I Stopped Buying Options. Here’s Why.

Ahoy there, Trader! ⚓️

Ahoy there, Trader! ⚓️

It’s Phil…

The thesis in one line

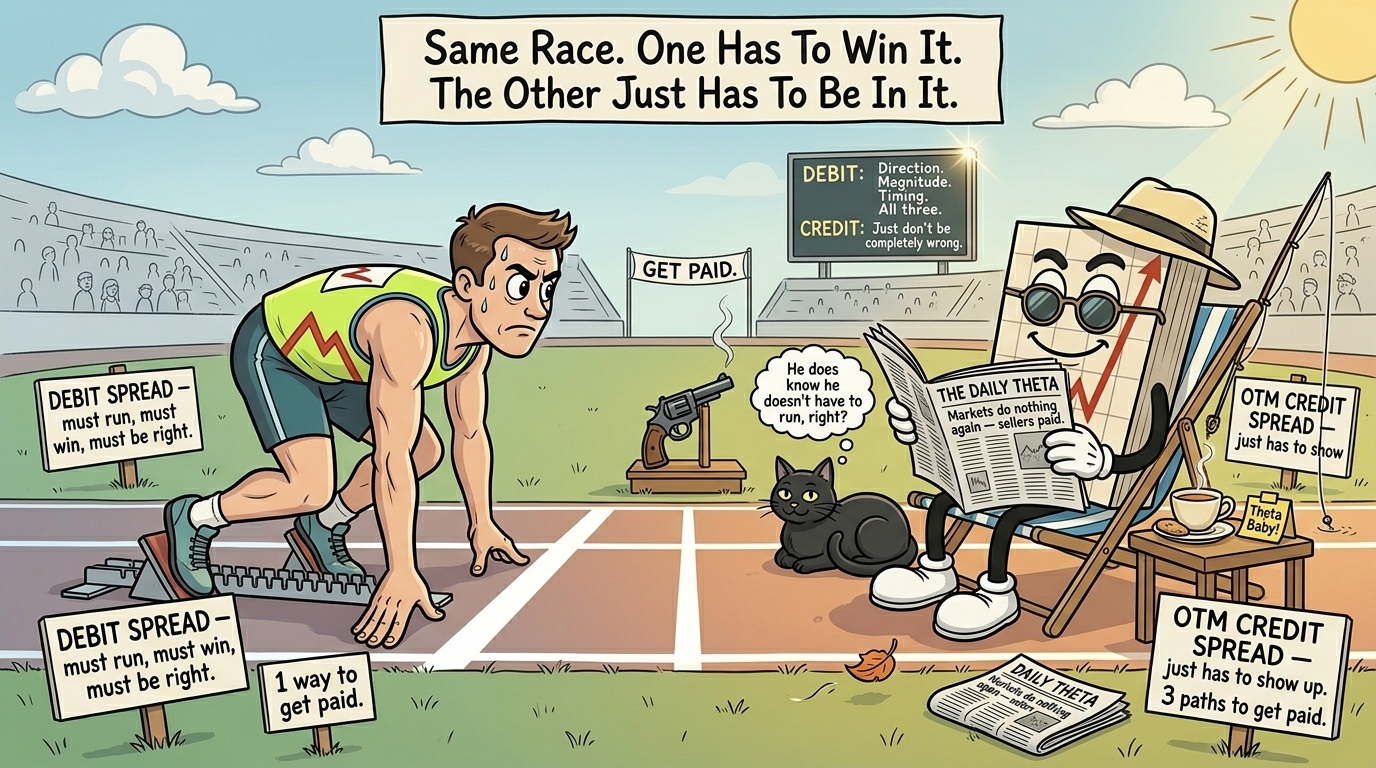

A debit spread pays you for being right about direction. An OTM credit spread pays you for not being completely wrong. Over enough repetitions, those are not the same business.

I have spent over three decades watching traders argue about which spread is better. Most of those arguments miss the point entirely. The question is not which spread has the better risk-reward ratio on any single trade. The question is which spread structure aligns with what humans are actually capable of doing repeatedly: predicting direction, magnitude, and timing all at once, or simply identifying a price level the market is unlikely to trade through in the next few days.

