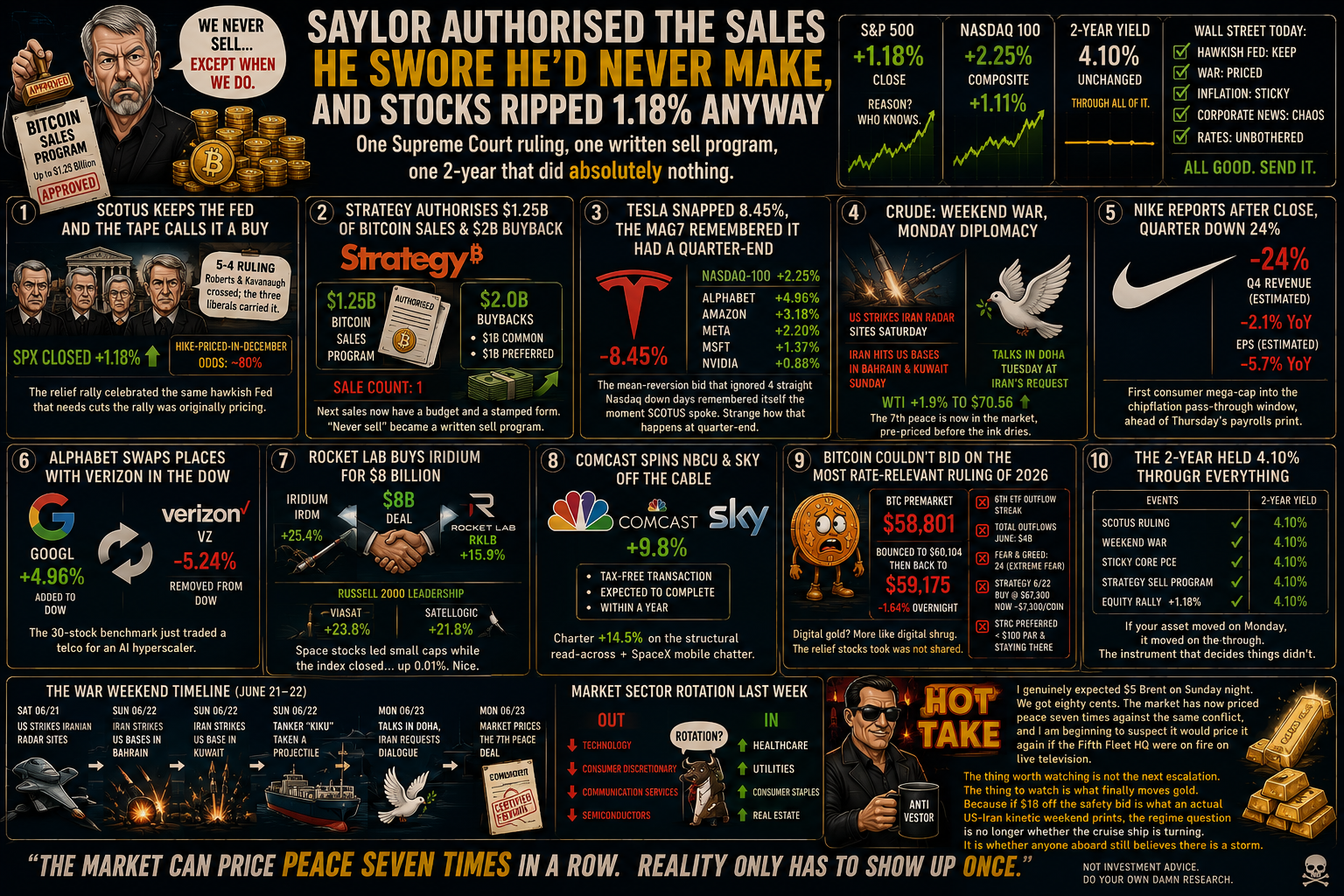

A 5-4 ruling, a 1.18% equity rally, and the corporate Bitcoin treasury that authorised a billion of sales the same morning.

