You Were Promised Four Things. The Numbers Say All Four Are Broken.

The Salary Trap. The Pension Mirage. The Empty Desk. And…

Ahoy there, Trader! ⚓️

Ahoy there, Trader! ⚓️

It’s Phil…

The salary that used to buy a house now barely covers the rent. The pension that was supposed to last your retirement runs out in November. The inflation rate the government keeps quoting is not the one you pay at the till. And the job you assumed was safe is being quietly automated out from under you.

This is not a UK problem. It is not a US problem. It is not a Canadian problem.

It is the same problem in all three countries, and the data is now impossible to ignore.

If you are working hard, saving where you can, and still feeling like the ground keeps moving away from you, this article is going to explain why. It is also going to explain what people are quietly doing about it.

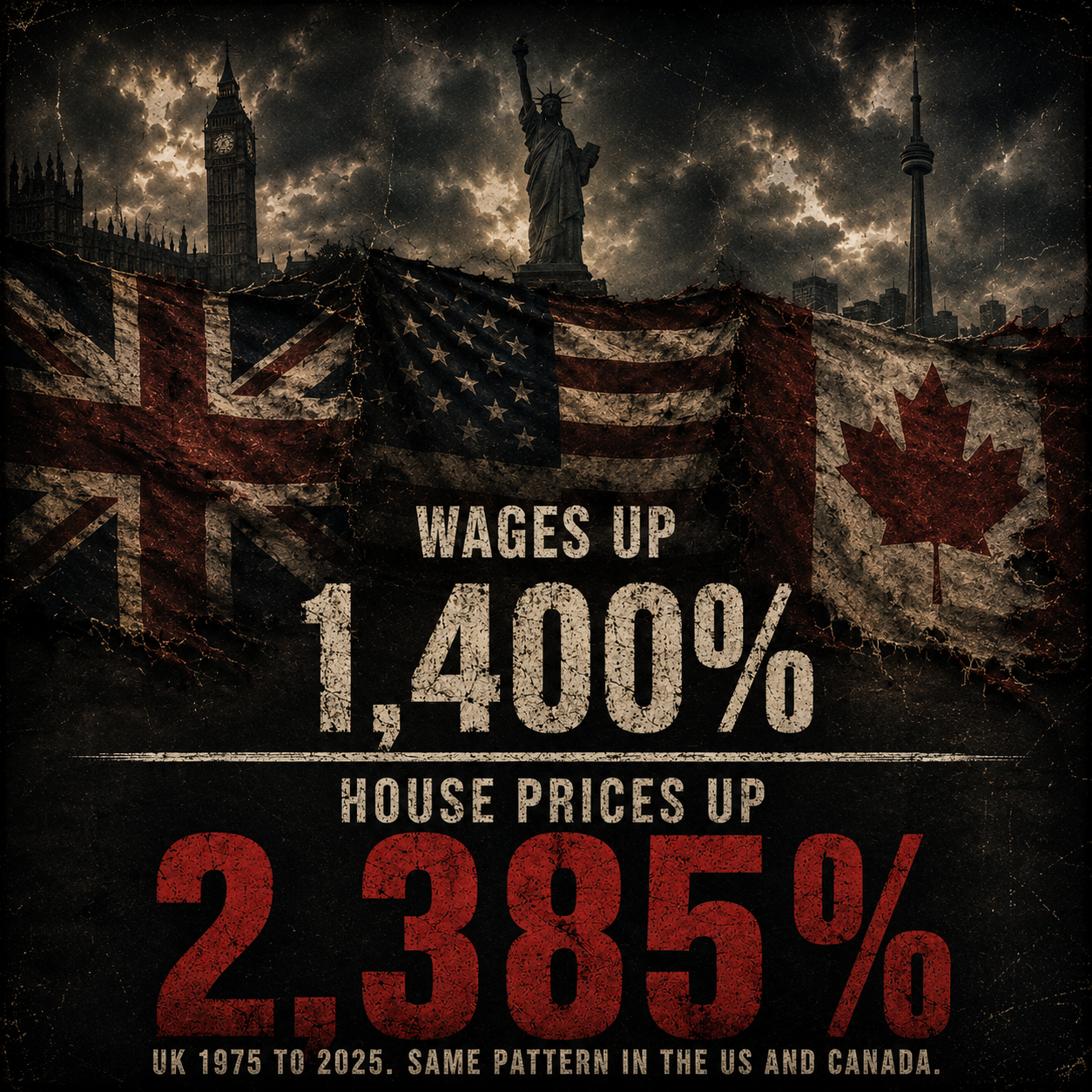

Promise One: A Salary Was Supposed to Buy You a House

The deal used to be simple. Work hard, earn a salary, buy a home. The numbers say that deal has been quietly cancelled.

In the UK, the average house in 1975 cost £10,978. In 2025, it cost £272,819. That is a rise of 2,385%. Over the same fifty years, salaries grew by 1,400%. If wages had kept pace with house prices, the average UK household would now earn £116,000. They earn £70,200. In 1975, a couple could save a deposit in eight months. Today it takes almost four years.

In the US, the median home cost $82,800 in 1985 and the median household earned $23,620. That was a ratio of 3.5 times income. In 2025, the median home costs $416,900 against a median income of $83,150. That is five times income, a record matching the pre-2008 peak. If American wages had kept pace with home prices since 1980, the median household would earn $115,224 today. They earn $83,730.

In Canada, the picture is worse. The national average home price now sits at roughly $670,000 against a median household income of $80,000. That is a ratio of 8.4 times income, putting Canada among the least affordable housing markets in the developed world. In Vancouver, owning the average home now costs 102% of the median income. Not the mortgage. The full cost of ownership. More than every dollar a household earns.

This is not a housing market problem. This is a salary problem. The salary has stopped doing the one thing it was supposed to do, and three different countries are looking at the same arithmetic.

Promise Two: A Pension Was Supposed to Pay for Your Retirement

Work forty years, retire on a pension, enjoy the time you have earned. The numbers say that deal has been quietly cancelled too.