The first job is exhausting and statistically thankless. The second is mechanical. That distinction is the entire article.

The mechanics, briefly, because the maths is the whole argument

Forget the textbook definitions for a moment. A vertical spread is just two options of the same expiry, same underlying, different strikes, one short and one long. There are four flavours:

- Bull put spread (credit, bullish to neutral): sell a higher-strike put, buy a lower-strike put. You get paid up front and you want the underlying to stay above the short strike.

- Bear call spread (credit, bearish to neutral): sell a lower-strike call, buy a higher-strike call. You get paid up front and you want the underlying to stay below the short strike.

- Bull call spread (debit, bullish): buy a lower-strike call, sell a higher-strike call. You pay up front and you need the underlying to rally past the long strike.

- Bear put spread (debit, bearish): buy a higher-strike put, sell a lower-strike put. You pay up front and you need the underlying to fall past the long strike.

The arithmetic across all four is the same skeleton:

- Width = difference between the strikes

- Credit spread max profit = net credit received

- Credit spread max loss = width minus net credit

- Debit spread max loss = net debit paid

- Debit spread max profit = width minus net debit

Notice the asymmetry hiding in that arithmetic. On a credit spread your maximum profit is achieved if the underlying does literally nothing. On a debit spread your maximum profit requires the underlying to move all the way through both strikes by expiry. Doing nothing is statistically a much more common outcome than moving through two strike prices on a deadline.

Get The Complete Premium Popper System – Automation Included

Your entry ticket to consistent SPX income. Inside: the exact setup, rules, and checklists I trade daily – for less than the cost of lunch. Easily actionable.

Get The Premium Popper System – Click Here

The real broker comparison, like for like

Here is the cleanest possible comparison. Same underlying. Same width. Same days to expiry. Same starting price. Snapped at the weekend close so there is no price movement during analysis.

Setup:

- Underlying: SPX

- Spot price: 7,473.47

- Expiry: 6 days (May 29, 2026)

