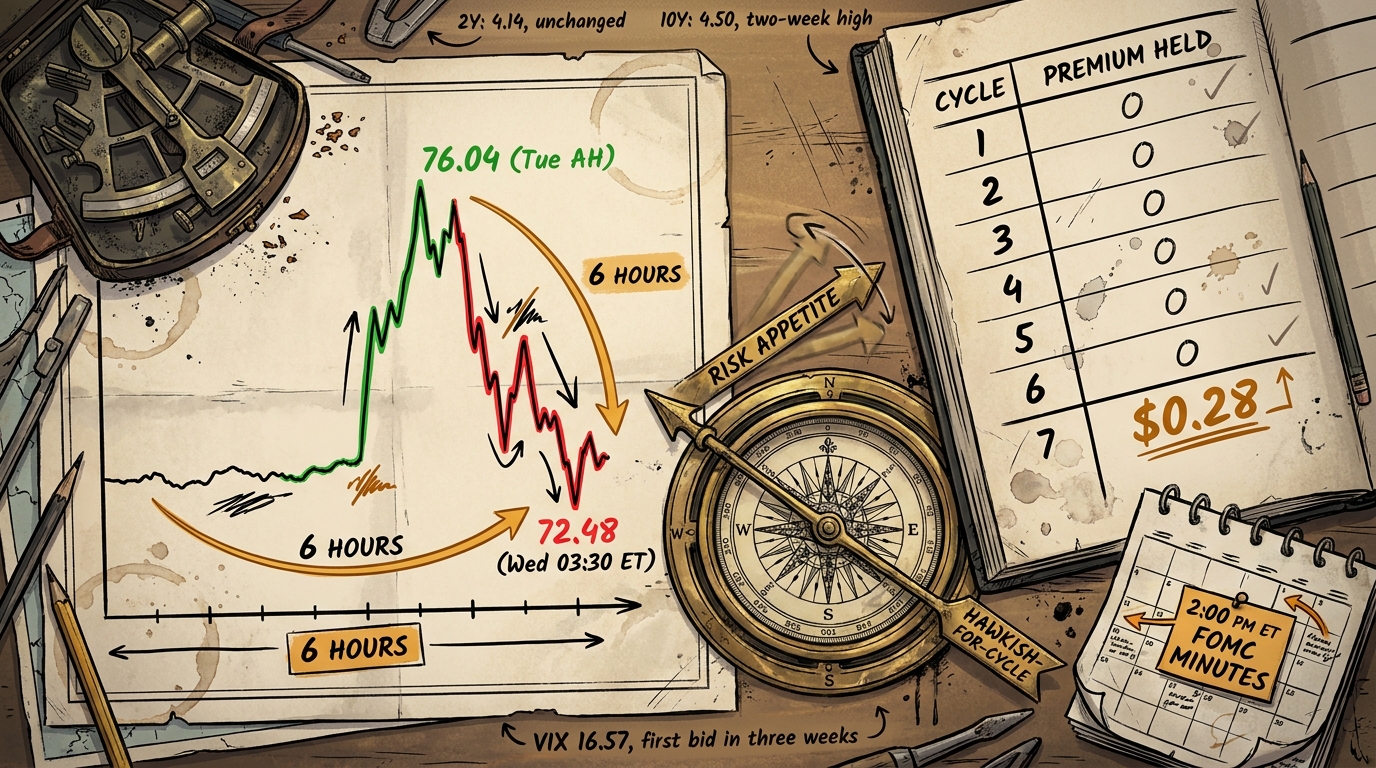

If a war premium round-trips in six hours after actual strikes, has Hormuz been priced out or has the tape stopped listening?

Here is what happened. Tuesday afternoon Iran attacked three tankers in Hormuz. The Treasury revoked Iran’s oil waiver after the bell. Brent spiked 5.6% to $76.04 after hours, WTI 5.4% to $72.25. Overnight, US Central Command struck Iranian targets in reply. By 03:30 ET, WTI sat at $72.48, three cents above Tuesday’s cash close, Brent near $72. Six hours, one war premium, gone. The 2-year did not move.

Sidebar – and this has all changed again in the time i’ve been writing this

The textbook says a kinetic exchange in the world’s largest oil chokepoint should not fully unwind before the next US cash session opens. Hormuz moves 20 million barrels a day; there is no substitution on that scale. None of the textbook survived contact with the tape.

Three candidate readings, and I am not sure which to lean on.