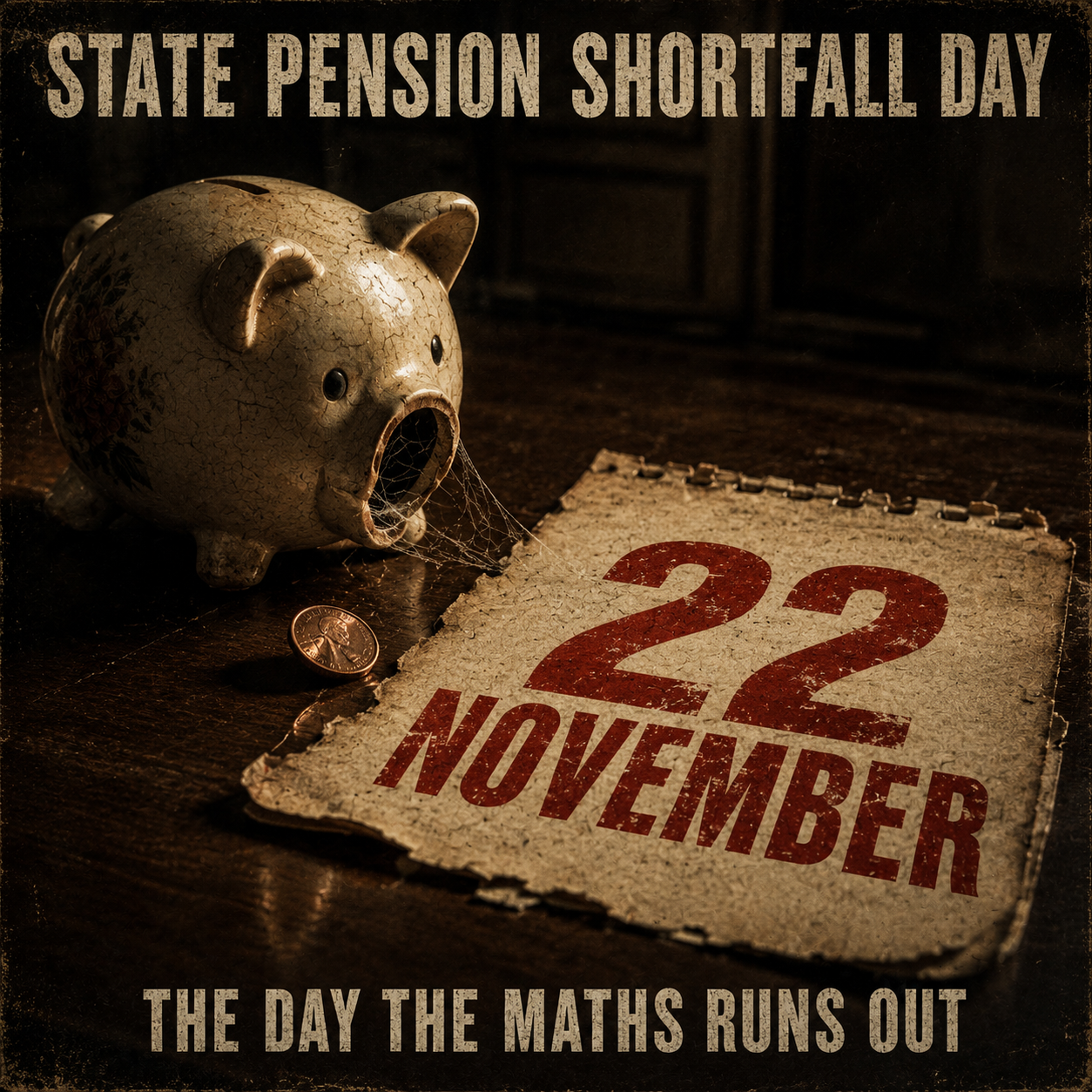

In the UK, 15 million working-age adults are currently under saving for retirement, according to the government’s own Pensions Commission. Without intervention that number reaches 19 million. The full new state pension pays £11,973 a year. The minimum standard of living in retirement, set by Pensions UK, requires £13,400. The state pension alone does not even cover the minimum standard. Industry research now publishes an annual “State Pension Shortfall Day,” the date in November when a pensioner relying solely on the state runs out of money. For a comfortable retirement, the average UK worker faces a lifetime shortfall of £115,768. In London, that shortfall is £177,847.

In the US, the picture is no kinder. The median 65-year-old retiree faces a $109,000 shortfall between what they have saved and what they will need. The median retirement savings for Americans aged 55 to 64, the group closest to retirement, is just $185,000. Industry consensus on the amount needed for a comfortable retirement is $1.26 million. Forty-six per cent of Americans report no retirement savings at all. The National Institute on Retirement Security puts the collective US retirement savings gap at between $6.8 trillion and $14 trillion. Retirees are now projected to outlive their savings in 41 states.

In Canada, the projected national retirement savings deficit reaches $13.4 trillion by 2050. With nearly 40% of the workforce now temporary or contingent, an entire generation is reaching retirement age with no employer-sponsored pension, no defined benefit, and increasingly thin personal savings.

The pension was the second leg of the deal. The data says the leg has gone.