- Width: 5 points

- Short strike for both: 7,470

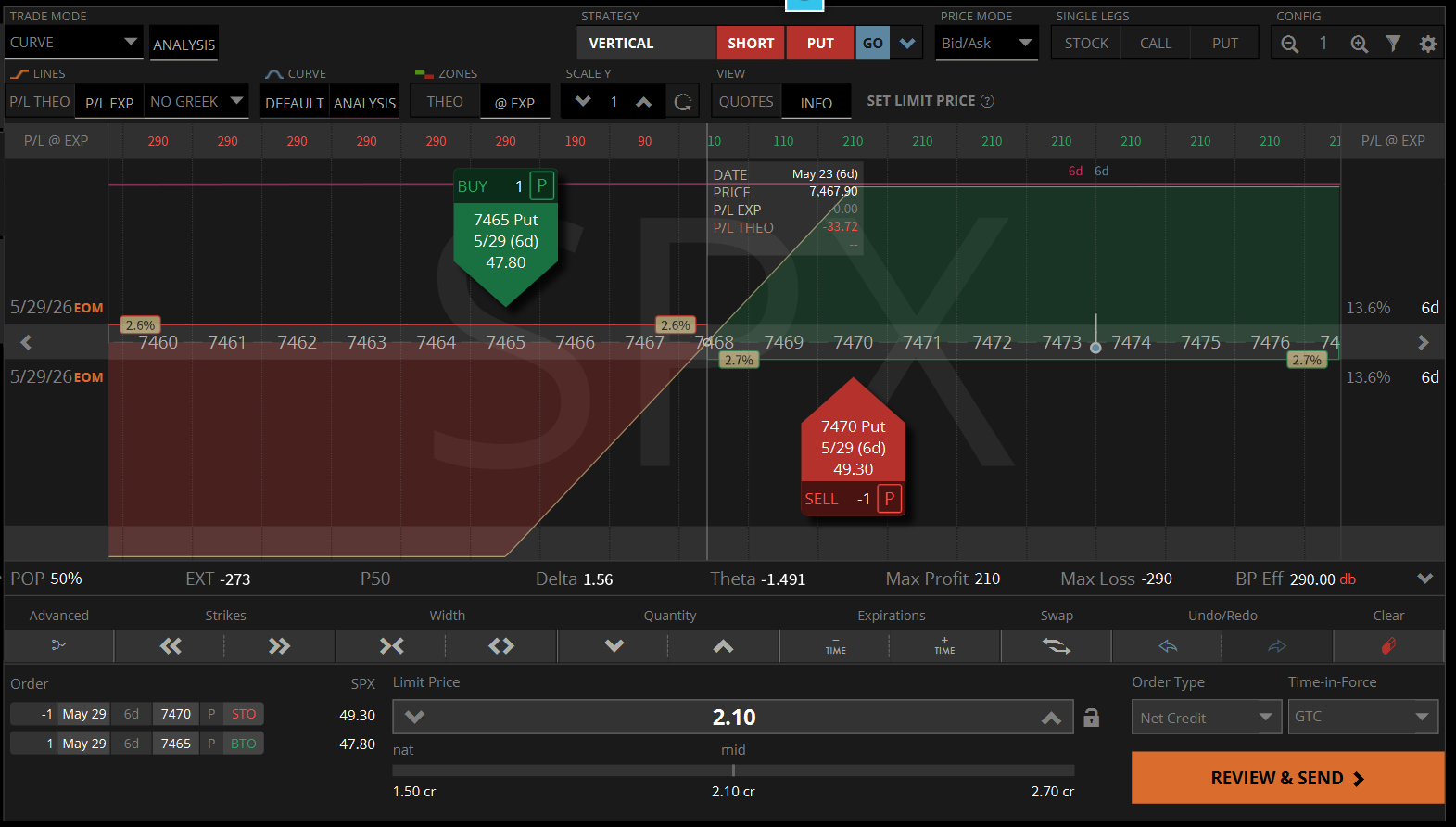

The ATM Credit Spread (Bull Put 7470/7465)

- Sell 7470 Put @ $49.30

- Buy 7465 Put @ $47.80

- Net credit: $2.10 mid ($210 per contract)

- Max profit: $210

- Max loss: $290

- Buying power required: $290

- Probability of profit: 50%

- Theta: working in your favour

- Breakeven: 7,467.90 (5.57 points below current price)

The ATM Debit Spread (Bull Call 7470/7475)

- Buy 7470 Call @ $51.50

- Sell 7475 Call @ $48.20

- Net debit: $2.80 mid ($280 per contract)

- Max profit: $220

- Max loss: $280

- Buying power required: $280

- Probability of profit: 49%

- Theta: working against you

- Breakeven: 7,472.78 (0.69 points above current price)

What the numbers actually say

The risk-reward looks superficially similar. That is what efficient option pricing does. But look where the breakevens sit:

- Credit spread breakeven: 7,467.90. SPX can drop 5.57 points and the trade still breaks even. To get full profit, SPX simply needs to be above 7,470 in 6 days. That can happen if it rallies, drifts sideways, or even drops up to $3.47 from current price.

- Debit spread breakeven: 7,472.78. SPX must rally at least 0.69 points just to break even. To get full profit, SPX must rally to 7,475 or above. If it sits still, you lose. If it drops a single point, you lose. If it rallies but stops just short of breakeven, you lose.

Here is the killer scenario. If SPX closes Friday at exactly 7,473.47, unchanged from where it is right now:

- The credit spread keeps the full $210.

- The debit spread loses the full $280.

Same starting price. Same ending price. Same width of structure. Opposite outcomes from the market doing nothing at all.

That is the asymmetry that no risk-reward calculation captures. Doing nothing is the most common thing markets do over short horizons. The credit seller is paid for that fact. The debit buyer pays for the opposite hope.

One variable versus three paths

This is the philosophical spine of the entire article. Once you see it, you cannot unsee it.