One. Hormuz has been genuinely priced out. Six cycles of escalate-deny-progress taught the tape these events look large and settle small. If cycle seven is the first with actual American strikes and the price still refuses to hold a premium, the de-pricing is structural. The next incident is worth less again, until sustained closure forces a re-price.

Two. The tape has stopped listening for reasons that have nothing to do with Hormuz. Fed minutes at 2pm, Mag7 guides from Jul 22, CPI Jul 14, and a 10-year already at a two-week high on Tuesday’s oil bid. Every desk on the street is watching 2pm. Overnight news arrived on a day the tape’s attention was pointed elsewhere.

Three. The two are the same thing. If a market looks through your event because other events matter more, that is de-pricing whether you call it that or not.

One instrument would resolve this. If Fed minutes read hawkish enough that the 2-year still cannot move, we have the strongest confirmation to date that the front end is anchored, and the Hormuz shrug is real. If minutes reveal doves louder than the dots implied and the 2-year finally moves, displaced attention is doing more work than we thought and cycle eight tests the read again.

I do not have a lot of conviction on which lands. I would rather sit with the question and see what 2pm does.

Phil’s Musing

On my read the six-hour round-trip is more signal than noise. The tape has already booked Hormuz as a cycle it can walk. The 2-year at 4.14% is the tell. My lean into Fed minutes is that Warsh’s committee shows enough hawk language to keep the front end where it is, which would confirm the de-pricing reading. The scenario I would price against: minutes reveal a louder dove wing than the dots imply, 2-year moves five basis points on the print, and both the Fed anchor and the Hormuz shrug get read as one displaced-attention story. That is not what I would bet, but it is the alternative I want to be honest about.

Happy trading,

Phil

Less Brain, More Gain

…and may your trades be smoother than a cashmere codpiece

P.S. – Phils Footnote I keep noticing that I now write the word “cycle” the way I used to write “chapter.” That is either useful shorthand or a warning sign that my brain has flattened seven distinct events into one shape. Something to watch.

🗒️ Desk Notes | Wednesday, July 08, 2026

Internal briefing. Observations, not trades.

Live tape state

SESSION BRIDGE: prior session (Tue Jul 7) full reaction cash SPX -0.45% to 7,503.85, NDX -1.8%, Dow -0.25% to 52,925.15 off intraday ATH, VIX close ~16.14, WTI settled +2.8% at $70.44, Brent +3% at $74.16, driven by Samsung’s Q2 preliminary print (19-fold profit priced as a miss), the Reuters DeepSeek in-house-chip report knocking NVDA -1.6%, and Iranian attacks on three Hormuz tankers. Overnight tail: Treasury revoked Iran’s oil sale waiver Tue AH, Brent popped 5.6% to $76.04 and WTI 5.4% to $72.25 AH, US Central Command struck Iranian targets Wed overnight, and the oil premium round-tripped back near Tuesday’s cash close by 03:30 ET. Live premarket at 03:30 ET: ES -0.25% to 7,532.75, NQ -0.46% to 29,284, YM -0.38% to 52,995, RTY -0.50% to 2,982.8, VIX +2.66% to 16.57, WTI +0.39% to $72.48, gold +0.26% to $4,127.3, BTC -1.09% to $62,632.67, DXY 100.855 flat, 2yr 4.14%, 10yr 4.50%. Threshold: HARD (NDX -1.8% with a clear catalyst per §8.4.1; overnight kinetic escalation with a live premium round-trip; carry-over fires across the ladder).

Mechanism read

What moved. Long end did the pricing yesterday: 10-year 4.50% is a two-week high on Tuesday’s oil bid, not on this morning’s kinetic reply. 2-year 4.14% has not moved since Friday: cheap oil, cooler PCE, a Supreme Court ruling, best Nasdaq quarter in six years, Warsh at Sintra, and now actual US strikes on Iran have failed to move the front end more than three and a half basis points. DXY 100.87 flat for eight consecutive sessions against sterling. VIX bidding for the first time in three weeks, but still sub-17.

What it implies. The long end is pricing oil-driven inflation risk into Warsh’s minutes; the short end is pricing Fed-committed hawkishness that already priced everything the short end thinks matters. That is the term-premium engine at work. The dollar is not confirming the oil bid (DXY flat), which reads consistent with domestic-only rate re-pricing rather than a global risk shift. VIX bid without an equity break is a positioning hedge, not a directional flag.

The one artery. The oil round-trip is the tape’s verdict, and its refusal to move the front end is the mechanism. Kinetic escalation in Hormuz cycle 7 failed to hold a bid in six hours. This is the strongest confirmation to date of the Hormuz-de-priced thesis and the Fed-anchored thesis in the same tape. Fed minutes at 2pm ET is the day’s only remaining catalyst that could argue with either.