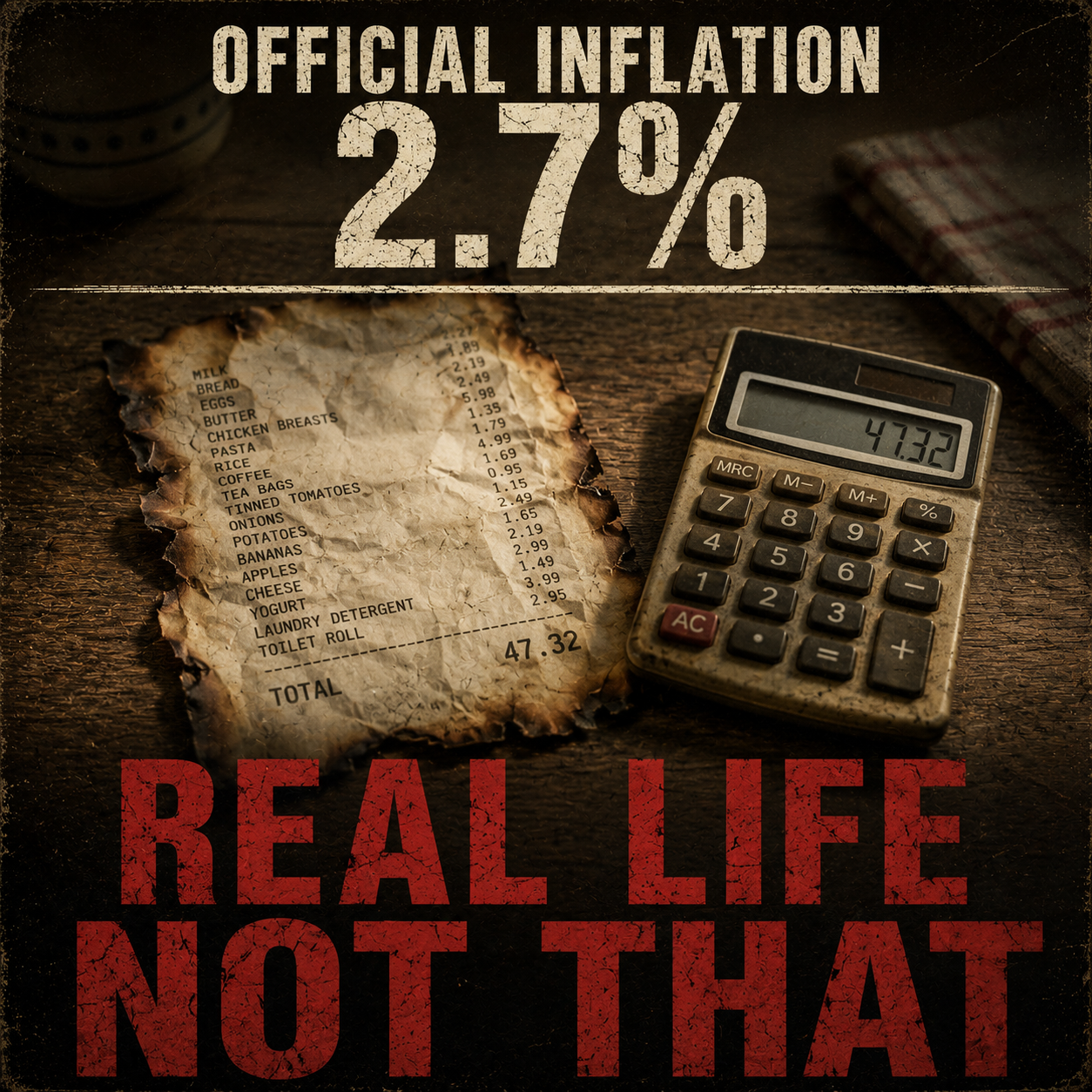

Promise Three: Inflation Was Supposed to Be 2%

The government tells you inflation is back under control. Your weekly shop, your rent, your energy bill and your council tax tell you something completely different.

The official numbers and the lived numbers stopped agreeing some time ago. In the US, real wages have shown almost no growth since 2020. Even with recent gains, inflation-adjusted weekly earnings since the pandemic began are essentially flat. As one analyst put it on CNBC in January 2026, “it feels like stagnation because it is.”

In the UK, real wages have stagnated for the longest sustained period since records began in the 19th century. Between 2008 and 2023, real wage growth averaged 0.1% a year. Over the last twenty-five years, real wages have grown by 16% in total, while housing has grown by 267%. Anything wage-denominated has stood still. Anything asset-denominated has run away.