The debit spread has one variable

Direction. Get it right, get paid. Get it wrong, lose. That is the entire decision tree.

Up to breakeven, the trade is a loser. Past breakeven, the trade is a winner. There is one single condition that must be met: the market must move in your chosen direction, far enough, fast enough, before expiry.

- Wrong direction? Lose.

- Right direction but not far enough? Lose.

- Right direction, far enough, but too slow? Lose.

- Sideways? Lose.

One variable. One way to win. Three ways to lose.

The OTM credit spread has three paths to profit

Path one: right on direction. Market moves up (for a bull put credit). You get paid. Often faster than you would expect, because if you close the trade early before expiry, time decay plus a favourable directional move can collapse the spread value quickly. Active management captures this.

Path two: flat. Market does nothing at all. Sideways. Zero movement. You still get paid. The credit you collected up front decays into your account as time passes regardless of what the chart does.

Path three: wrong on direction, by a tolerable amount. Market moves against you, but not past your short strike, and not far enough to overwhelm the credit you collected. You still get paid, either fully (if it stays above the short strike) or partially (if it drifts into the spread but stops above your breakeven).

Three paths to profit. One way to lose, and only when you are significantly wrong, not slightly wrong.

Count the variables you have to be right about

Debit spread: Direction. One variable. Get it right or lose.

OTM credit spread: You can be wrong about direction (path two). You can be wrong about direction and magnitude (path three). You can be right about direction (path one). The structure absorbs being wrong in two distinct ways before it fails.

This is all before any entry filter, any IV regime selection, any opening-range setup, any timing logic, any management rule. Just the raw mechanical structure of the trade. The credit spread starts the race with three legs to the debit spread’s one.

The bookmaker analogy is the cleanest way to see this. A bookmaker does not need to predict who wins the race. They set the odds and they get paid by everyone who is wrong. The credit seller is the bookmaker. The debit buyer is the punter at the rail with a betting slip, hoping. (For the full philosophical treatment of this, see the Probability Over Prediction article on the Knowledge Edge hub.)

Where the OTM credit spread really shines

The ATM comparison shows the structural asymmetry. The real-world income setup is where it actually shines.

