Bitcoin’s worst ETF month found Saylor’s breaking point.

Ahoy there, Trader! ⚓️

Ahoy there, Trader! ⚓️

It’s Phil…

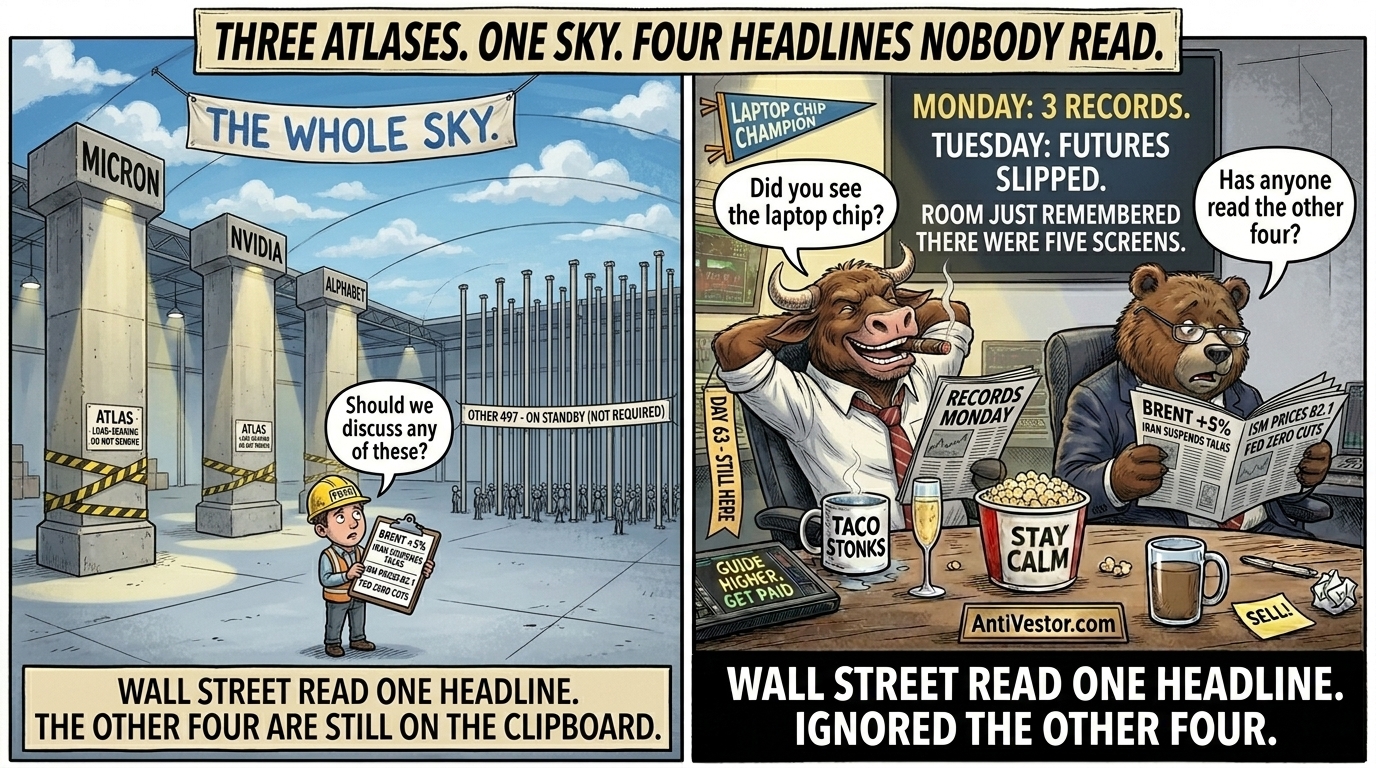

Wall Street Reads One Headline, Ignores the Other Four A laptop chip outran an oil shock, a hawkish Fed, and the market’s loudest permabull. Same day.

Monday handed Wall Street five things to think about. It picked the cheerful one. The S&P closed at 7,599.96, the Nasdaq at 27,086.81, the Dow at 51,078.88, three records stacked on a single Nvidia chip that runs AI on laptops.

Dell rose 10%. HP added 8%. Intel, which used to own this category, fell 4% and was not invited. That was screen one. Screens two through five were less fun. Brent jumped 5% above $95 after Iran suspended talks with Washington and floated closing the Strait of Hormuz.

Trump said the talks would work out well, which is the sort of thing one says when the other side has just put down the phone. ISM manufacturing beat at 54 with prices stuck at a scalding 82.1, which is the sound of rate cuts dying.

Markets now price zero Fed cuts in 2026, with Kevin Warsh’s first meeting on June 17 looming over a tape that has stopped pretending easing is coming. And Bitcoin opened June near $73,000 while Michael Saylor’s Strategy, of all sellers, sold.

The tape, having weighed an oil shock, a hawkish Fed and a capitulating permabull, bought a laptop instead. Tuesday’s futures finally slipped, which is roughly what happens when the room remembers there were five screens.

Get The Complete Premium Popper System – Automation Included

Your entry ticket to consistent SPX income. Inside: the exact setup, rules, and checklists I trade daily – for less than the cost of lunch. Easily actionable.

Get The Premium Popper System – Click Here

Stock Market Edge

Three Stocks Are Holding Up the Whole Sky The tape is standing on Micron, Nvidia and Alphabet, and hoping nobody looks down.

