A record memory-price quarter meets a hawkish Fed, a Dow endorsement, and a Nasdaq that opened the tape lower into the news.

⚓ Weathervane. The Fed has turned hawkish for the cycle. The committee’s own dots flipped from a cut to a hike under Warsh, and higher-for-longer is now confirmed by the instrument. The unconfirmed second leg is risk appetite: equities are still trading as if the turn isn’t real. Unchanged this session. Samsung’s print did not turn the vane; it added a sixth leg to it.

Ahoy there, Trader! ⚓️

Ahoy there, Trader! ⚓️

It’s Phil…

Four days on the tender and I return to a tape that has done more work than I have. Payrolls missed. A bill was signed. A Dow name climbed 7.7% on a bell-ceremony endorsement. A rocket company joins an index today with four billion dollars of forced buying knocking. And overnight the memory vendor at the top of the semiconductor stack booked the biggest tech quarter that has ever been booked. I want to be careful about which of those is the wind and which is the wake.

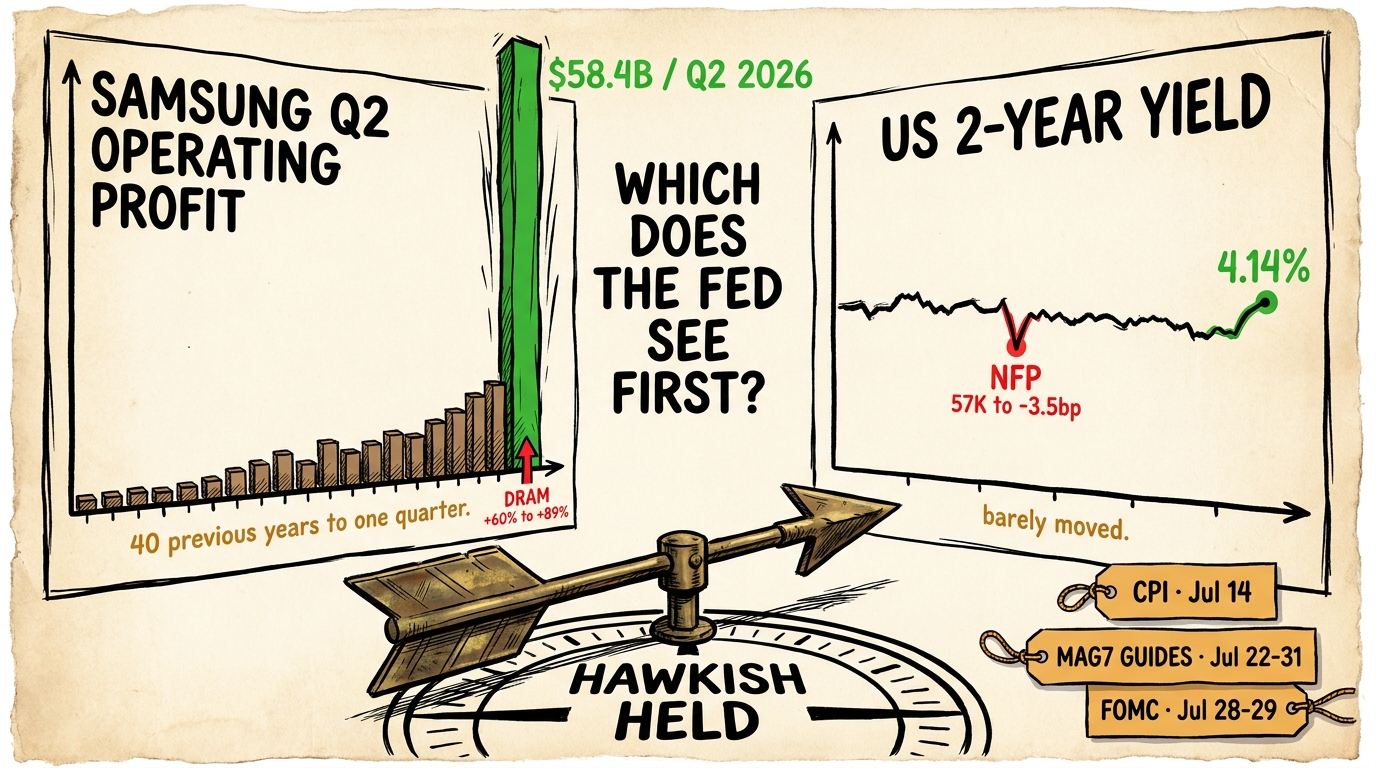

Today the question I keep sitting with is this. When Samsung books the largest quarterly profit in tech history on 60 to 89 percent memory hikes, whose margin was that, and does the Fed see chipflation on CPI or a Mag7 guide miss first?