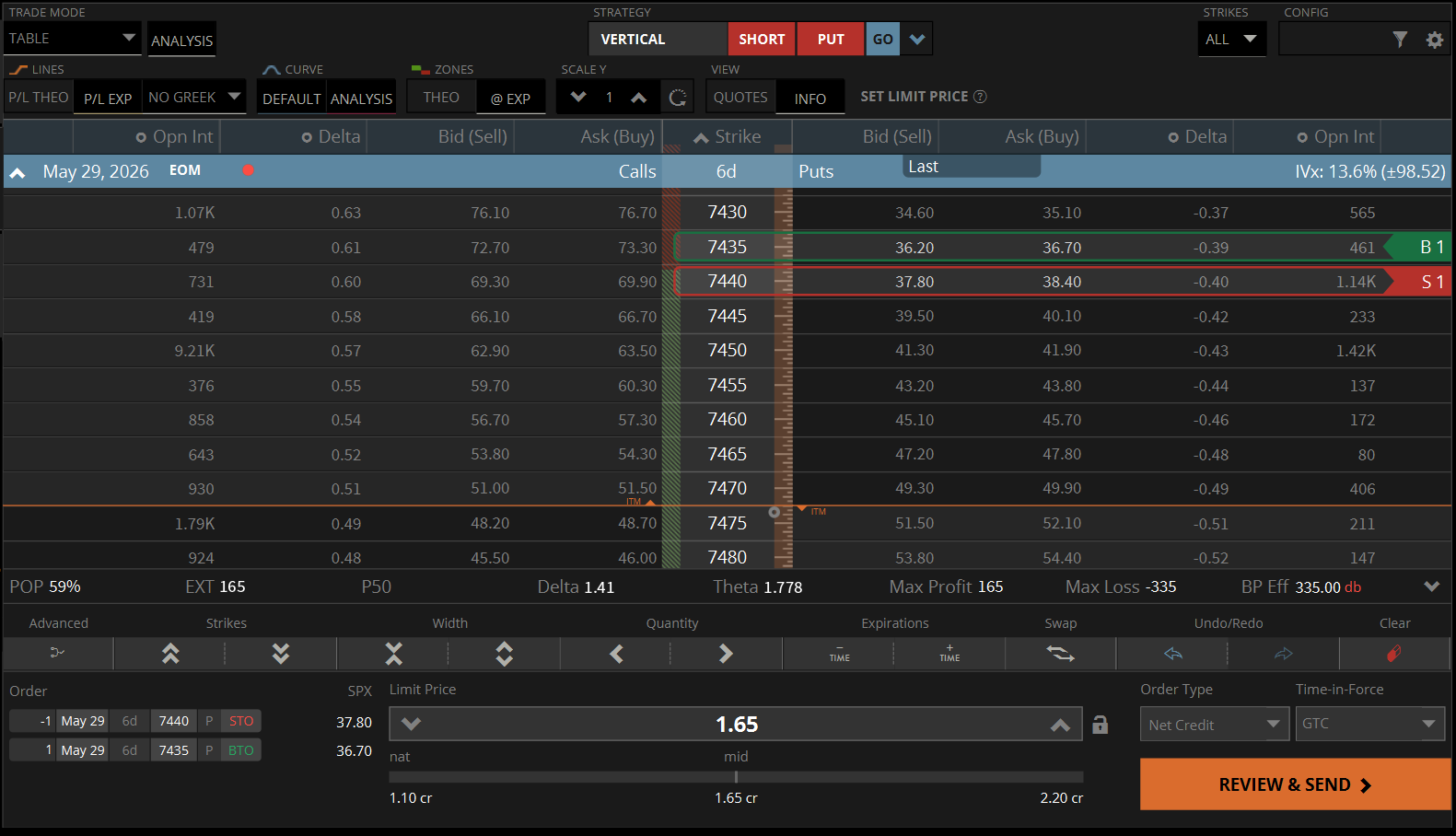

The standard systematic income setup is not an ATM credit spread. It is an out-of-the-money credit spread sold at roughly the 40-delta level on the short strike. This pulls the entire structure further away from current price and stacks probability harder in your favour.

40-Delta OTM Credit Spread (Bull Put 7440/7435)

- Sell 7440 Put @ $37.80 (delta 0.40)

- Buy 7435 Put @ $36.70 (delta 0.39)

- Net credit: $1.65 mid ($165 per contract)

- Max profit: $165

- Max loss: $335

- Buying power required: $335

- Probability of profit: 59%

- Theta: working strongly in your favour

- Breakeven: 7,438.32 (35.15 points below current price)

Wrong by 33 points and still paid in full

Look at where that breakeven sits. SPX can fall 35 points, a 0.47% drop, and the trade still breaks even. To get full max profit, SPX simply needs to stay above 7,440 by Friday. That covers a rally of any size, sideways drift of any duration, and a 33-point fall.

Compare that to the ATM debit spread which needed a rally of even a single point to break even. The 40-delta credit spread can be wrong by 33 points and still pay maximum.

This is what “wrong but not completely wrong” actually looks like on the screen. You can be wrong all the way down to your short strike and still get paid in full. That is not a marketing line. That is the literal pricing on a real broker platform on a real weekend.

Why timing matters less than most people think

Here is the part that gets glossed over in most options content. The OTM credit spread structure absorbs timing errors in a way the debit spread cannot.

Most traders, regardless of experience level, can identify a reasonable trade setup. Charts repeat, patterns persist, levels matter. Finding good trades is not where retail traders bleed money. Retail traders bleed money on execution and management. They enter too late, exit too early, panic on adverse moves, freeze on profitable ones, get chopped by intraday noise, and second-guess themselves on otherwise sensible setups.