⚓ Weathervane: The Fed has turned hawkish for the cycle. The committee’s own dots flipped from a cut to a hike under Warsh, and higher-for-longer is now confirmed by the instrument. The unconfirmed second leg is risk appetite: equities are still trading as if the turn isn’t real.

Ahoy there, Trader! ⚓️

Ahoy there, Trader! ⚓️

It’s Phil…

I’ve been staring at Monday’s tape and I’m not sure I have the right read yet. Let me work through it out loud and see if you spot what I’m missing.

The setup. The Supreme Court ruled 5-4 Monday afternoon that President Trump cannot, for now, fire Fed Governor Lisa Cook. Roberts joined Kavanaugh and the three liberals. The Warsh committee, which has spent the year pricing cuts out and now prices a December hike at roughly 80%, just had its independence preserved. The S&P closed up 1.18% at 7,440.44. The Nasdaq-100 closed up 2.25%. The 2-year held 4.10%. Six hours earlier, Strategy’s board authorised up to $1.25 billion of Bitcoin sales, plus $2 billion of buybacks, plus a 12% coupon hike on a preferred that has spent weeks below the $100 par.

Here is the question that puzzles me.

How does the same Fed independence ruling that ripped equities by 1.18 percent leave Strategy authorising 1.25 billion of Bitcoin sales and the rest of crypto refusing to bid?

The textbook reads it this way. Fed independence preserved should support the dollar, firm the long end, hold gold steady on the monetary-discipline read, leave equities mixed, and pressure Bitcoin. The tape did the opposite on the first three. The dollar softened 0.25%, the 10-year barely moved, gold fell 0.24%, and equities ripped, led by Mag7 names that need cuts more than almost anything in the market.

Three assets read the same news three different ways. The 2-year said “already priced.” The S&P said “the hike path is credible, safe to chase quarter-end.” Strategy’s board said “the dear-money regime is structural; fund operations out of the reserve, not out of more issuance.” Bitcoin sat at $59,175 and said nothing.

I lean towards the 2-year, because the instrument has now held its level through PCE, a weekend kinetic exchange, the SCOTUS ruling, and a corporate Bitcoin sell authorisation. When the benchmark stops reacting to scheduled catalysts, it’s either anchored to a strong forward view or warning of a dislocation. The longer 4.10% holds, the more it reads as anchored.

If the 2-year is right, the equity rally is a quarter-end positioning artefact in the costume of a relief story, and Strategy’s authorisation is the more honest read from inside the corporate-treasury weather. Thursday’s NFP is the live tell: a soft print that eases September hike odds confirms equities; a print that doesn’t, plus a fortnight of crypto refusing the next leg up, confirms the corporate read.

Three readings of one ruling, only one consistent with the regime banner that opens this letter. I’m watching which one persists.

Phil’s Musing

The honest signal is that risk appetite at the corporate-treasury level is rationing itself. Strategy’s $1.25B authorisation isn’t a tactical sale; it’s a budget line. If the slow-moving regime is turning, this is the kind of small structural admission you see first. The cruise ship hasn’t turned yet, but a senior officer just walked onto the bridge with a different chart and didn’t make eye contact. I’d watch what other corporate Bitcoin treasuries do this fortnight before calling the turn.

Happy trading,

Phil

Less Brain, More Gain

…and may your trades be smoother than a cashmere codpiece

P.S. – Phil’s Footnote – The thing I keep getting stuck on is why gold didn’t bid into the SCOTUS ruling. Fed independence preserved should be the cleanest possible case for gold as monetary discipline, and gold actively fell. Either gold has fully decoupled from its monetary-discipline character and become a pure duration-rate trade, or the ruling carried implications about the rate path that I haven’t yet fully understood. Probably the first. Possibly both. Still chewing on this one.