Let me walk the dots as I read them. Samsung’s preliminary Q2 result is 89.4 trillion won, roughly $58.4 billion, a nineteen-fold jump against the same quarter a year ago and, per the wires, the largest single-quarter operating profit any technology company has ever reported. The driver is not new. It is memory pricing. DRAM prices rose 60% to 89% during the quarter. AI accelerators cannot ship without HBM, and HBM is a supplier-constrained good with three producers who watch each other closely. So Samsung raised, shipped, and booked a record.

That memory did not become free at the buyer. Nvidia, Apple, Microsoft, Google, Meta, and every hyperscaler datacentre operator paid the higher price. Which means one of two things happened inside their quarter. Either the higher input cost was absorbed at the margin, and July guidance says so, or it was passed to the end product, and the CPI eventually says so. Textbook says both, in some ratio, over some lag. The interesting question is not whether. It is which the Fed sees first and how it reacts.

Here is the piece I find genuinely puzzling and I will name it. The instrument the Fed watches most closely for inflation transmission is the two-year yield, and the two-year barely moved on a very soft payroll print last Thursday. Three-and-a-half basis points, under my own five-point falsifier. That tells me the front end is not being led by growth data right now; it is being led by the Fed’s stated intent. Which then implies that if the Fed sees chipflation on the CPI print before it sees a Mag7 guide miss, the front end may already be waiting for it. If it sees the guide miss first, the reaction function may lean the other way (softer growth, softer path).

Textbook expectation says a vendor-node margin capture should show up first in the customer’s margin, second in the end-product price, third in the CPI, and only fourth in the reaction of a central bank. Reality this cycle has repeatedly compressed that lag: the SCOTUS-Cook ruling, the war weekend, the Sintra encore, all shortened the transmission distance rather than lengthened it. So I lean toward “we see the Mag7 guide miss inside July, and the CPI print in October or November.” I would not bet the boat on that lean.

The piece I am not sure about, and I will say so, is whether one guide miss inside a single mega-cap is enough to matter to the tape, or whether the market needs the pattern before it prices it. Nasdaq futures opened 0.88% lower into Samsung’s release, which reads to me like the tape is already pricing at least one guide miss. That is a strong signal, and it is also the kind of signal that has been wrong before.

Phil’s Musing

The chipflation thread on the ledger is now moving faster than I thought it would. Samsung’s booked print is the first hard evidence that the vendor node is capturing the margin at record scale, and the tape opened red into it without waiting for the confirmation from a hyperscaler’s own quarterly print. I think we are one Mag7 July guide from an upgrade of chipflation from candidate thread to tracked structural thread. If Microsoft, Meta, or Alphabet names memory as a headwind on the July call, I would want to consider a slower-horizon lean into memory suppliers and away from the buyers, and I would want to think about whether the September FOMC dot revision actually holds or whether the room needs to add a hike. If none of them name it, we hold the current setting and let the CPI print in October adjudicate. Either way, this is the first regime-flag candidate I can see going hard inside a fortnight.

Happy trading,

Phil

Less Brain, More Gain

…and may your trades be smoother than a cashmere codpiece

P.S. – Phils Footnote Four days off the desk and I come back to find that the memory guys booked more in a quarter than I have earned in my entire career, and Nasdaq futures opened red into it. That is a market doing accounting in real time, and it is nice to see it happen. I am still working out whether the “front end holds while the CPI catches up” pattern is a coincidence of the last two years or a real feature of how this cycle transmits. If you have a view, tell me. I read them.

🗒️ Desk Notes | Tuesday, July 7, 2026

Raw briefing feeding Analysis Edge. Observations only, no named trades.

Pre-drafting bridge (§8.4)

SESSION BRIDGE: prior session (Mon Jul 6) full reaction SPX +0.72% to record 7,537.43, Dow +0.29% to record 53,055.91, Nasdaq Composite +1.12% to 26,121.16, no meaningful overnight tail into the Samsung print at 06:50 ET Tuesday; live premarket Tue Jul 7 04:12 ET ES -0.21%, NQ -0.88%, VIX +2.25% to 15.91, WTI +1.15% to $69.34, gold -0.45% to $4,148.6, BTC -1.44% to $63,082; threshold: soft on the day, HARD on the multi-session carry-over.