Forward catalyst slate

- Wed Jul 8, 2pm ET. FOMC minutes from June 16-17 meeting, first Warsh-era document. Nine dots project a 2026 hike; the chair withheld his own. The minutes are the FOMC’s only substantive on-record read on the September hike question. Watch for hawks’ language explicitly justifying September and doves’ language explicitly building a hold case; Warsh’s forward-guidance abandonment is the frame.

- Wed Jul 8, ongoing. Hormuz cycle 7 live. Any second projectile incident before Thursday close is a hard falsifier for the “de-priced” thesis. Watch WTI $75 and Brent $80 as visible re-price thresholds.

- Thu Jul 9 premarket. PepsiCo Q2 print (~$2.19 EPS consensus). First read on discretionary staples pricing power. Delta Fri premarket opens airline earnings; travel demand tell.

- Mon Jul 14. June CPI print. Core-goods contribution is the chipflation transmission tell (§ledger Part B “Chipflation is a margin transfer first”).

- Jul 15. STRC coupon payment date. First cash out of the announced BTC-monetization program. Track for downstream corporate-BTC treasury signal.

- Jul 17. CLARITY Act hearing in the Senate. Institutional crypto flow catalyst.

- Jul 22 through Jul 31. Mag7 July guides rolling from Tesla (Jul 22) through the majors. Memory input cost as a named margin headwind is the trigger for chipflation regime upgrade.

- Jul 28-29. FOMC meeting. September hike odds now 50 to 58% depending on the source; live catalyst window.

Divergence flags

- Long end vs front end. 10-year moving on the oil bid, 2-year unmoved by kinetic escalation. Term premium is doing the work. Not resolved by Fed minutes unless the language rebuilds forward guidance (unlikely given Warsh’s stated posture).

- Oil vs oil news. Brent tapped $76 AH on the license revoke, US strikes fired, and the round-trip completed in six hours. The market has stopped pricing Hormuz risk as a live catalyst. Watch cycle 7 for a second hard confirmation.

- BTC price vs Strategy sale. BTC bounced $4,600 off the June low, then held near $62,600 into the Jul 6 disclosure of Strategy’s largest-ever sale ($216M at a loss to cost basis). The reference bid held, but the corporate-treasury tell is now on the calendar.

- BTC price vs ETF flows. Two positive flow days (Jul 2 +$221.7M, Jul 3 +$46.6M) versus seven straight weeks of prior outflows. Not a trend, an interruption.

- Chip vendor node vs customer margin. Samsung’s record Q2 booked the margin capture. Nasdaq futures opened red into the print; customer-side transmission adjudicates on Mag7 July guides. This is the chipflation adjudication window opening now.

- KOSPI vs SMH. KOSPI -4.9% Tuesday, SMH -3%. Semi complex remains globally correlated but the domestic re-price is smaller. Watch SK Hynix ADR launch this week.

Regime read (Part C, tight-or-loose sensitivity)

⚓ Weathervane: unchanged, load-bearing on seven legs now that Hormuz cycle 7 has resolved to a six-hour round-trip on kinetic strikes. Current read: “The Fed has turned hawkish for the cycle. The committee’s own dots flipped from a cut to a hike under Warsh, and higher-for-longer is now confirmed by the instrument. The unconfirmed second leg is risk appetite: equities are still trading as if the turn isn’t real.”

Today’s note. Cycle 7 with a US kinetic response and a six-hour Brent round-trip is the strongest single-session confirmation to date of the Hormuz-de-priced candidate thread. Combined with the 2-year sitting at 4.14% through the whole exchange, the instrument tape is compounding. Fed minutes at 2pm is a live gate on both legs simultaneously (short-end confirms hawkish path, or reveals internal fracture; if hawkish confirmed, Weathervane deepens).

Regime Flag: not tripped this session. Hormuz thread is one clean cycle inside the confirmation trigger (upgrade to tracked structural on the next zero-price kinetic incident, or one CPI-through with core goods contribution). Chipflation is at booked-margin confirmation, one Mag7 guide from tracked structural. Sensitivity read: UNCHANGED, holding loose-leaning. Two live candidate threads at the confirmation threshold, both testing on the next scheduled event (Fed minutes 2pm; PepsiCo/Delta earnings Thu/Fri; June CPI Jul 14). Phil to agree or instruct tighten/loosen.

Public tell: NOT triggered. “Hoist the mainsail, the macro winds have changed” stays holstered.