🛠 Desk Notes | Tuesday, June 30, 2026

Raw mechanism read, catalyst slate, divergence flags. Observations only, never trades.

Live tape state

SESSION BRIDGE: prior session (Mon Jun 29) full reaction SPX +1.18% to 7,440.44, Nasdaq-100 +2.25%, Nasdaq Composite +1.11%, Dow +0.59%; tech-mean-reversion driven by the SCOTUS-Cook 5-4 ruling preserving Fed independence (Roberts and Kavanaugh crossed) and Strategy’s $1.25B BTC monetisation authorisation landing 12:35 UTC. Live premarket Tue Jun 30: ES +0.01%, NQ -0.03%, VIX 17.64 (-0.11%), gold -0.24%, BTC -1.64% to $59,175, DXY -0.25%, WTI +0.08% to $70.81. Threshold: soft, with manual catalyst flag (Strategy authorisation landed post-Part-157 ledger refresh).

The cash session was the move. The premarket is the rest position. Read the premarket as a reaction to a +1.18% close on a Fed-independence ruling, not as a standalone story.

Mechanism read

Front end (2-year): Held 4.10% through PCE Thursday, the weekend kinetic exchange, the SCOTUS-Cook ruling Monday afternoon, and the Strategy $1.25B sell authorisation in the morning. Four consecutive scheduled tests, no flinch. CME FedWatch reads roughly 80% odds of a December hike; July hike odds firmed slightly to roughly 30% post-PCE. The instrument has now held its level through fundamentally everything offered it this fortnight.

Long end (10-year): 4.376% Monday close, up roughly 1bp on the day. The 2s10s spread holds +27bp, term-premium not the dominant story. The long end is rotating with risk appetite at the margin; the 2-year is not rotating with anything.

Dollar (DXY): 101.111, softer by 0.25% overnight. Quiet softening despite the SCOTUS rally; the dollar is not confirming the equity move with conviction, suggesting the equity bid was domestic positioning more than a flight-to-USD story.

Volatility (VIX): 17.64, down 0.11% overnight from 18.41 Friday close. The risk-on read was confirmed by vol compression. No disagreement between equities and vol on Monday’s relief.

The one artery driving the tape: the SCOTUS-Cook ruling preserved Fed independence at the moment markets were pricing the highest Fed-political-risk in a generation. The equity rally is a relief rally about the credibility of the hike path itself, not about cuts arriving. The 2-year confirms this exactly: rate-path credibility went up, the rate path did not change.

Strategy’s $1.25B authorisation is the second-leg confirmation we have been watching for in the Warsh trajectory thread. Risk appetite at the corporate treasury level just admitted it cannot fund itself off Bitcoin alone in a dear-money regime. Capital structure won. The instrument was right; the leadership lever turned out to be neither geopolitical (Hormuz survived) nor data (PCE held) but corporate capital structure choices forced by duration.

Forward catalyst slate

- Tuesday Jun 30, today: US-Iran Doha talks at Iran’s request. Nike Q4 earnings after the close (analysts -2.1% YoY revenue, -5.7% EPS). Quarter-end markings.

- Wednesday Jul 1: ADP private payrolls preview ahead of Thursday NFP. Q3 begins, fresh positioning window.

- Thursday Jul 2: US NFP June print. Consensus 114k jobs (vs 172k May), unemployment unchanged at 4.3%. This is the week’s main rate-path test. Bond market closes early.

- Friday Jul 3: Bond market and most US markets closed for Independence Day.

- Through July: Strategy 8-K window for any actual use of the $1.25B authorisation. Mag7 July guides (META, GOOG, MSFT, AMZN) for chipflation pass-through. Strategic Bitcoin Reserve blueprint due before 22 July under standing executive order.

Divergence flags

- Equities took Fed-independence-preserved as risk-on; Bitcoin did not. SPX +1.18% with BTC trading $58,801 low to $60,104 close (then $59,175 overnight). The most rate-sensitive risk asset refused the relief that stocks accepted. This is the cleanest cross-asset divergence in the print and the central observation of the edition.