Carry-over context (four sleeps since Part 160). Phil’s last edition previewed Thu Jul 2 pre-NFP. In the intervening window: (1) NFP printed 57K vs 110K expected with April and May revised down 74K combined; unemployment fell to 4.2% via a labour force participation drop to 61.5%; two-year yield eased 4bp to 4.14%, ten-year eased 2bp to 4.46%, Fed September hike odds slid from 64% to 50%. (2) Fri Jul 3 US markets closed for the Jul 4 observed holiday. (3) Sat Jul 4 the president signed the One Big Beautiful Bill Act, launched the Trump Accounts children’s savings programme, and a July 2 CNBC interview aired in which he said he expects Musk to donate SpaceX stock to the programme. (4) Mon Jul 6 Dow closed at record 53,055.91 after Dell rose 7.7% on Trump’s “go out and buy a Dell computer” at a joint NYSE-Nasdaq bell ceremony; SMH ran 2.7% at the open on WDC +7%, TDY +2.8%, MRVL +1%, ORCL +2.5%. (5) Overnight into Tue Jul 7 06:50 ET, Samsung Electronics released preliminary Q2 operating profit 89.4 trillion won ($58.4 billion), 19-fold YoY, the largest single-quarter operating profit any technology company has ever reported. Nasdaq futures were down 0.88% at 04:12 ET into that print. That is the carry-over that fires today’s editorial.

Mechanism read

What moved (four instruments, plus the spine number).

- Two-year: 4.176% pre-NFP Thu → 4.14% post-NFP Thu → held 4.14% into Mon close. Move on the print: about 3.5bp, just under the 5bp falsifier we set for the front-end anchor thesis.

- Ten-year: 4.481% Wed Jul 1 close → 4.46% Thu post-NFP → 4.47%-4.48% Mon Jul 6. Long end gave back most of the Sintra +7bp steepening on the softer growth signal, then held.

- DXY: 100.855 Tue premarket, essentially flat on the four-session window. Dollar did not reprice the labour print materially.

- VIX: 16.63 Wed Jul 1 → held mid-16s through NFP Thursday (did not blow out) → 15.91 Tue Jul 7 premarket, up 2.25% intraday but continuing the compression trend. Vol crush deepened, not reversed.

- The spine number that changed today: Samsung Q2 operating profit at 89.4 trillion won ($58.4B), 19-fold YoY, on 60% to 89% Q2 DRAM price hikes. Chipflation as a margin transfer, printed at the vendor node.

What it implies (causal read). The front end refused to move materially on the softest NFP print in months, and the vol curve refused to bid despite what looked like a data catalyst. Both instruments read the miss as noise inside the participation-drop mechanism, not as evidence the Fed had a reason to pivot. The Fed’s own posture (Warsh Sintra “prices are too high”) is not being challenged by the tape. Then Samsung’s print landed and confirmed the argument the ledger has been running for a fortnight: the AI-memory margin is being captured at the vendor node, not the model node. The premarket NQ -0.88% is the tape doing basic accounting. Someone bought that memory. Someone’s July guide reflects it. This is chipflation transmission in real time, and it is showing up as a margin transfer first, exactly as the Part B shot from Jun 26 argued.

The one artery. The memory-price capture at Samsung is today’s driver. Fed path relief is the secondary story, and it stalled inside its own five-basis-point envelope. Dell, SpaceX, Trump Accounts are set pieces on the tape, not mechanism.

Forward catalyst slate

- Wed Jul 8 14:00 ET: FOMC minutes (June meeting). Live falsifier for the “hawkish-locked-in” trajectory if the room reads more divided than Warsh’s Sintra tone suggested.

- Wed Jul 8 AM ET: Delta Air Lines Q2 earnings. First transportation read into the demand debate.

- Thu Jul 9 AM ET: PepsiCo Q2 earnings. Consumer-margin read; watch for input-cost commentary.

- Fri Jul 10: SK Hynix ADR debuts on Nasdaq, target raise near $28 billion. Second memory print landing after Samsung.

- Mon Jul 14: June CPI. Live falsifier for the chipflation transmission thesis; watch core goods with tech-heavy items.

- Jul 15: Strategy STRC 12% coupon payment date; MSTR live equity read.

- Jul 22: Tesla Q2 full earnings after 480,126 delivery beat and Thursday’s 7.3% sell-off.