The OTM credit spread does not care about any of that, within reason. If you place a 40-delta credit spread on what turns out to be a slightly mistimed entry, you do not need a clean directional move to bail you out. You need the market to not collapse past your short strike. A mistimed entry that drifts sideways for two days still pays. A mistimed entry that grinds down 20 points still pays. A mistimed entry that ranges around in chop still pays.

The same mistimed entry on a debit spread is dead on arrival. It needs the directional move to materialise and be fast enough to outrun theta decay. Anything less and the trade bleeds out.

This is the genuinely overlooked advantage of credit spread structures: they are forgiving of the exact mistakes retail traders most commonly make. The probability edge is one part of it. The structural forgiveness is the other, and it is arguably the more important of the two for traders still building execution discipline.

The honest bit – risk-reward and expectancy

I will not insult anyone by pretending the 40-delta OTM credit spread has a better risk-reward ratio than the ATM debit. It does not. $165 max profit against $335 max loss is roughly 1:2 against you. One full loss takes out two full winners. The maths is what it is.

This is the part most options content quietly skips. We will not skip it.

Raw expectancy at expiry, assuming no active management:

- 40-delta credit at 59% POP: (0.59 × $165) − (0.41 × $335) ≈ −$40 per trade

- ATM credit at 50% POP: (0.50 × $210) − (0.50 × $290) = −$40 per trade

- ATM debit at 49% POP: (0.49 × $220) − (0.51 × $280) ≈ −$35 per trade

If you hold any of these to expiry and let them run to their statistical outcome, you lose money. Option pricing is roughly efficient. Market makers are not idiots.

So how does anyone make money selling premium?

Four sources of real edge, none of which show up in the at-expiry expectancy:

1. Active management. Closing winners at 50% of max profit before they reach full expiry. Cutting losers before they reach max loss. This shifts the entire expectancy curve because you are no longer accepting the binary at-expiry outcome. Both tastytrade and OptionAlpha’s public research consistently show that managing winners at 50% of max profit on credit spreads materially improves long-term returns and reduces drawdown.

2. The variance risk premium. Implied volatility on SPX has averaged about 4 percentage points above realised volatility for thirty-plus years. This is the structural overpricing of options that sellers harvest. Bondarenko’s 2019 Cboe-sponsored white paper on the CBOE PutWrite Index documents 9.54% annualised returns vs the S&P’s 9.80%, with a third less volatility and a smaller maximum drawdown. The structural edge is real and it is persistent.

3. Trade selection. A credit spread placed at random on a random day is not the same as a credit spread placed when the index has confirmed an intraday directional bias. Entry filters such as opening range breakouts align the structure with intraday flow rather than fighting it.

4. Position sizing. A 1-2% risk per trade rule means a max loss is survivable. A 10% risk per trade rule means one bad day ends the strategy. Position sizing is not a sub-topic of options trading; it is options trading. Everything else is execution detail on top.

These four together are what turn a structurally neutral expectancy at expiry into a positive expectancy in practice. The Premium Popper System at AntiVestor sits on exactly these four pillars, which is why it leans on 0-DTE SPX credit spreads with structural entry filters rather than ATM debit spreads on equities. (See the Wall of Wins for the running log of how that plays out in live trading.)

When debit spreads actually are the right tool

I owe debit spreads an honest hearing. They are not stupid. They are the correct choice when:

Implied volatility is genuinely depressed and you expect it to rise. Long vega is your friend, short vega is your enemy. A long debit spread benefits from IV expansion. A short credit spread suffers from it. If IV is at a multi-year low and you have a directional view, the debit spread is the cleaner expression.

You have a genuine high-conviction directional view with a defined catalyst. If you firmly believe a stock will move 8% in the next three weeks because of an earnings cycle, a regulatory decision, or a product launch, a debit spread offers convex defined-risk exposure to that view. The credit spread cannot match that asymmetric upside.

You want a small, defined-risk speculation. £200 of conviction on a known outcome with a small defined loss and a meaningful potential payoff. Debit spreads give you exactly that. They are good lottery tickets.

You are playing an event where IV will crush both ways. A tightly structured debit spread around a known event can sometimes outperform a credit spread on the same view because the directional move is the dominant force and the IV crush hits both legs.