- The 2-year is now a non-event indicator. Four consecutive macro catalysts (PCE, weekend kinetics, SCOTUS, Strategy news) have failed to move it. When a benchmark stops reacting, it is either dead-anchored to a strong forward view (the read) or warning of a coming dislocation. The trajectory says anchored.

- Gold sold off into a Supreme Court ruling about the Fed. Gold -0.24% on a day equities ripped on Fed-independence-preserved. The traditional safe-haven did not bid on what should mechanically be a positive structural story for the dollar’s monetary plumbing. Gold’s recent character is duration-sensitive, not safe-haven; the print confirms.

- Comms-sector internal shuffle masks breadth at the index level. Alphabet entered the Dow, Verizon exited; Comcast spun off NBCU and Sky; Charter caught a 14.5% bid on read-through. Three corporate-action stories layered into one tape make the breadth statistics look noisier than the underlying flow.

- STRC’s 12% coupon hike is the loudest tell from the Strategy package. The $1.25B BTC sell authorisation gets the headlines, but the preferred dividend ramp is the structural confession: the preferred has refused to hold the $100 par for weeks, and a 12 handle on the coupon is the size of fix a fixed-income manager runs to prevent a forced sale.

Carry-over note (§10.6)

The §8.4.1 threshold tripped soft (+1.18% prior session) plus a manual catalyst flag for the Strategy authorisation landing after the Part 157 ledger refresh. The carry-over rides the tiers:

- AVE: the deflating one-number callback (“sale count was one; now there is a budget”).

- Snippet: the HotTake on the 2-year-as-non-event indicator.

- Macro Edge: the dissection of how Fed-independence-preserved was supposed to be a positive structural story for stocks AND bonds AND gold AND Bitcoin, and only stocks bothered to celebrate.

Part C – Regime tracking

⚓ Weathervane: UNCHANGED. The Fed has turned hawkish for the cycle; the committee’s own dots flipped from a cut to a hike under Warsh, and higher-for-longer is now confirmed by both the instrument AND the institutional posture (Strategy’s authorised $1.25B sell program is the corporate-treasury equivalent of the 2-year holding 4.10%). The unconfirmed second leg is risk appetite at the index level: equities still trading as if the turn isn’t real, even as the Strategy package shows institutional risk-taking is rationing itself.

Today’s note: Monday’s equity bid IS the second-leg confirmation problem in its purest form. The market took Fed-independence-preserved as risk-on, the corporate Bitcoin treasury took it as duration-too-long-to-sit-out, the 2-year took it as already-priced. Three readings of the same news, only one of them consistent with the regime banner. The cruise ship hasn’t turned; the speedboat is performing a convincing rendition of calm seas with a corporate sell program filed in the corner.

⚓ REGIME FLAG (internal tripwire): No fresh flag today. Warsh thread remains the confirmed multi-week pattern break. Candidate threads still below threshold:

- Chipflation as a regime story: still below threshold. Apple sticker plus Microsoft’s Xbox hike plus the Mag7 July guides not yet a pattern. Waiting on July guides.

- Hormuz complacency as a regime story (logged Mon Jun 29 Part B): still below threshold. One quiet weekend not yet a pattern. Doha talks today are the early read on whether the structural-de-pricing continues.

- Corporate treasury capitulation as a regime story (NEW, candidate, logged today Part B): Strategy’s $1.25B sell authorisation is a single corporate event. Whether other corporate Bitcoin treasuries follow (Block, Tesla treasury, MARA) is the trigger. Below threshold for now.

Sensitivity read (§17.3): UNCHANGED, holding loose-leaning. Three candidate threads now tracked as Part B shots rather than as fired flags. Phil to agree or instruct tighten/loosen.

Public tell status: NOT triggered. “Hoist the mainsail” stays holstered.