- Premarket snapshot: All three indexes printed records Monday, with Nvidia near $224 doing the heavy lifting after its RTX Spark launch and a 20% run for 2026. Futures slipped Tuesday, the market’s way of admitting it had a large lunch. The records were real; the breadth holding them up was mostly rumour.

- Sector rotation: Technology led, because technology always leads now. Dell rose more than 10% and HP 8% as anointed Nvidia partners, while Intel fell 4% for the crime of being yesterday. Energy was the only other green sector, which tells you the day’s other story was a fire nobody wanted to discuss.

- Earnings or guidance: ISM beat at 54 and new orders hit 56.8, but the prices index sat at 82.1, hot enough to settle the cut debate for good. Evercore’s Julian Emanuel notes Micron, Nvidia and Alphabet drive over 40% of this year’s S&P EPS revisions. His 7,750 target rests on three companies and a prayer.

- Cross-asset nuance: Brent added 5% above $95 on the Hormuz threat, the one macro input the equity tape declined to acknowledge. Yields held firm, the dollar held bid, and zero-cut pricing hardened into consensus. Every asset class but stocks spent Monday quietly bracing. Stocks spent it shopping.

📊 There’s a level on SPX I’m watching closely this morning. My full analysis briefing has it – plus what happens if we hold it, and what happens if we don’t. [Read it here →]

Crypto Market Edge

Bitcoin Bleeds, and Its Loudest Believer Joins the Sellers Saylor spent years saying never sell. June opened with the invoice.

- Price snapshot: Bitcoin held a $72,500-$73,200 range to open June, with Ethereum face-down near $2,000. Total market cap slipped 1.4% to about $2.46 trillion on roughly $70 billion of volume. Bitcoin dominance near 59% is less a flex than a measure of where everyone hid.

- Flows & positioning: US spot Bitcoin ETFs bled $2.43 billion in May, the year’s worst month, with BlackRock’s IBIT leading the walk to the exit. Combined Bitcoin and Ethereum ETF selling has topped $2 billion since May 14. Put/call ratios of 0.84 and 0.74 confirm pain while politely withholding panic.

- Leadership & rotation: Bitcoin’s 59% dominance mostly means it is losing slowest, which now passes for leadership. Ethereum sits roughly 50% below its October peak and its ETFs have bled for over 14 straight sessions. Altcoins did what altcoins do in a downturn, which is worse.

- Catalysts & roadmap: Strategy sold bitcoin for the first time since 2022 to cover preferred dividends, quietly retiring the never-sell slogan it built a brand on. The June quarterly expiry looms next. Support sits at $70,000, the reclaim at $73,869-$75,000, and Warsh’s June 17 meeting hangs over the lot.

TL;DR – The Bottom Line

- Three indexes closed at records Monday on one Nvidia laptop chip; Dell rose 10%, HP gained 8%, Intel fell 4%, and by Tuesday the futures had sobered up and slipped.

- Micron, Nvidia and Alphabet drive over 40% of 2026 S&P earnings revisions, which makes the record-breaking rally a technically impressive three-man job with a 7,750 target.

- Brent spiked 5% above $95 after Iran cut talks and threatened Hormuz; Trump assured everyone it works out, and the equity tape simply chose to believe him.

- Markets now price zero Fed cuts in 2026 with ISM at 54 and prices at 82.1; Warsh inherits a hike-risk economy at his first meeting on June 17.

- Bitcoin opened June near $73K as Strategy sold for the first time since 2022, proving the only thing more flexible than the price is the word never.

📌 Fun Fact

The Stock Trader’s Almanac records the S&P 500 having just completed its 14th nine-week winning streak since 1930. That places the event roughly once every seven years on average, though in practice the spacing has been highly uneven – clusters in the 1940s, 1950s, and 1960s, then long droughts.

The just-completed streak ran from 27 March to 29 May 2026, posting +19.0% over the nine-week period. That makes it the strongest 9-week streak in the data set going back nearly a century. The previous strongest was the November 1985 occurrence at +15.85%, followed six months later by a +22.7% extension.

The historical pattern after these streaks is short-term softness, long-term continuation. The one-week average post-streak is -0.84%, the median -0.91%, with only 31% of occurrences seeing immediate further upside. The four-week picture is constructive: 77% positive, average +1.21%. Six months out, 77% positive, average +5.48%. Out of 13 historical occurrences (excluding the current one) the six-month return was negative only three times, including the worst at -15.08% after the May 1957 streak.

In summary: history says the immediate aftermath is mixed-to-soft, the medium term constructive. The Almanac, having published this, takes no view on which side wins.

[Source: Stock Trader’s Almanac historical data, Hirsch Holdings Inc., stockradersalmanac.com, public]

Meme of the Day:

Happy trading,

Phil

Less Brain, More Gain

…and may your trades be smoother than a cashmere codpiece

p.s. There are 3 ways I can help you…

- Option 1: The SPX Income System Book (Just $12)

A complete guide to the system.

Written to be clear, concise, and immediately actionable.

>> Get the Book Here

- Option 2: Full Course + Software Access – 50% off for Regular Readers – Save $998.50

Includes the video walkthroughs, tools for TradeStation & TradingView, and everything I use daily. Plus 7 additional strategies

>> Get DIY Training & Software

- Option 3: Join the Fast Forward Mentorship – 50% off for Regular Readers – Save $3,000

>> Join the Fast Forward Mentorship – trade live, twice a week, with me and the crew. PLUS Monthly on-demand 1-2-1’s

No fluff. Just profits, pulse bars, and patterns that actually work.