- Jul 28-29: FOMC decision, dot plot revised. This is the September-vs-December live falsifier for the Warsh path.

- Jul 30: Samsung Q2 full results with segment breakdown; the 60% to 89% DRAM hike gets a formal channel readout.

- Rolling: Mag7 July guides. First one to name memory cost as a margin driver validates the transmission thesis.

Divergence flags

- Samsung record profit vs Nasdaq red premarket. The largest tech quarter ever printed and NQ futures traded 0.88% lower. The tape is reading the record correctly as a margin transfer, not a sector-wide melt-up. Watch which specific Mag7 name breaks first on guidance.

- BTC price up, ETF flows down for a seventh week. Price is $4,300 above the late-June low with a seven-week outflow streak. Bounce arrived without a flow catalyst. Someone is bidding that is not the wrapped-institutional bid the last two years relied on. Divergence hardens if next week’s flow print stays negative and price stays above $60k.

- Dow at record vs breadth still thin. The Dow made another record Monday on a single-stock presidential endorsement. Small caps are back above 3,000 but broad market breadth has not confirmed the cap-weight leadership. Watch for a real Russell push into new highs versus another single-name Dow event.

- NFP soft print vs unemployment falling. Payrolls missed by half, and the unemployment rate went down because 700,000 people left the workforce faster than jobs disappeared. Fed reaction function reads the headline; the front end is reading the internals. Two-year stuck at 4.14% is the tell.

- VIX bidding into a Fed-minutes week from a low base. VIX 15.91 with a 2.25% intraday bid is not a blow-out. It is a room adding a small hedge into Wednesday’s minutes and next week’s CPI. Watch for a break of 17 into either print.

Part C – Regime tracking & the weathervane (§17)

⚓ Weathervane

UNCHANGED, now load-bearing on six legs (instrument, court protection, corporate posture, quarter-end equity disagreement, hawkish encore, chipflation as vendor-capture). Current read: “The Fed has turned hawkish for the cycle. The committee’s own dots flipped from a cut to a hike under Warsh, and higher-for-longer is now confirmed by the instrument. The unconfirmed second leg is risk appetite: equities are still trading as if the turn isn’t real.”

Today’s note. Samsung’s preliminary print puts the chipflation leg on public display for the first time as a booked margin, not a forecast. The vendor node captured the AI-memory margin at record scale on 60% to 89% Q2 DRAM hikes; the Nasdaq futures read the transmission correctly. The rate impulse (soft NFP) tried to add relief and stalled at 3.5bp on the two-year. The equity index is still arguing harder against the cruise ship’s heading than any other cross-asset thread, and the vol curve is now quietly walking in behind it. Speedboat celebrating a Dow record on a Dell endorsement. Cruise ship still pointed the other way. Deckhands starting to compare notes.

⚓ REGIME FLAG

- CONFIRMED on Warsh thread; no new flag fired today. The hawkish-for-the-cycle turn remains the confirmed multi-week pattern break.

- Candidate threads worth watching:

- Chipflation as a regime story: candidate STRENGTHENING sharply on Samsung’s booked print. Trigger for upgrade to tracked structural thread: first Mag7 July guide that names memory input costs as a margin headwind. Watch Microsoft, Meta, Alphabet.

- Hormuz complacency as a regime story: candidate STRENGTHENING toward confirmation. OPEC+ fifth consecutive monthly add for August, Brent held $72 pre-war level, Iran-US MoU intact on paper. One clean cycle from upgrade.

- Corporate Bitcoin treasury capitulation: below threshold, candidate strengthening. Strategy STRC coupon window live; still need a second corporate filing.

- Vol regime compression at quarter-end: still LIVE. Tuesday premarket VIX 15.91 up 2.25% but from a low base; the crush has deepened rather than reversed post-NFP. Trigger: vol holds sub-17 through Fed minutes AND June CPI.

- Sensitivity read (§17.3): UNCHANGED, holding loose-leaning. Four candidate threads tracked as Part B shots rather than fired regime flags. Chipflation has strengthened most this session and is the closest to a hard flag. Phil to agree or instruct tighten/loosen.

- Public tell status: NOT triggered. “Hoist the mainsail, the macro winds have changed” stays holstered. Next candidate trigger window: Mag7 July guides (rolling) + June CPI (Mon Jul 14) + FOMC (Jul 28-29). If chipflation lands on the print AND FOMC keeps its dots hawkish, the language shifts.