In Canada, the gap is even starker. Real posted wages remain 2.5 percentage points below their January 2021 level. Cumulative home prices have risen 53% since 2015, while incomes have risen 13%.

This is the inflation that does not appear in the headline rate. The compounding gap between what the headline number says and what the price tag says. Anything you have to buy with your salary has compounded faster than your salary. Anything you would buy with capital, if you had it, has compounded faster still.

You are not imagining it. The arithmetic is doing it to you.

Promise Four: A Job Was Supposed to Be Safe

The newest of the broken promises, and the one most workers have not yet priced in. The data on AI displacement is no longer speculation. It is appearing in the hiring numbers right now.

In May 2025, the chief executive of Anthropic, one of the world’s leading AI companies, told the press that AI could eliminate up to half of all entry-level white-collar jobs within one to five years, with unemployment potentially spiking to 10 to 20%. Similar warnings have since come from the chief executives of Ford and JPMorgan. These are not technology critics worried about the future. These are the people building it, deploying it, and hiring against it.

The displacement has already started. Entry-level job postings in the US are down roughly 35% since January 2023. Goldman Sachs reports that employment for workers aged 22 to 25 in AI-exposed roles fell 6% between late 2022 and mid-2025. For young software developers specifically, the decline approaches 20%. Cornell University research found that US companies adopting AI tools cut junior hiring by 13%. In the first five months of 2025 alone, US employers announced 696,309 job cuts, an 80% jump on the same period the previous year.

This is not a future risk. The chief executive of Microsoft confirmed in 2025 that 30% of the company’s code is now written by AI, and more than 40% of Microsoft’s May 2025 layoffs targeted software engineers. The same tools are being deployed across legal services, financial analysis, customer service, and administrative work.

The UK and Canada are not insulated. The tools are global, the labour markets are connected, and whatever is happening to entry-level white-collar work in Boston is happening in Birmingham and Toronto on the same timeline.

The salary you have not yet earned may not exist by the time you go looking for it.

So What Is Anyone Actually Doing About It?

Three countries. Four broken promises. One arithmetic. The political fix is not coming. The salary fix is not coming. So what does coming work look like?

The short answer is that an increasing number of people have stopped trying to win the salary game and have started building income streams that do not depend on an employer, a pension provider, or a government promise.

This is not a passive idea. It is not a hope-and-pray investment strategy. It is the simple recognition that if everything wage-denominated keeps stagnating while everything asset-denominated keeps compounding, the only way out is to participate on the asset side of that equation, on your own terms, with your own time, every week.

There are two practical ways to do this with index options on the world’s most liquid market.

- Collect morning income from the stock market. A defined-risk, short-duration position taken in the first portion of the trading day. Execution time is 20 to 30 minutes. The position is closed the same day. No overnight risk. No traditional stop loss needed, because the risk is defined by the structure of the trade itself. – Learn more here

- Collect weekly income from the stock market. A defined-risk position designed to be opened and closed within the week. Same defined-risk principle. Same liquid market. Same disciplined execution. – Learn more here

These are not get-rich-quick ideas. They are not replacements for a long-term capital base. They are an alternative income stream for people who have looked at the salary, the pension, the inflation and the job-security numbers above and concluded that the deal they were sold is not coming back.

If you are reading this and recognising the picture, you are not alone. The numbers in this article describe an entire generation in three countries. The question is not whether the old deal is broken. The data has already settled that. The question is what you build instead.

If this resonates, share it with someone who is working hard, saving where they can, and quietly wondering why none of it seems to add up. The arithmetic in this article is not their fault. But what they do next is their decision.

Sources for every figure cited in this article are drawn from the UK Office for National Statistics, the US Federal Reserve and Census Bureau, Statistics Canada, the OECD, the Joint Center for Housing Studies at Harvard, the UK Pensions Commission, the US National Institute on Retirement Security, the PLSA, Vanguard, Indeed Hiring Lab, the Brookings Institution, Visual Capitalist, Goldman Sachs Research, Cornell University, Anthropic, and Microsoft.