What debit spreads are not is a systematic income engine. They are a directional bet with a hedge. Treating them as a recurring weekly income strategy is roughly equivalent to playing the lottery every Friday and calling it a yield strategy.

The Greeks, in plain English

You only need three.

Theta is the daily cash flow from time passing. Credit spreads collect it. Debit spreads pay it. On a 0-DTE position, theta is enormous near at-the-money strikes in the final 90 minutes of trading. Time decay is not a metaphor; it is a number that hits your P&L every day the market is open.

Gamma is how fast your delta changes as the underlying moves. Short-dated short options have brutal gamma. A credit spread that looked safe at 11am can be at max loss by 3pm if the market trends through the short strike. This is the genuine, non-negotiable cost of being a seller and the reason position sizing matters more than entry timing.

Vega is how much your position changes value when implied volatility changes. Credit spreads benefit when IV falls (vol crush). Debit spreads benefit when IV rises. Selling premium into elevated IV and watching vol normalise is one of the cleanest setups available in options.

This is also why the “low IV environment” objection to credit spreads is legitimate and gets honoured in the previous section.

The behavioural problem with retail

Three findings deserve flagging together because they describe the same person.

First, directional accuracy is not the constraint. Barber, Lee, Liu and Odean’s “The Cross-Section of Speculator Skill: Evidence from Day Trading” (Journal of Financial Markets, 2014) concluded that less than 1% of the day trader population is able to predictably and reliably earn positive abnormal returns net of fees. Direction is the wrong place to plant your flag if direction is the only way to get paid.

Second, retail prefers lottery structures. Kahneman and Tversky’s prospect theory explains this neatly: people overweight small probabilities and feel losses roughly 2.25 times as strongly as equivalent gains. Buying an out-of-the-money call is the textbook lottery structure (small loss probable, large win possible). Selling a credit spread is the inverse (small win likely, larger loss possible but bounded). Retail crowds the buy side because that is what their wiring tells them feels right.

Third, the data on retail options buyers is unambiguous. Beckmeyer, Branger and Gayda’s 2023 working paper “Retail Traders Love 0DTE Options… But Should They?” documents that retail investors lost about $241,000 a day on average trading 0DTE options between February 2021 and September 2023, climbing to $358,000 a day after daily SPX expiries launched in May 2022. Within that same dataset, retail short positions in options were profitable. The losing leg is the buying leg.

Most retail options activity is a wealth transfer from buyers to sellers, mediated by overconfidence and prospect theory. That is not a marketing claim. That is what the academic literature, the broker data, and the long-run performance of the CBOE PutWrite Index all converge on.

Decision framework

Before you put a vertical on, run through these honestly:

1. What is my IV rank? Below 20 favours debit. Above 30 favours credit. Below 10 makes me question whether to be in the trade at all.

2. What is my directional conviction, honestly? “I think it will probably drift up” is credit-spread conviction. “I am certain it will rip higher in the next week” is debit-spread conviction. Most retail conviction is the first kind being mis-sold as the second.

3. What is my time horizon? Inside a week, theta is enormous and credit spreads dominate. Beyond 45 days, the relative advantage narrows considerably.

4. What is my maximum acceptable loss? Is the spread width small enough that one max-loss event is survivable at my position size? If a single max loss is more than 2% of account equity, the position is too big.

5. Is the underlying cash-settled or share-settled? SPX, XSP, NDX are cash-settled and remove pin risk. SPY, QQQ, and equity options are share-settled and carry assignment risk on short positions, particularly around ex-dividend dates.

6. Am I selling because I have an edge, or because last week’s trade worked? The variance risk premium is a structural edge. Recency bias is not.

If you cannot answer all six questions clearly, do not place the trade.

The one-line version

If you expect a decisive directional move and IV is low, buy a debit spread. If you expect the market to stay within range and IV is elevated, sell a credit spread. Everything else is a variation on that principle.

For systematic income, credit spreads are the structural choice not because they are clever or sophisticated, but because they only require you to be right about where the market probably will not go. That is a much easier question than where it definitely will go, by when, and how far. Markets do “nothing” far more often than they do “something specific.”

The Premium Popper System runs on this logic, applied mechanically to 0-DTE SPX credit spreads with structural entry filters and disciplined position sizing. Not because it is the only thing that works, but because it is the thing that aligns mechanical structure with the actual statistical behaviour of the index. The full system breakdown can be found here, and the running results live on the Wall of Wins.

Caveats

A few I want to flag explicitly, in the spirit of polish-never-invent.

- All the backtest figures cited above are historical. None of them guarantee future returns. The 1990–2024 sample period covers multiple stress events including 2008 and 2020, but it is not exhaustive.

- 0-DTE markets are still young. Daily SPX expirations only launched in May 2022, and most published 0-DTE backtests do not yet include a true bear market with elevated correlations and persistent gap risk.

- The bid/ask spreads shown above are weekend snapshots and will widen slightly during market hours. The mid price assumes you can get filled, which on SPX 5-wide ATM verticals is usually achievable but not guaranteed.

- Win rate is not edge. A 90% win rate with a 1:10 risk-reward still loses money. Always check expectancy in dollars per trade after expected drawdowns, not just win percentage.

- Position sizing matters more than entry timing for any defined-risk premium-selling strategy. The maths of one max loss versus many small wins is unforgiving.

- Nothing in this article is financial advice. It is a description of the structural maths and what the academic and industry data say about how that maths plays out in practice. Whether any of it suits your circumstances is between you and a regulated adviser.

The summary, if you read nothing else

Debit spreads need you to be right about one variable: direction. One way to win, three ways to lose.

OTM credit spreads pay you on three paths: right on direction, flat with no movement, or wrong on direction by a tolerable amount.

Same underlying. Same width. Same days to expiry. The credit spread starts the race with three legs to the debit spread’s one. That advantage exists before any entry filter, timing logic, or management rule layered on top.

Most traders can find decent setups. Where they bleed money is in execution and timing. The OTM credit spread is forgiving of exactly those mistakes in a way the debit spread cannot be.

Over enough repetitions, those are not the same business. Pick the one that aligns with what you can actually do, repeatedly, without needing to be a fortune teller.

For more on the structural and probabilistic underpinning of this approach, check out The Premium Popper System.

TL;DR

- A debit spread has one variable that must be right: direction. Miss it and you lose.

- An out-of-the-money credit spread has three paths to profit: right on direction (up), flat with zero movement, or down by a tolerable amount that still leaves you above the short strike.

- That asymmetry exists before any entry filter, timing logic, or IV regime selection. It is baked into the raw mechanics of the trade structure itself.

- Same underlying, same width, same days to expiry, same starting price. Opposite breakevens. The credit seller’s breakeven sits below current price. The debit buyer’s sits above it.

- The structural reason this works long-term is the variance risk premium: SPX implied volatility has averaged roughly 4 percentage points above realised volatility since 1990. Sellers harvest that gap. Buyers pay it.

- Debit spreads have legitimate uses (low IV, high-conviction directional plays, event-driven setups). But as the engine of a systematic income process, the credit spread does a fundamentally different and easier job.

Happy trading,

Phil

Less Brain, More Gain

…and may your trades be smoother than a cashmere codpiece

p.s. There are 3 ways I can help you…

- Option 1: The SPX Income System Book (Just $12)

A complete guide to the system.

Written to be clear, concise, and immediately actionable.

>> Get the Book Here

- Option 2: Full Course + Software Access – 50% off for Regular Readers – Save $998.50

Includes the video walkthroughs, tools for TradeStation & TradingView, and everything I use daily. Plus 7 additional strategies

>> Get DIY Training & Software

- Option 3: Join the Fast Forward Mentorship – 50% off for Regular Readers – Save $3,000

>> Join the Fast Forward Mentorship – trade live, twice a week, with me and the crew. PLUS Monthly on-demand 1-2-1’s

No fluff. Just profits, pulse bars, and patterns that actually work.